For the last five years, BP Plc has put ideology ahead of profitability. This week, its board of directors has a final chance to change direction. If it doesn’t, an investor revolt will follow, and many executives could be out of a job by summer.

The company’s capital markets day on Feb. 26 is the most anticipated Big Oil strategy update since, well, BP’s last master plan in 2020.

The most pressing question is seemingly contradictory: BP needs to reduce its huge debt pile, but it needs to do so while paying shareholders if not more, then at least the same as they were accustomed to. It’s the corporate version of squaring the circle. As difficult as it is, it’s possible. BP loves using its initials for branding wordplays. Once it was “Beyond Petroleum.” Let’s hope “Big Payouts” will be the replacement for the current less-than-flattering moniker: "Beyond Profits."

Five years ago, the British oil company bet its century-long business model was over: Oil demand had peaked, and the future was renewables, it said. Thus, BP announced a strategic shift that would see the company redirect its investment toward green energies such as solar, wind, hydrogen and biofuels. By 2030, the company had planned to produce 40% less oil and gas than it did in 2020. Under Chairman Helge Lund and former Chief Executive Officer Bernard Looney, BP became the first oil major to embrace net zero.

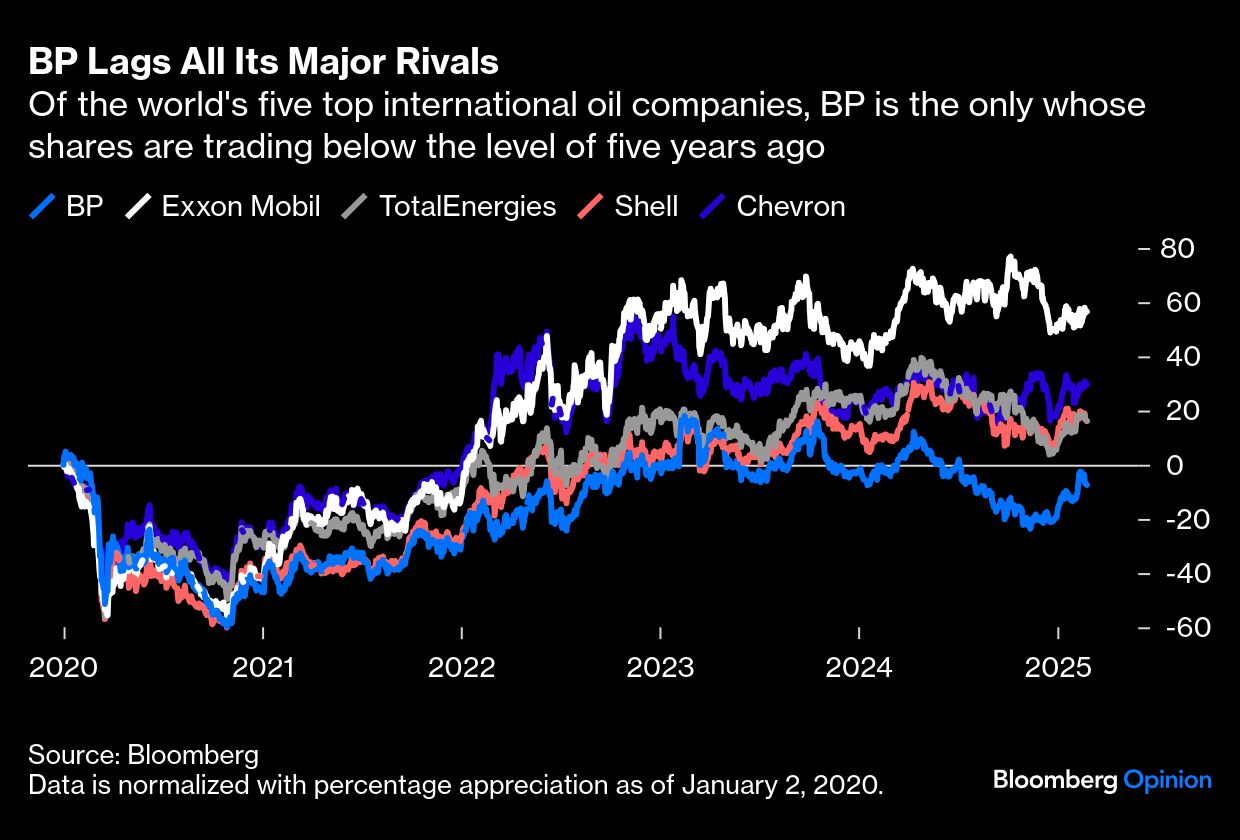

The ideological shift failed spectacularly: Not only did oil demand growth continue but returns on renewables were far lower than expected. Rather than admit defeat, BP persevered, using windfall profit from the Russia-Ukraine war as a smokescreen. But investors were abandoning the company. Its shares trailed every rival. Its market value plunged. Its debt soared.

