The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

One man’s tax strategy is another’s moral outrage, and few tax maneuvers evoke more controversy than the recent popularity of “buy, borrow, die.” (BBD).

The concept is simple. Say you’re a billionaire whose net worth is tied up in equities, either private or publicly traded. Further assume that one fine day a Gulfstream III or private equity opportunity catches your fancy.

Trouble is, although you’ve got an 11-figure net worth, maybe you don’t happen to have the requisite $125 million kicking around in cash for the jet or the shares, and you’d prefer not to incur the humungous capital gains tax incurred by selling your low-basis stocks.

No problem: Simply borrow that sum against your stock portfolio and keep your equities intact. The basic idea, as explained in this Forbes article: Don’t ever sell your stocks, then bequeath them to your heirs who can sell it the next day cap-gains free at the step-up basis; if deftly deployed, this strategy can keep your holdings free from capital gains tax for generations.

Over the past decade, this strategy has attracted an increasing amount of attention, both positive and negative. A Merrill Lynch “financial advisor” quoted in a 2021 Wall Street Journal article opined that “You could buy a boat, you could go to Disney World, you could buy a company; the tax benefits are stunning.”

The step-up basis lies at the heart of BBD: The conservative National Taxpayers Union Foundation correctly points out that the inheritance tax necessitates it, since adding an additional capital gains tax on estates would amount to double taxation. It’s interesting that the step-up basis, encapsulated in 26 U.S. Code § 1014, has been around for several decades, long before BBD came into fashion. (The piece’s ideological tipoff: the term “inheritance tax” appears nowhere in the article. It’s “death tax,” of course.)

The liberal response to BBD is equal and opposite, typical of which is a recent article by Atlantic columnist Rogé Karma entitled “Buy, Borrow, Die: How to be a billionaire and pay no taxes,” which labels the maneuver “the mother of all tax loopholes.” Fifteen Democratic senators, led by Oregon’s Ron Wyden, have introduced the “Billionaires Income Tax Act” which would, among other provisions, apply a wealth tax on total assets in excess of $1 billion. In the current congressional configuration, this particular snowball would require a considerable adjustment to the thermostat in Hades.

The Math Behind the Theory

The theory goes something like this. The University of Chicago's Center for Research in Security Prices reports an annualized compound return of 10.16% for U.S. stocks over the period from 1926 to 2023. So, if one can borrow at 6% with a securities-baked line of credit (SBLOC) and earn 10.16%, the investor benefits in two ways:

- They earn the additional spread of 4.16% annually.

- Their heirs get the step-up basis upon death without having to pay capital gains tax.

