Dueling economic reports whiplashed bond markets on Friday — for all the wrong reasons.

At 8:30 a.m. in New York, a hotter-than-expected US payrolls report sent yields on Treasury notes significantly higher, as traders bet that labor market strength would delay interest rate cuts from the Federal Reserve. About ninety minutes later, another report from the Institute for Supply Management seemed to send the opposite signal — that employment activity in the US service sector was contracting — and yields plunged. The series of events was a perfect encapsulation of two key lessons from the post-pandemic economy:

- The month-to-month data is very, very noisy.

- The bond market is still overly focused on labor market data (even though the Fed itself is laser focused on inflation, which has proved untethered from the unemployment rate).

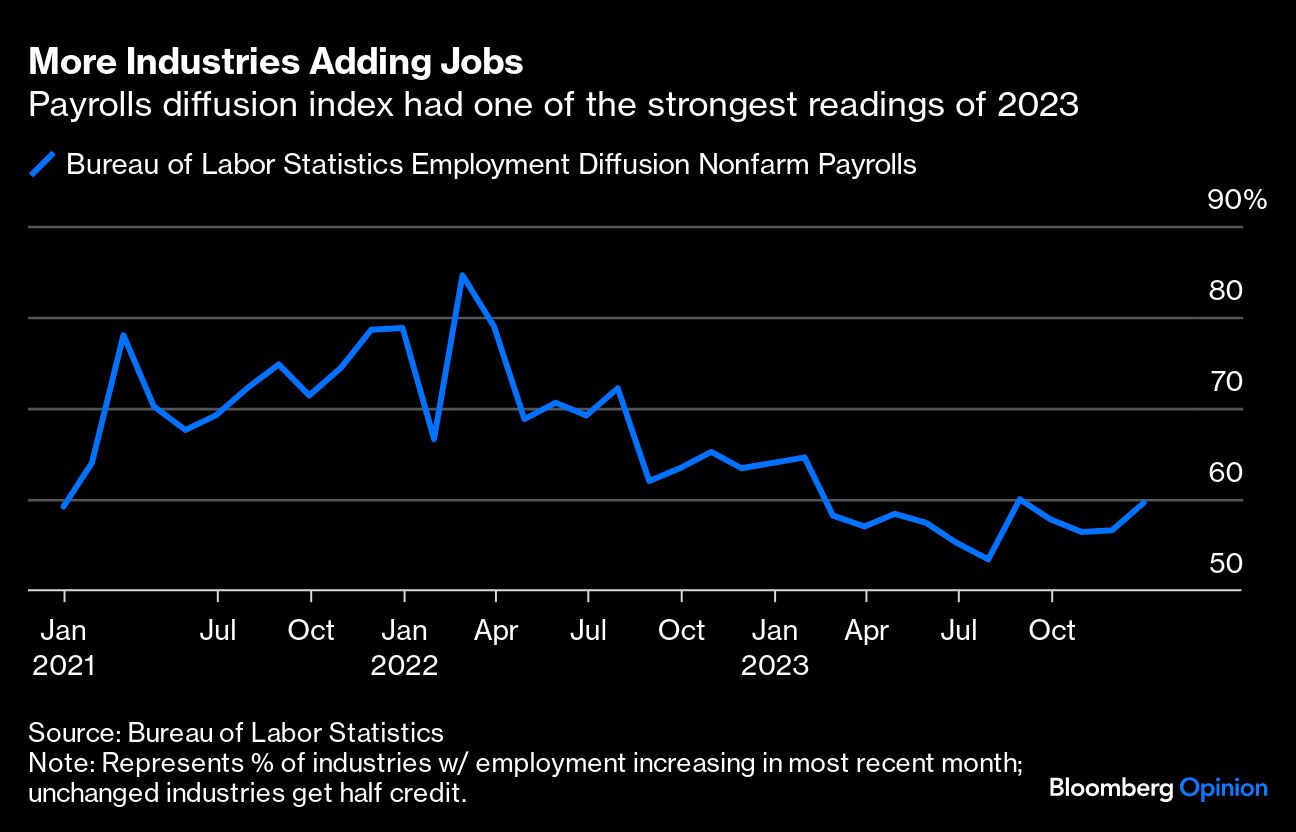

Let’s start with Friday’s data. The market day began with a Bureau of Labor Statistics report showing nonfarm payrolls increased by 216,000, better than the 175,000 that forecasters surveyed by Bloomberg had expected. What’s more, a measure of labor market breadth showed that the gains were shared by a broader set of industries.

There were some blemishes under the surface, of course — average weekly hours dipped and the previous two months’ payroll gains were revised lower by 71,000 — but the number was generally taken as a sign that markets had gotten ahead of themselves in pricing in a 25 basis-point rate cut in March. The futures-implied probability of a rate cut in March fell as low as about 54%.

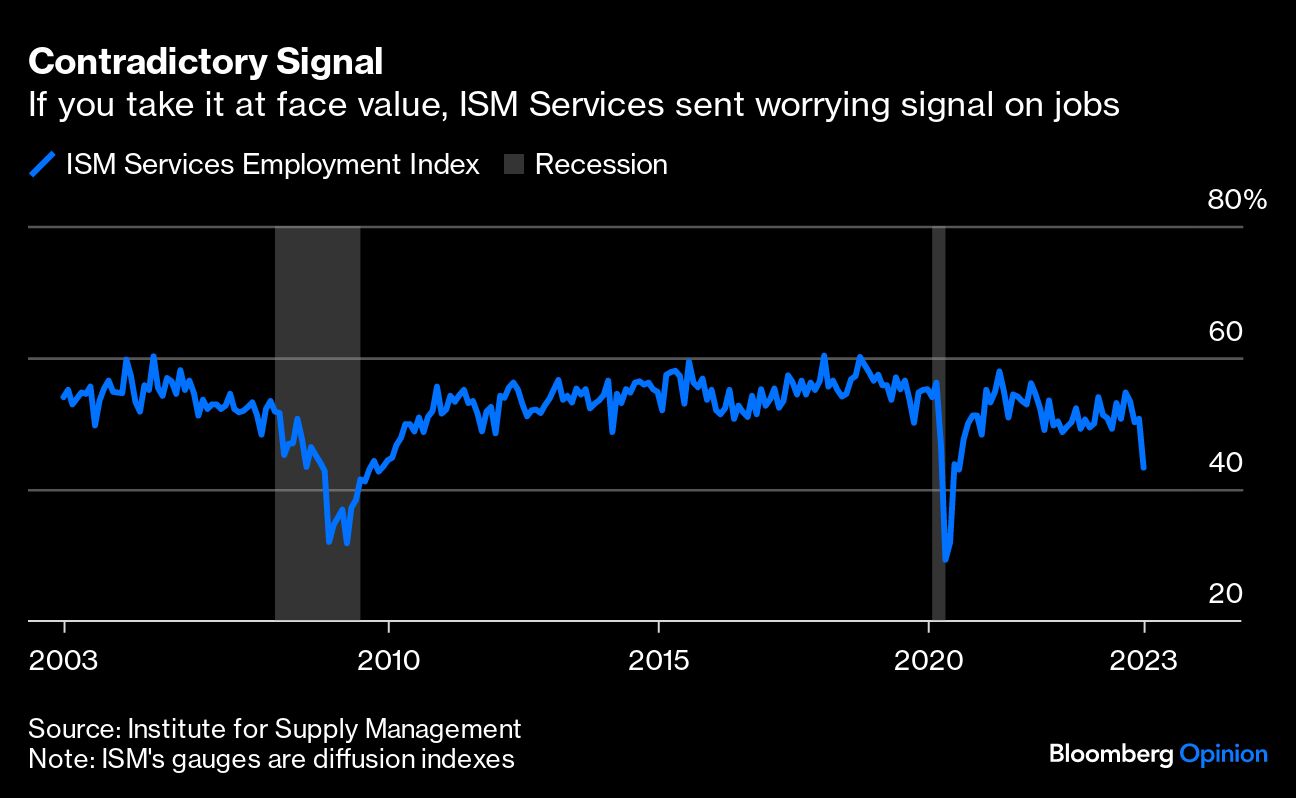

Then came the U-turn. At 10 a.m., the Institute for Supply Management revealed that — based on its survey of executives and purchasing managers — the US services sector nearly stagnated in December. The survey also suggested that employment activity in services contracted last month, posting the worst reading in nearly three decades outside of the periods around the Covid-19 pandemic and the financial crisis. Futures-implied odds of a March cut surged as high as 84% (only to reverse course again to be back at Thursday’s levels around 71% at the time of writing).

So which report are investors supposed to believe?

The short answer is: neither one in isolation. If there’s one thing the past couple of years have made clear, it’s that there’s extraordinary peril in placing much weight on any month-to-month data point. The panel size for the ISM survey is thought to be just about 300 ISM members with a possible bias for larger companies, according to an analysis by ISM competitor S&P Global Market Intelligence. Since small businesses employ about half of America’s workers, the size bias could partially explain the discrepancy between ISM and BLS figures. ISM also includes several categories (basically everything that doesn’t fall under “manufacturing”) that aren’t typically associated with services (i.e. construction and retail), the 2022 analysis showed.

Although the Bureau of Labor Statistics’ establishment survey includes 122,000 businesses and agencies at 666,000 worksites, the margin of error is still quite large. At a 90% confidence interval, all we know is that US employers added somewhere between 84,500 and 347,500 jobs last month. When compared to the previous month, that means labor market momentum might have gone up a lot — or maybe down a lot — but our best guess is that it’s somewhere in the middle.

In 2023 alone, the median month’s data was ultimately revised down by 45,000 jobs, with June’s number getting cut by 104,000 and July's getting revised up by 49,000. It’s hard to draw much signal from the initial reading, and we probably shouldn’t. But the bond market sure does!

On top of the data uncertainty, the market’s knee-jerk reaction also implies that there’s a clear and actionable relationship between labor market strength, inflation and — ultimately — central bank policy. Recent history has left me unconvinced.

Since January 2023, six-month annualized core PCE inflation has dropped from 5.2% to 1.9% even as the unemployment rate hovered in the range of 3.4%-3.8%, among the lowest readings in recorded history. As long as inflation trends continue, the Fed will soon have all the evidence it needs to start surgically reducing interest rates — irrespective of what’s happening in the labor market.

On the whole, I tend to believe that the market got the move right the first time — after the BLS report, but before ISM. As the saying goes, markets were “priced for perfection” heading into the report, with futures implying almost six rate cuts in 2024. It made sense for traders to inject some caution into that outlook.

Instead, a small-sample-size survey of purchasing and supply executives swung the market right back in the other direction, laying bare the inherent silliness of the entire episode. Ultimately, we still seem to be at the mercy of noisy data — based on the extremely tenuous belief that the labor market must necessarily dictate what the Fed does next. A labor market collapse would certainly spur deeper cuts than would otherwise be the case, but there’s no evidence that softer labor conditions are a precondition for easier monetary policy.

A message from Advisor Perspectives and VettaFi: The crypto landscape is on the brink of a revolution. Are you prepared for what's coming in 2024? Dive into expert insights on the future of crypto and its influence on next year's market. Join us at the Crypto Symposium on January 12th at 11 am ET. Click here to register.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin