The Federal Reserve’s decision to leave interest rates unchanged was right — but easy to misinterpret. “Nothing to see here, move along” wasn’t the intended message. Wary as the central bank might be about saying it too forcefully, the current administration is making its difficult job vastly harder. The conditions for a serious economic setback are falling into place, and there’s little the Fed can do about it.

Until recently, the Fed’s sought-after soft landing — inflation gradually returning to its 2% target without higher unemployment — still looked plausible, even though inflation had proved stickier than anticipated and cuts in the policy rate were thus likely to be somewhat delayed.

Suddenly, though, the outlook is much worse — not because monetary policy is now too loose and aggregate demand too high, but because the administration’s threatened trade war could cause prices to spike by disrupting supply. The new threat is stagflation, and the Fed isn’t equipped to handle it.

The remedy for too much demand is tighter monetary policy. That’s the calculation that preoccupies the central bank. But there’s no monetary-policy remedy for inflation induced by a supply-side shock. If the administration persists with its actual and threatened tariffs, it will deliver exactly that, raising the cost of producers’ inputs, directly adding to consumer prices, and leading workers and investors to expect higher inflation to come. When a central bank responds to supply-side inflation by raising rates, the result is lower output and less-than-full employment.

In short, using monetary policy to fight stagflation is enormously costly. And in such circumstances, the Fed’s dual mandate — stable prices and maximum employment — is simply unachievable.

If the Fed is reluctant to voice such fears openly, that would be understandable. Appearing to criticize the administration’s policies would only make things worse by provoking a response that calls the Fed’s independence into question. In his news conference Wednesday, Chair Jerome Powell emphasized uncertainty and expressed the hope that any pause in progress on inflation due to tariffs would be (despite the word’s unfortunate connotations) “transitory.” Likewise, the new summary of economic projections — the so-called dot plot — foresees no persistent rise in inflation and no recession.

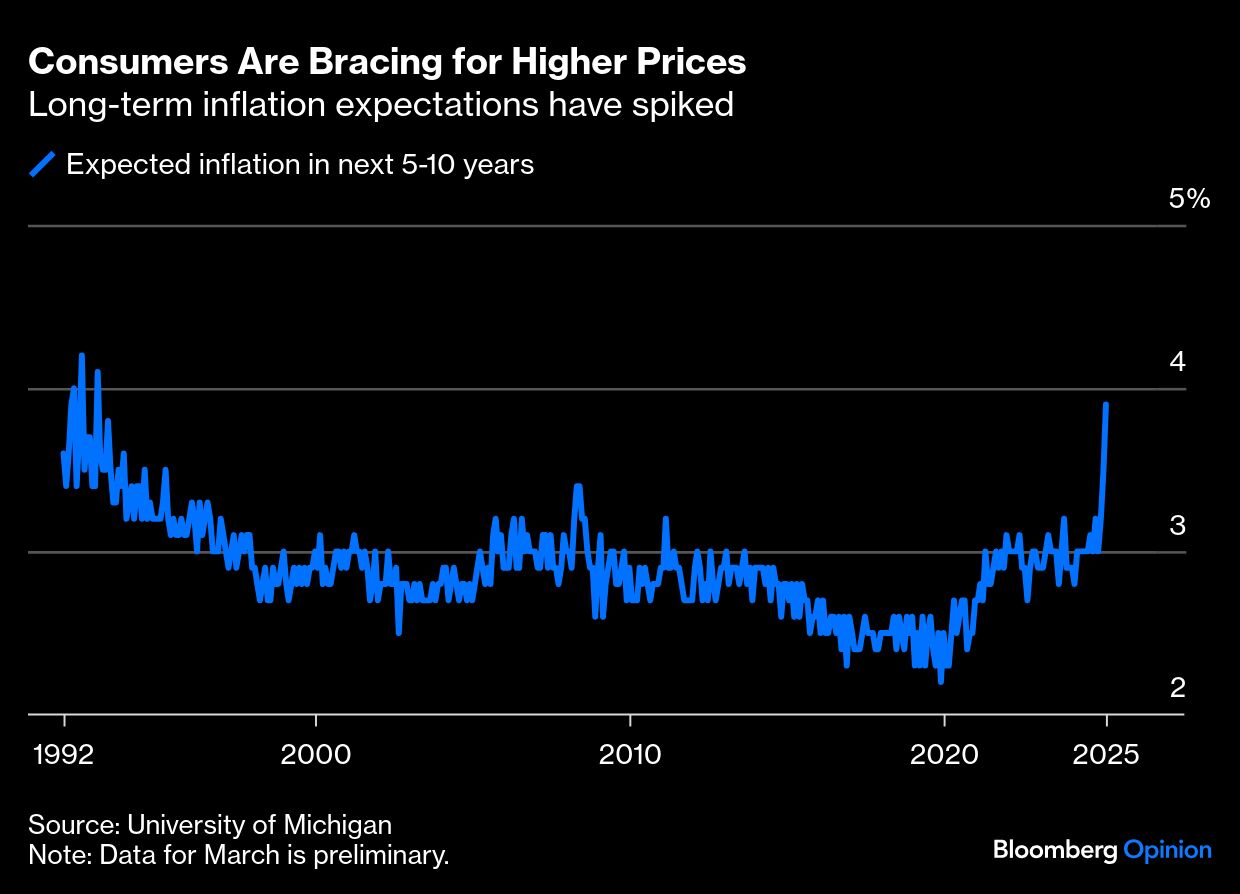

Take that with a very large pinch of salt. There are signs that tariffs are already pushing prices higher. Measures of inflation expectations have surged. And recent research by Fed economists highlights the possibility of persistent effects. If the White House changes course, these setbacks will indeed most likely be temporary. But if it doubles down and keeps its promise to impose “reciprocal and sectoral tariffs” across the board at the start of next month, watch out. The past month’s stock-market turbulence might be as nothing compared with what happens when investors decide that a full-scale trade war has begun.

In that case, don’t assume the Fed can come to the rescue. It’s in much the same position as everybody else — hoping against hope that this senseless act of self-harm can still be averted.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by The Editors