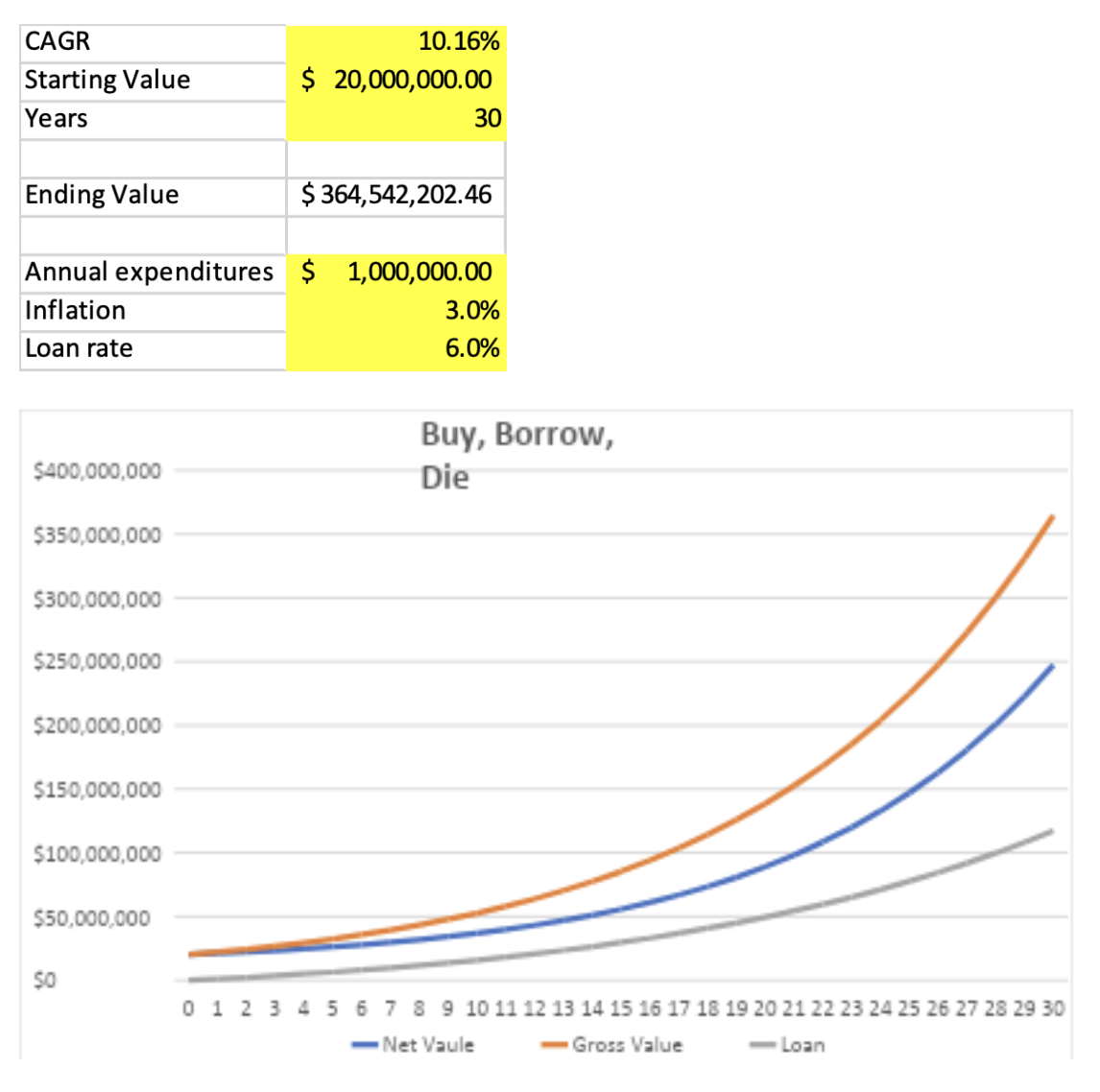

Let’s take an example of an executive at XYZ company whose stock goes public. The executive’s stock is suddenly worth $20 million. His basis in the stock is only $100,000. He holds the stock for 30 years and passes it on to his heirs. If the stock returns a compounded 10.16% (paying no dividend), it will be worth over $364,500,000.

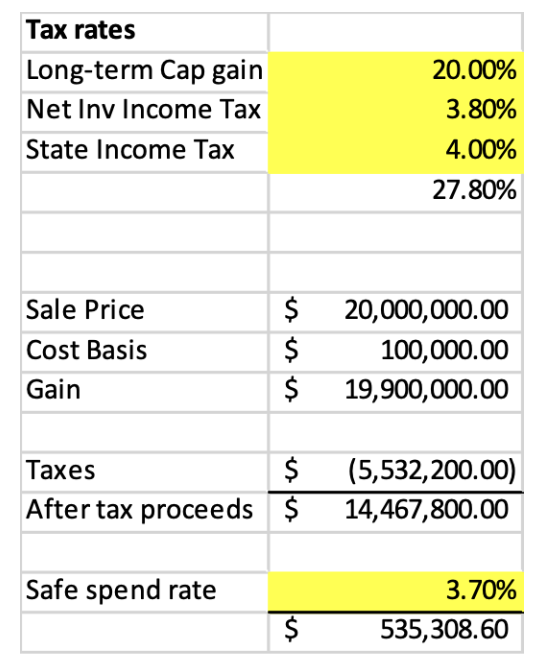

However, this executive wants to live large and spend one million dollars annually after taxes, increasing with an estimated 3% inflation. His advisor recommends diversification into a portfolio of 50% stocks and 50% bonds. This will leave him with $14.468 million and, using a 30-year life expectancy, allows only a $535,300 real withdrawal rate, according to Morningstar.

