Don’t believe the economic consensus, according to David Rosenberg. A recession is much more likely than a soft landing, and investors should allocate to 10-year Treasury bonds instead of stocks.

Rosenberg was the opening keynote speaker at John Mauldin’s Strategic Investment Conference, an event that I have attended for many years, both virtually and, in prior years, in person.

Rosenberg is the president, chief economist, and strategist of Rosenberg Research & Associates Inc., an economic consulting firm he established in January 2020. Prior to Rosenberg Research, he was chief economist and strategist at Gluskin Sheff and Associates Inc. from 2009 to 2019. From 2002 to 2009, he was chief North American economist at Merrill Lynch in New York.

Before we look at his latest predictions, let’s review what he said last year. In his opening keynote for this same conference, he forecast a 99% probability of a “hard” recession, and that earnings and multiple contractions will drive equity prices down 30%.

He was wrong. There was no recession, and the S&P 500 is up 22.6% over the last year. Indeed, as I noted in my article last year, the central predictions in his keynotes over the last four years have been incorrect.

Let’s look at what Rosenberg said about the economy and interest rates.

No soft landing

The title of his presentation was, “The Soft-Landing View is on Pretty Soft Ground.”

Rosenberg believes in the business cycle and that expansions always end in recessions. He believes in the power of interest rates (i.e., rate hikes) to influence the economy (i.e., cause a recession) with long lags.

He doesn’t believe in a soft landing.

Those in the hard-landing camp, like Rosenberg, are “on their back heels,” he said. “Everyone has thrown in the recession towel.”

But when everyone drops their hard-landing views, the next thing will be an anticipated recession, according to Rosenberg.

He made the case that last year’s GDP growth was due to non-recurring factors: fiscal stimulus, corporate spending, and debt-fueled consumer spending.

He attributed his incorrect forecast a year ago to missing the 25% expansion in the fiscal deficit last year, which contributed mightily to GDP growth. But last year’s expansion will be this year’s restraint, he said. There will be no fiscal policy stimulus this year.

Nominal GDP growth was 6% last year, but government revenue was down 7%. A lot of money went into “Potemkin” construction of manufacturing facilities, he said. But there is no production from those facilities, he said. “It’s a facade.”

The savings rate is a key economic indicator and has a big effect on GDP. Pre-COVID, it was 7.5 to 8%, but now it is 3.5%. That contraction added $1 trillion to consumer spending last year. Moreover, Americans historically spend half of their stimulus checks, but this time they spent all of it.

“We’ve become more narcissistic than ever,” he said.

That excess spending has ended.

Rosenberg doesn’t expect the corporate sector to contribute to GDP growth. Corporations need to refinance $7 trillion of debt in the next several years, and cap-ex growth has been flat.

Credit-card debt has grown by double digits, he said, and the average household has four credit cards. Debt-servicing costs relative to income is where it was heading into the last two recessions. The delinquency rate on consumer debt is at a 13-year high, equivalent to what it would be at a 9% unemployment rate.

Monetary policy and inflation

There have been three Fed tightening cycles that did not end in a recession: in the mid-1960s, 1980s and 1990s. Each time the Fed stopped tightening. Recessions happen 12-24 months after the end of a tightening cycle, he said. (Rosenberg did not say this, but the tightening cycle ended in July 2023, so that means we could still be a year or more away from a recession.)

Recessions also historically occur 26 months from the start of the tightening cycle, which in this case was March 2022. “The clock is ticking on this expansion,” Rosenberg said.

Rosenberg said inflation will recede dramatically.

Inflation was down 6% in the last 21 months, but Rosenberg is not convinced that the Fed is nervous about it (implying that monetary tightening is unlikely). Auto insurance, healthcare service and energy are the sources of inflation. Rent is also sticky, but it is coming down. The areas of inflation that are still in play are effectively “tax increases,” he said; they are not part of the business cycle. Those prices that are cyclical are already deflating.

Core inflation would be 1.9% if we measured it the same as in Europe, Rosenberg said.

The supply chain is less constrained than it was before COVID. There is tremendous capacity growth, and the labor force is growing; it is up 1.2 million workers over the past year. There are 500,000 more unemployed, but there is still a glut of workers. Productivity is up, which is deflationary.

Demand is lagging supply, and he predicted inflation would be 1% by the end of the year. “The pressure on inflation, broadly speaking, is subsiding,” Rosenberg said.

Rates are coming down

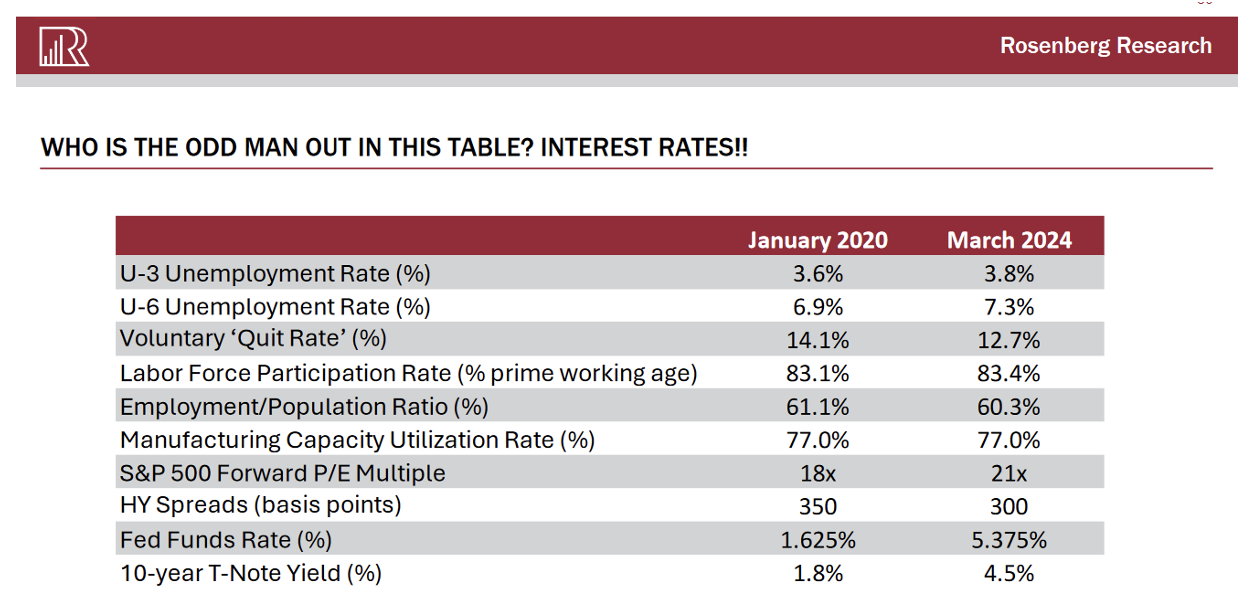

He presented the chart below, which shows a range of economic metrics pre-pandemic and now.

The takeaway is that the economy has not changed much since January 2020, but interest rates (the Fed funds rate and 10-year Treasury yield) are much higher now.

The equity-risk premium is less than 50 basis points; historically it has been 400 basis points. That is the lowest in the developing world. It will “mean revert,” he said, by a decrease in bond yields.

“You better be bullish on Treasury bonds,” he said, “because that is the only way the math makes sense.”

If we get the hard landing, he said, the Fed will cut rates by 500 basis points. If we don’t get a recession, the Fed funds rate is still too high. It is above the theoretical neutral rate (i.e., the interest rate if there was no unemployment or inflation).

It is an “easy call,” Rosenberg said, to invest in bonds. “It’s just a matter of a waiting game until the cuts come. The longer the Fed waits, the more cuts will be made.”

“The whole curve will drift lower,” Rosenberg said.

To illustrate the opportunity, he said that if 10-year yields go up 100 basis points this year, investors will lose only 3%. But if rates go down by that same amount, investors will gain 12%.

“I like that risk-reward tradeoff,” he said.

“If I am right on my forecast, 75% of the return will come from capital gains,” he said. “You will make equity-like returns without equity-like risk.”

Robert Huebscher is the founder of Advisor Perspectives and is a vice chairman of VettaFi.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.