The knockout came when the board had to fire the strategy’s architect, Looney, for unrelated “serious misconduct,” replacing him in 2024 with his number two, Murray Auchincloss, who, frustratingly, pledged continuity. A year later, the new CEO and the old chairman have finally admitted defeat.

Under pressure from one of the most aggressive activist investors Wall Street has produced — Paul Singer of Elliott Investment Management — the newish CEO promised this month he would use Feb. 26 to “fundamentally reset” the strategy. Let’s keep our fingers crossed that he means it. However, I fear that Auchincloss, still handicapped by an ideological board, would suggest minor surgery. One cut here and there, and perhaps some divestments, leaving shareholders to bear the pain of strengthening the balance sheet via lower total payouts. BP needs far more radical intervention.

Nearly every sell-side analyst assumes that BP will cut total shareholder distributions in 2025 and beyond, reducing buybacks to an annual rate between $5 billion and $4 billion a year from $7 billion in 2024. It’s obvious that in its present shape, BP can’t afford its current buyback bill. But making shareholders bear the cost of previous mistakes would only deepen the mistrust between the company and its investors.

Instead, management can plot a more revolutionary path.

First, it needs a wholesale retreat from renewables, selling most of its wind and solar projects. In short, BP shouldn’t be in the electricity generation business — at all. Stuff like Lightsource, a solar developer, and BP’s joint venture with Japanese investor JERA in wind power should be on the chopping block. So it should its Archaea Energy unit, which produces biogas.

Second, sell some large, non-core assets to pay down a mountain of net debt that, if measured properly including hybrid bonds, reaches almost $50 billion — more than double the debt obligations of either Exxon Mobil Corp. or Chevron Corp. Castrol, the historic lubricant business, should be considered for disposal. Another candidate for divestment is the convenience unit — the stores attached to BP’s fuel stations, which have a much different cash profile. Analysts at investment bank Evercore Inc. reckon each of those divisions could be worth at least $10 billion. With the help of a few additional disposals — pipelines, for example — BP could easily raise $25 billion to halve its liabilities.

Third, refocus spending on fossil fuels, the business it knows, reducing overall investment. Currently, BP is planning to spend $16 billion in new projects in 2025, including at least $5 billon in renewables and other energy-transition businesses. As it retreats from renewables, spending will fall naturally, leaving room for more oil and gas stuff. Ideally, the company should aim to spend not more than $15 billion a year.

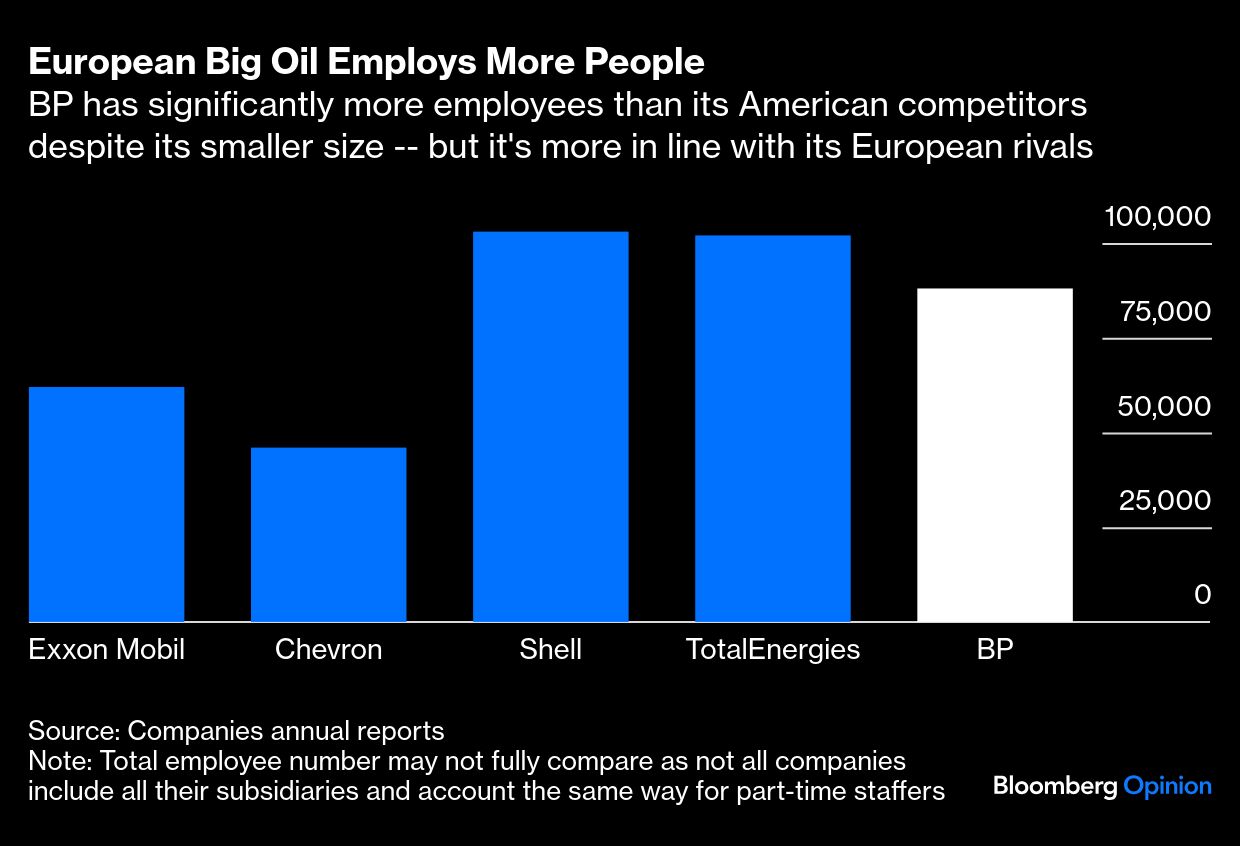

Fourth, management needs to cut costs meaningfully — and, yes, that includes significant, much needed job losses. While most of its rivals spend less today than they did in 2019, BP has done the opposite. Operating underlying expenditure reached $22.3 billion last year, up from $20.9 billion five years earlier. One reason is the costly bureaucracy that BP has built to run its green businesses, including a large number of staff. Today, BP employs nearly 88,000 people, compared with about 45,000 for Chevron. Notably, the latter is trying to reduce its staff by 20%.

If the British major takes all those steps, it will be able to reward its shareholders (including Elliott) while putting its balance sheet on a sound footing. Long-only investors have had a brutal time holding BP stock — not just since 2020, when the current failed strategy was announced, but for the last 15 years. It’s time BP thinks about the company’s owners.

Look at the sequence of events: For the first time since World War II, BP suspended its quarterly dividend in 2010 after the Gulf of Mexico’s oil spill. When it reintroduced it a year later, the payout was cut in half — to 7 cents a share compared with 14 cents before the oil spill. For a few years, BP slowly boosted the dividend, but then cut it again during the Covid-19 pandemic, reducing it to 5.25 cents a share, down 50%. At the time, then-CEO Looney said the move was “deeply rooted in strategy.” What nonsense.

Even today, after several quarters of dividend growth, BP shareholders get a payout of 8 cents a share, down more than 40% from the level of mid-2010. Over the same period, Exxon Mobil increased its payout by 135% and Chevron by 140%. Shell Plc, which also cut its payout during the pandemic, distributes a dividend today that’s just 15% lower than it was 15 years ago.

And that’s the problem. In an era when Big Oil doesn’t have many allies, particularly in Europe among generalist investors, dividends and buybacks are the only things that truly matter. We can discuss the ins and outs of strategy all day long, but that’s the path ahead.

Maybe the company had some other less radical and painful choices a couple of years ago, but now it’s too late. Incremental change won’t be enough. I warned in the past that BP was on borrowed time to change. An activist has become one of the largest shareholders, and many other investors, from the shadows, support it. If management and the board don’t deliver this week, I expect these parties will join forces to fire them. Time’s up.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.