To make matters worse, this is a withdrawal rate, and he will have to pay taxes on his income and realized gains on his portfolio. Another broker approaches him with the last two steps of BBD. The broker presents the following calculations, where he borrows one million dollars per year (increasing with inflation) for the next 30 years without paying a penny in taxes. The numbers show the loan to collateral value hits a maximum of 35.7%, remaining well below the 50% margin loan maximum, and actually declines over the last decade. Ultimately, he dies in 30 years leaving almost a quarter billion dollars to his heirs — all tax-free with the step-up basis and after paying off the loan.

When Theory Hits Reality

If this solution scares the heck out of you, you’re on the right track. There are several flaws with this strategy.

While the U.S. stock market has turned in a cumulative 10.16% annualized return for nearly a decade, very few stocks have done that well. Research by Hendrick Bessembinder of the W. P. Carey School of Business at Arizona State revealed that, from 1926 to 2023, 96 percent of stocks collectively matched one-month T-bills. The majority (51.6%) of these stocks had negative cumulative returns.

Further work on the compound returns for over 64,000 global common stocks from 1991 to 2020 showed that the majority — 55.2% of U.S. stocks and 57.4% of non-U.S. stocks — underperform one-month U.S. Treasury bills. Further, the top-performing 2.4% of firms account for all of the $75.7 trillion in net global stock market wealth creation during the thirty-year period.

That is to say, stock market returns are highly skewed. Though it’s possible XYZ Company could fall under that lucky 2.4% of wealth creators, the odds are that the strategy recommended by the broker will fail spectacularly.

Diversify Without Selling

The broker comes back with another solution – the exchange fund. The executive contributes all $20 million of his XYZ shares to the exchange fund. The assets are pooled with others having highly concentrated positions in different stocks. For example, say 19 other investors join the fund with different stocks; they don’t have to contribute an equal value. Let’s also say the new pool is created with a total value of $200 million. The executive would then own 10% of the new, more diversified fund. He could then continue with the borrow and die strategy, says the broker.

This strategy is also flawed in many ways. First, 20 stocks aren’t even close to having a diversified portfolio. And there are very high fees associated with exchange funds, not to mention restrictions on selling.

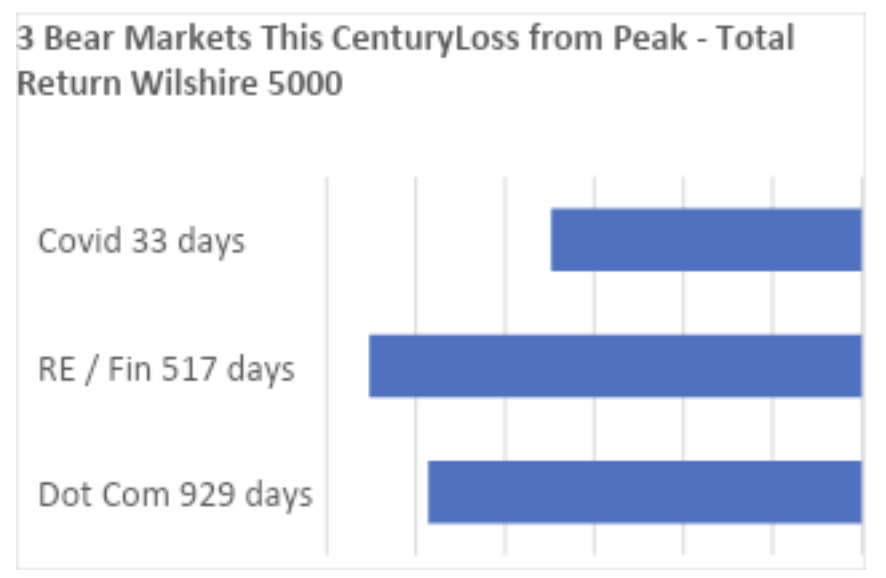

But, aside from this, there are other issues. Margin loans are typically limited to 50% and there have been two bear markets of about this level since 2000. Even in 2020, the stock market lost nearly 35% in the 33 days ending on March 23.

Two Issues With SBLOC (Margin) Loans

The first problem with the borrowing part of BBD is the fact that lenders may not allow 50% margins for concentrated positions. It could even be as low as 25%. And the FINRA disclosure notes “The firm can increase its ‘house’ maintenance margin requirements at any time and is not required to provide you advance written notice.”

Next, margin loans rates are typically variable. If fixed, they are typically fixed for a very short period of time and can then adjust. People who took out margin loans in 2021 saw their rates skyrocket in 2022.

Estate vs. Long-Term Capital Gain Taxes

In the example, the client was in the 20% federal long-term capital gains tax rate and will be paying the 3.8% net investment income tax, or a total of 23.8% federal. Compare that to the current federal estate tax rate of 40% for amounts over $1 million. Many states have estate or inheritance taxes as well. While the current federal estate tax exemption is nearly $14 million ($28 million for a couple), there is no way to know what it will be in a couple of decades. And, for the super wealthy, even $28 million is immaterial.

Because estate taxes trump long-term capital gains taxes, various irrevocable trusts tend to be the vehicle of choice for the very and super wealthy. This allows the assets to be passed down for generations, possibly skipping estate taxes altogether. But irrevocable trusts are legal entities themselves and don’t get a step-up in basis. In other words, the irrevocable trust could be better than the BBD strategy as it’s the more tax-efficient vehicle.

Now, it may be possible to get both the step-up and avoid estate taxes through some sophisticated tax planning where the trust has the right of substitution. But now you’d be playing with dynamite. You’d have to be lucky enough to have an individual security that performs at least as well as the market for decades and loopholes in estate tax laws not being closed.

Conclusion

The current agita over BBD reminds one of Gertrude Stein’s verdict on her hometown of Oakland: “there is no there there.” Not only, as seen above, does the strategy fail to pencil out, but research by academics Edward Fox and Zachary Liscow demonstrates that portfolio cash flows of the overwhelming majority of the uber-rich are sufficient to meet even the most extravagant of consumption and investment needs. Thus, they have no need of BBD.

According to Fox and Zachary, “the rich have a large amount of liquid income… [and] their savings rates are high, suggesting that the main tax avoidance strategy of the super-rich is ‘buy, save, die.’”

The ever-louder brouhaha surrounding BBD is thus much ado about nothing. Not only is it expensive, dangerous, and liable to only make bankers and brokerage firms rich and public coffers poor, it is deployed by only a tiny, impecunious minority with insufficient cash flows who will, at some point, likely be sorry they did.

William J. Bernstein is a neurologist, the co-founder of Efficient Frontier Advisors, an investment management firm, and a writer with several titles on finance and economic history. He has contributed to the peer-reviewed finance literature and has written for several national publications, including Money Magazine and The Wall Street Journal. He has produced several finance titles, and four volumes of history, The Birth of Plenty, A Splendid Exchange, Masters of the Word, and The Delusions of Crowds about, respectively, the economic growth inflection of the early 19th century, the history of world trade, the effects of access to technology on human relations and politics, and financial and religious mass manias. He was also the 2017 winner of the James R. Vertin Award from the CFA Institute.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by William Bernstein, Allan Roth

The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.