Investment bankers must at times bore themselves with their talk of “strong pipelines” and “active conversations,” the ever-present characteristics of even the worst markets. But following a deeply disappointing 2023 for mergers, acquisitions and capital raisings, the new year belief in a rebound is more fervent than normal. After all, 2024 can’t be any worse, can it?

On the plus side, there really does seem to be a lot of pent-up activity waiting to break out — there were bursts of it already late last year. The expectation of a recovery has led bank executives to boost bonuses for unproductive rainmakers to stop them from quitting, while boutique advisory firms have continued hiring.

However, confidence among chief executives, investors and bankers will remain fragile and prone to evaporation at any sign of trouble. It’s likely to be a very stop-start year for deals of all kinds even if things go generally well.

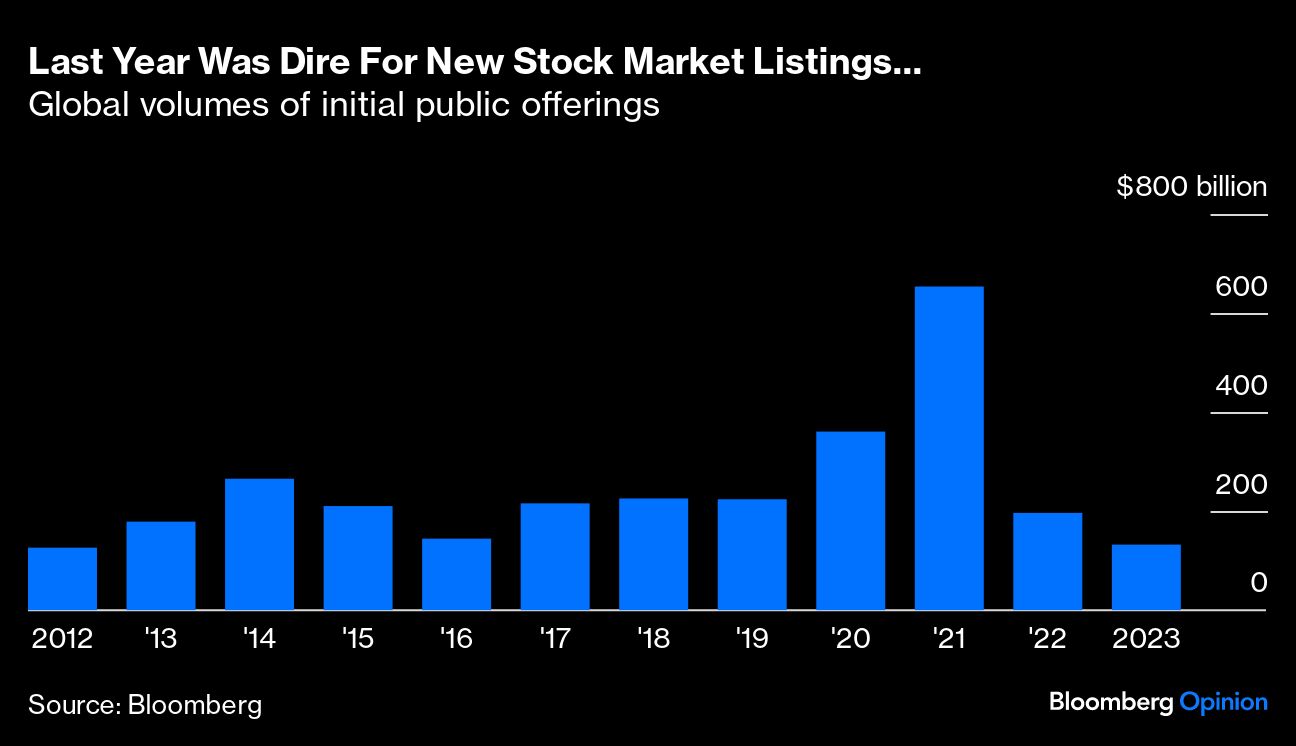

This is how last year ended, too. A short wave of initial public offerings in September and October brought four big share listings, including sandal company Birkenstock Holding Plc and chipmaker Arm Holdings Plc, before bankers and investors lost their nerve again. All four fell below their offer price and apart from Arm have struggled to recover. Total global IPO volume for 2023 of $132 billion was the worst since 2012, according to data compiled by Bloomberg.

October also saw the two biggest takeovers of the year — Exxon Mobil Corp.’s $68 billion acquisition of Pioneer Natural Resources Co. and Chevron Corp.’s $53 billion deal for Hess Corp. And yet, M&A for the full year was anemic, with global volume totaling less than $3 trillion for the first time since 2013.

A big part of the story was the near-total collapse of activity among private equity funds — and they face the same problems heading into 2024. Many need to sell mature investments and return cash to their backers in order to stimulate appetite for new deals, but the weak IPO market stands in their way.

Even if exits pick up, buyouts will be hampered by high funding costs. There is investor desire for loans: Sales picked up at the end of the year and prices in the US secondary market rallied as the Federal Reserve signaled that it was close to finishing its interest-rate increase cycle. As a result, banks should now be more comfortable underwriting debt even if they still have large unsellable deals clogging up their books, like the loans for Elon Musk’s buyout of Twitter Inc. (now called X).

However, there’s still a fair chance that rates won’t fall quickly. For private equity, that will mean a struggle to plot a path to strong returns through high debt costs and targets that aren’t necessarily cheap.

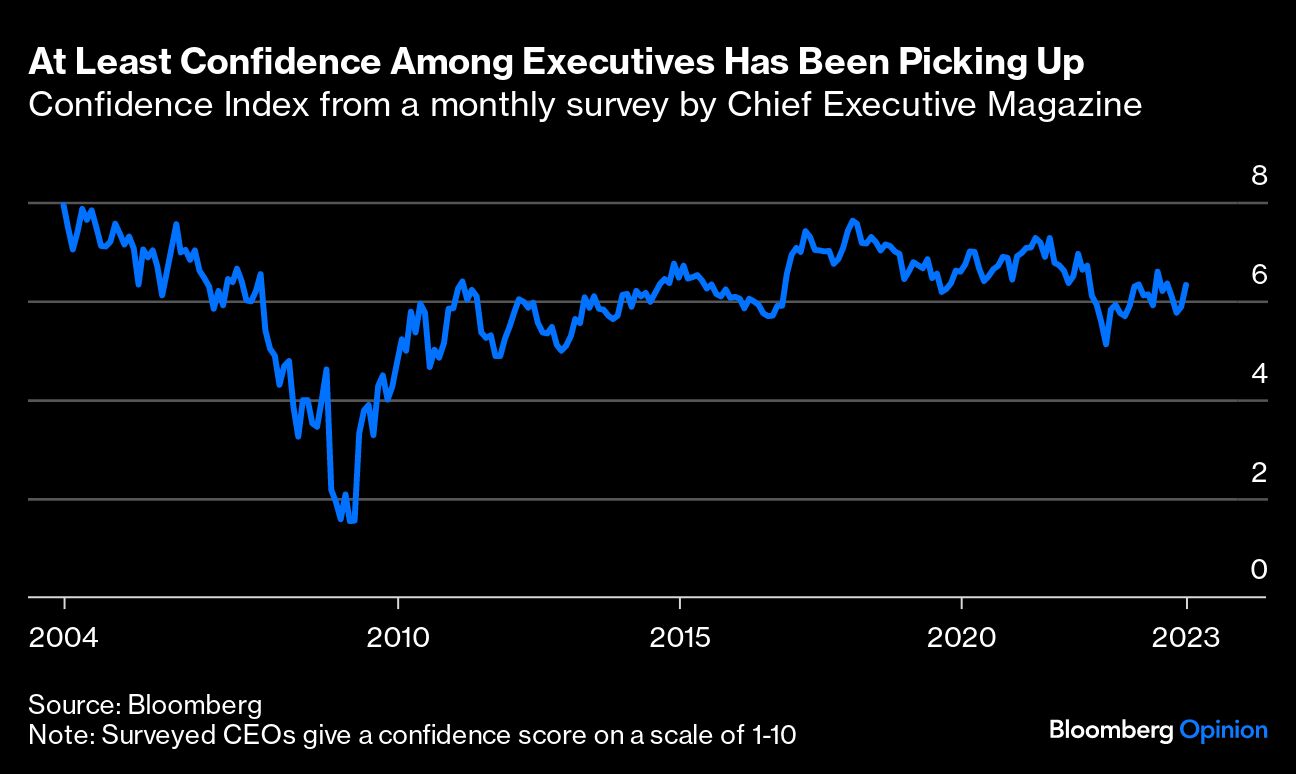

Bankers will have to hunt elsewhere for their fees. They’re pinning their hopes on corporate deals, especially among big, cash-generative companies in industries like energy, mining, chemicals and pharmaceuticals. Exxon and Chevron show what’s possible when executives have the conviction to press ahead with their strategic aims and growth plans — and the cash to do it. A big positive is the rebound in CEO confidence late last year, as measured by Chief Executive magazine’s monthly survey. If US business leaders keep believing in some form of a economic soft landing in 2024, they’ll be more likely to look through short-term volatility.

But there will be plenty of that! The first few days of the year have already seen stocks and bonds pare December’s gains. In futures markets, investors have been betting heavily on interest-rate cuts coming quickly. That might not happen if the last bit of inflation proves difficult to squash as some expect, given ongoing pressure in services and wages. If rates do fall fast, it could be for the bad reason of a looming recession rather than because inflation is dissipating painlessly.

Investors and markets are going to remain acutely sensitive to each bit of fresh economic data until there has been a long run of solid news in the same direction. My bet is that there will be surprises ahead: Windows of relative calm will see bursts of activity, but then something will turn up to make everyone wary once more.

On top of all that, there are a host of major elections this year, not least being the scrap for the US presidency. As Stephan Feldgoise, Goldman Sachs Group Inc.’s global co-head of M&A, said on the bank’s Exchanges podcast last month, election years are typically down years for deals.

Assuming interest rates have at least stopped rising, this year ought to be better than last for bankers squeezing real work out of their healthy pipelines and dialogues. But it probably won’t be until the second half before we can be sure that‘s the case — and in truth there are enough economic and political dangers to slam all of this into a ditch at any moment.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies