Tweedy Browne: This is the Best Opportunity Set in 20+ Years

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTweedy, Browne Company LLC, based in Stamford, CT, is a value-based asset manager with an investment philosophy based on the work of Benjamin Graham. It was originally a broker, and one of its clients was Graham, co-author and author of the seminal textbooks on value investing: Security Analysis (1934) and The Intelligent Investor (1949). The firm also had brokerage relationships with Walter Schloss and Warren Buffett. Tweedy, Browne established its first investment account in the late 1950s, and began managing value oriented separate account investment portfolios in 1975 after registering as an investment advisor. The firm established its first mutual fund in the summer of 1993, and today serves as investment advisor to four mutual funds including its flagship, Tweedy Browne International Value Fund. It ceased operations as a broker-dealer in 2014.

As of September 30, 2023, its flagship fund, the Tweedy, Browne International Value Fund (TBGVX; it was previously called the Tweedy, Browne Global Value Fund until its name was changed effective July 29, 2021), has returned 8.28% annually since its inception in 1993. That is 180 basis points better than the hedged MSCI EAFE index and 255 basis points better than the foreign stock fund average (which is calculated by Tweedy, Browne based on data provided by Morningstar and reflects average returns of all mutual funds in the Morningstar Foreign Large-Value, Foreign Large-Blend, Foreign Large-Growth, Foreign Small/Mid-Value, Foreign Small/Mid-Blend, and Foreign Small/Mid-Growth categories).

I interviewed six members of Tweedy Browne’s investment team: Roger de Bree, John Spears, Tom Shrager, Bob Wyckoff, Jay Hill and Andrew Ewert.

The interview took place on November 17 over Zoom. I previously interviewed several members of the Investment Committee at Tweedy, Browne on February 5, 2019, when we discussed their investment philosophy, how they differentiate themselves, and their views on currency hedging. Please refer to that interview for information on those topics.

This interview contains forthright opinions and statements on securities, investment techniques, economic and market conditions and other matters. These opinions and statements are as of the date indicated, and are subject to change without notice. There is no guarantee that these opinions and statements are accurate or will prove to be correct, and some of them are inherently speculative. The adviser may be wrong in its assessment of a security’s intrinsic value. The information included in this interview is not intended, and should not be construed, as an offer or recommendation to bury or sell any security, not should specific information contained herein be relied upon as investment advice or statements of fact. This interview does not contain information reasonably sufficient upon which to base an investment decision.

The fund has a low annual turnover, implying that your average holding period is approximately 14 years. Is that reflective of the fact that your performance should be viewed over long timeframes?

Bob Wyckoff: I think I speak for the group when I say that we believe long-term, value-added performance is more indicative of skill than performance over very short periods of time. Long-term records are important. Our clients are interested in longer-term results to fund a good retirement.

But by no means when we look at a security are we saying to ourselves, "We plan to own the security for 14 years." We're buying that security at a discount to intrinsic value. We tend to stay with it, assuming the intrinsic value holds up, and wait for that spread to close. If it closes, then we have a decision to make whether to continue to hold or to sell the security.

If it's a better business that compounds its intrinsic value over time, we'll often stick with it. In our portfolios, we have companies like Nestle, Diageo, and Heineken that we've owned for 10- or 15-plus years and in some instances even longer than that. But we'll own other companies where the price to intrinsic value gap closes more swiftly, and we may exit our position sooner. But I would say on average, we tend to own securities for three to five years or longer.

That 14-year average holding period you mentioned is going to move around as the portfolio changes character over time.

Roger de Bree: It's also the old thing about the stock market being a voting machine in the short run and a weighing machine in the long run. We try to be rational players. We think of ourselves a little bit as microeconomists trying to establish the value of companies.

Roger de Bree: It's also the old thing about the stock market being a voting machine in the short run and a weighing machine in the long run. We try to be rational players. We think of ourselves a little bit as microeconomists trying to establish the value of companies.

Because we don't play the sentiment game, it takes time – often a long time – for these values to be recognized. It can happen very quickly, which is better, but it can take a long time. Ultimately, we play for long-term rationality in the market, and we don't play for the next hot microchip stock or something like that.

That also drives why this turnover is so very low. If you want to do microeconomics and if you want to buy things cheaply, it takes time and discipline to see your values realized.

Jay Hill: Every manager should be evaluated over very long timeframes.

Jay Hill: Every manager should be evaluated over very long timeframes.

Regardless of whether they have a high or low turnover, or a long or short holding period, every manager should be evaluated over very long periods of time because in the short term, there's too much randomness.

The fund has outperformed its benchmark in every calendar year when the benchmark had negative returns. To what do you attribute that? Is that some aspect of the capital structure in the companies that you're buying, or the process in which you select securities?

Jay Hill: I'd say two things. First, we insist on balance sheet strength when we buy a new company. If you study our portfolio, we have many companies that have net cash on their balance sheet. Most of the companies that we own would be considered to have investment-grade rated debt. They are companies with strong balance sheets that can self-finance themselves.

They don't need access to the capital markets when times get tough. That helps during downturns. We're not worried about companies breaking debt covenants, or losing companies to creditors in downturns. It's also a function of buying low-expectation stocks.

They're generally cheap because there's problems, risks, and very low expectations. If you own low-expectation stocks, they probably hold up better when the entire stock market is falling, because the bad news is largely already reflected.

Roger de Bree: We don't tend to fish in the recent high ponds where, if the market falls out of favor, yesterday's darlings become today's ugly witches. We don't skew ourselves to a large disappointment because we don't buy stocks that are expensive or up a lot.

Low valuations, which imply low prices, give us a lot of protection.

Andrew Ewert: Our currency hedging can also be a benefit, given the dollar tends to strengthen in times of stress, in a flight to quality or to safety.

U.S. stocks outperformed foreign markets for more than a decade until 2022 when that trend reversed. Do you think international stocks will continue to outperform U.S. markets in the year ahead? Are they cheap now? Last year when we spoke, you said you were actively shopping in China, Japan and Europe. What positions have you added in those regions?

Jay Hill: Generally speaking, if you look at the broad-market valuation ratios, it's quite clear that international stocks are cheaper than stocks in the United States. Just look at overall P/E ratios; they're much cheaper outside of the United States. It's also true if you adjust for the mix in the different types of companies that make up the indexes.

Some people argue, "Well, the United States deserves to trade at a premium to, let's say, the UK stock market on a P/E basis because the U.S. has many growth-tech or faster-growing businesses and fewer banks and insurance companies. The UK has a greater weighting to these lower-multiple sectors like banks and insurance companies.”

But we've found that even if you look at companies in the exact same industry, a U.S. and a European company, the European company is almost inevitably cheaper.

Here's a recent example. There's a company called CRH whose primary listing was on the London Stock Exchange, but a lot of its revenue is derived from the United States. It recently changed its primary listing from the London Stock Exchange to the NYSE, and by doing that its stock has gone up over 20%.

Many of the funds that bought the company did so because, "Hey, when it's primary listing is in the United States, it's going to become a part of the U.S. indices." In the U.S., the company's going to trade at a higher multiple. The company has been at a disadvantage by being listed in the UK. Think about that. Nothing changed with the company – nothing.

That tells me that there's inefficiencies on international exchanges.

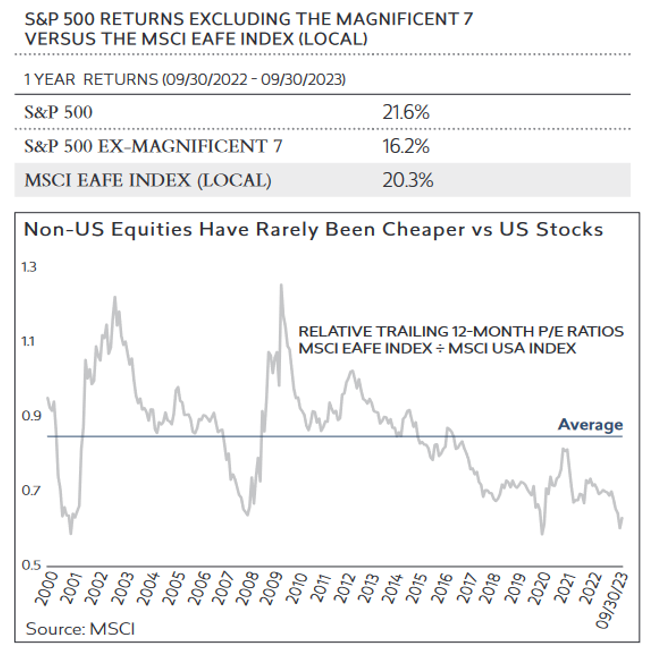

Bob Wyckoff: We have a chart that shows non-U.S. equity valuations relative to U.S. equity valuations over the last 20-plus years, looking at the trailing 12-month P/E ratio for the MSCI EAFE Index versus the MSCI USA Index. When you look at that chart, non-U.S. equity valuations appear to be, on a relative basis, very compelling. And the performance of non-U.S. equities has begun to perk up relative to their U.S. counterparts. If you were to strip out the returns of the “Magnificant 7,” (Amazon, Microsoft, Apple, Meta, Alphabet, Nvidia and Tesla), mostly tech related companies, from the return for the S&P 500 over the past year ending September 30, the MSCI EAFE Index would have outperformed the S&P in local currency.

Non-U.S. equities have rarely been cheaper relative to U.S. equities over the last 20-plus years. The last time they were as cheap as they are now was briefly in 2020 during the pandemic, and during the financial crisis in 2008. As of November 30, 2023, the price/earnings ratios of the MSCI USA Index and the MSCI EAFE Index were, 23.9X and 14.4X, respectively, providing earnings yields of 4.18% and 6.94%, respectively. The dividend yield of the MSCI EAFE Index was 3.14% vs 1.5% for the MSCI USA Index.

We've also done some work looking at rolling 10-year compound returns for the S&P 500 and the EAFE Index going back to the mid-1970s. We have a calculation for this through the first quarter of this year. Approximately 54% of the time, the S&P 500 outperformed in rolling 10-year periods. Approximately 46% of the time, the EAFE Index outperformed. We've just been through an extraordinary period of outperformance by U.S. equities over the last 10-plus years.

It’s anyone’s guess but if the historical pattern holds, we could be looking at a period over the next 10 years where non-US equities do well.

Jay Hill: The second part of your question was examples of stocks that we've added in Europe, China and Japan.

SKF is a ball bearings company based in Sweden. It was a company that, at least at the time of purchase, was trading at a big discount to a similar company in the United States that competes in the same industry.

Roger de Bree: SKF is by far the best and strongest player in ball bearings in the world. What it has discovered, and this would not be rocket science, is that making ball bearings for passenger cars is a very tough game in which there are some German and a lot of Japanese companies. They're all long-term bleeders of shareholder wealth.

What SKF did a long time ago was focus on replacement bearings for niches: agriculture, trains, airplanes, trucks, all kinds of medical things, marine applications. There are many more. A big part of the business is replacement bearings; that's selling bearings to wholesalers. It's a very high-return business. The post-tax returns are approximately 20%.

It's not a business that grows a lot, although there are always some things that will expand. Right now, aerospace, trains and trucks are strong and expanding. Then, of course, they do some bearings for cars, but they don't make money on it. But they are ahead of the game in bearings for electrical cars, which are heavier bearings because these cars are heavier, so they need stronger bearings.

There's also the idea of remote monitoring of bearings, especially very critical bearings, because they need maintenance or greasing now and then. On very valuable bearings, and there are some truly expensive bearings, you have remote monitoring of how they're doing, and some are just amazingly complex things. Think about the bearings on a reel that puts out a fishing net.The pressures applied to bearings are enormous. They move in all directions, so you better have a good product. They are more and more remotely monitored.

Assuming a valuation of 12x normalized EBIT, we valued SKF at 220 to 240 Swedish krona per share.

That's not a very high valuation multiple for what this is. There had been some insider activity also by the controlling shareholder, which is the Wallenberg family via their vehicle called Investor AB. Those were significant insider buys, so we liked that. We paid around 160, thinking it was worth 240 even without huge growth.

The opportunity was created by COVID, and that is a theme that runs through a lot of our recent buys. COVID threw a spinner in the wheels of many strong businesses, because of the inflation of input costs and logistical problems. If you made something, then your inventories were going up because you had to buy ahead your raw materials. You couldn't ship out what you had made, but you wanted to make sure that you had what clients wanted.

All of this made inventories go up, which was bad for free cashflow. There was demand interruption and high inflation of input prices. In that environment, which is just a speed bump and not a permanent impairment of these business models, we were scouring the globe for the strongest companies in a lot of industrial businesses. We bought many. That was the gift of COVID, as far as we are concerned.

The past decade has been very tough for many value investors. We discussed this last year. You said that it was due at least partially or mostly to artificially low interest rates. In your third quarter report to shareholders, you wrote, "… we continue to believe that we are in the midst of a tectonic shift in markets, catalyzed in part by the war in Ukraine and pandemic-related supply shocks, but driven primarily by a stubbornly persistent level of core inflation and interest rates that over time are likely to normalize higher than the zero bound levels of the last decade." With rising interest rates, has that created a richer opportunity set for you?

Jay Hill: It has. The best opportunity set I've ever seen in my career was 2008/2009 and then in 2020. Those were the two best times, but higher interest rates are starting to lead to multiple compression.

Trading and M&A takeover multiples are starting to feel the impact of higher interest rates, and so multiples are coming down. In general, there are more ideas that hit our screens. If you have a screen set to look for stocks that are trading below, let's say, an enterprise value to EBIT of less than 10x, there are more names hitting those screens.

Our approach is to buy companies at a discount to private market value, with private market value being defined as what would the business be worth in a deal. We study deal multiples, and we're just now starting to see lower deal multiples. It’s the first time I've observed meaningfully lower deal multiples being paid in over 10 years.

So on one hand, we're seeing more stocks trading at lower multiples. But it's probably also true that what a business is worth on a multiple basis is less today than it was 18 months ago because of the rise in interest rates.

Tom Shrager: It's a little bit hidden by the fact that there are fewer M&A transactions being done. Investment bankers are pretty upset about their bonuses.

Bob Wyckoff: In an environment where higher interest rates are putting pressure on valuations, the price you pay for a security matters more than ever.

It becomes relevant again, as opposed to an era of zero interest rates where a stock trading at 50 times earnings looked like a value compared to a zero level of yield on a competitive, risk-free, fixed-income instrument.

We're enthusiastic and optimistic about what the next decade holds for us. Unfortunately, it is a result of a rise in interest rates.

John Spears: The downside is that everything we own is now becoming intrinsically less valuable. It's worldwide.

John Spears: The downside is that everything we own is now becoming intrinsically less valuable. It's worldwide.

While we're on the subject of the opportunity set, last year when we spoke, you said you were looking at adding small- and mid-cap positions that were becoming attractive at that time. Can you give an example of any that you've added since then?

Jay Hill: Winpak is a packaging company that is cheap on an absolute basis and relative to M&A comps. It's a business that has very high margins and high returns on invested capital. It has an extremely strong balance sheet – 28% of its market cap is in cash, and there's zero debt. It's also a business that's had material insider buying.

This company has one of the best statistical fact patterns that I've seen in my career. It's a company that's based in Winnipeg, Canada. It has a market cap in U.S. dollars of 1.8 billion. While this company is listed in Canada, it's really a U.S. business, because 80% of its sales are derived from the United States.

This is a company that makes mostly plastic packaging for the food and beverage industry. When your readers go to the grocery store and buy a package of bacon, there's a 60% chance that the packaging was made by Winpak.

Winpak makes 60% of the bacon packaging in the United States and 100% of the bacon packaging in Canada, and its product line extends to all types of foods and beverages. 90% of sales are related to food and beverage packaging.

The key attributes of its products are to extend the shelf life, preserve freshness, and eliminate odors and leaks in packaging. The company has a great long-term track record of growing organically. It has very high margins, amongst the highest margins of any company in the packaging industry. It has high returns on invested capital.

This company's never taken a one-time charge, which to me is very rare and admirable. When it reports its financial statements, there's no, "Hey, we really made this, but you should look at the adjusted numbers and exclude the bad stuff."

It's a company that has a fortress balance sheet, with a big net-cash position. 11 different insiders have purchased shares with their own money, $6 million worth of stock at an average price of around $38 to $39 per share, approximately equal to the current stock price.

At today's stock price, the company trades at 5.6x enterprise value to EBITDA, or 7.0x enterprise value to EBIT, and has a P/E of 12 times. I looked at M&A deals among food & beverage packaging companies, and I found eight very good, comparable transactions. If you look at the average enterprise value to EBITDA multiple paid in those eight transactions, it was 11x EBITDA.

The range was from 8x to 14x, but an average of 11s. Winpak trades at a substantial discount. If Winpak were sold in an M&A transaction tomorrow, my estimate is they'd get 10x EBITDA.

If you assume 10x EBITDA, which is a discount to where the average M&A comps have occurred, the business would be worth roughly 60 Canadian dollars per share.

One of the big reasons why this stock is cheap and why other investors aren't as excited about it as I am, is because of capital allocation. This is a company that has what I would call “Japanese” capital allocation. It generates cash and the cash builds up on the balance sheet. This company pays a tiny recurring dividend; it has paid three special dividends in its history.

Winpak is a perfect candidate for share repurchases. We think it makes incredible sense for it to buy back its shares as opposed to paying another special dividend. That, in our view, is the greatest way to increase the intrinsic value of the business. I'm hopeful that the company may rethink capital allocation.

Frank Hawrylak: We've bought a number of small- and mid-cap stocks in Europe and Japan. We've been active in the markets. While it's hard to watch the stocks go down, the framework allows us to lean, and that's what we've been doing. Those stocks were characterized by insider buying and statistically pretty cheap valuations.

Frank Hawrylak: We've bought a number of small- and mid-cap stocks in Europe and Japan. We've been active in the markets. While it's hard to watch the stocks go down, the framework allows us to lean, and that's what we've been doing. Those stocks were characterized by insider buying and statistically pretty cheap valuations.

What is your cash position relative to historical levels?

Frank Hawrylak: Cash fluctuates a little bit, but we've been in the 3% to 5% range across the funds. We sometimes let it go a little bit lower than that, but that is where we are now.

Jay mentioned insider buying in the context of the position that he was discussing. Last year, we spoke about research that you were doing on that topic, looking at C-level purchases above a certain amount. Where has that research taken you over the last year, and how have you been able to put that to use?

John Spears: We recently finished a study of insider buying around the world, looking at C-suite, insider purchases. We had the date of the purchase, the amount of the transaction and the title of the insider. We have had a historical file that included the United Kingdom, continental Europe, Australia, Canada, and of course, the United States and Singapore, Hong Kong and South Korea.

The study was for approximately a 22-year period. We looked at holding periods of six months, one year, two years, and three years. To sum it all up, we found that if you have certain characteristics in combination with the insider behavior, there is an insider signal. Insiders tended to beat the market by about 10 percentage points a year relative to various benchmarks.

In the United Kingdom, it was the FTSE 350. In Europe, it was the STOXX 600 Europe Index, In the United States, the S&P 500. Then for a grab bag of all the other companies, we were able to convert their foreign currency returns into U.S. dollar-equivalent returns. Then we used the MSCI World Index as the benchmark, which of course, is based in U.S. dollars.

As a group, if we could get anywhere near that eight to 10 percentage point return in excess of these market cap-weighted indexes, it'd be just wonderful.

ETFs have become increasingly popular. They're about 20% of the market, a fifth the size of mutual funds. But much of the flows, particularly this year, have gone to actively managed ETFs. How are you able to compete with ETFs, and do you have any plans to introduce an actively managed ETF?

Bob Wyckoff: For tax-paying investors, ETFs are formidable competitors. We service a lot of tax-paying investors, so it's fair to say we have an interest in this topic. We're studying this topic. Stay tuned because we're very interested.

Taxes don't show up in expense ratios. They're a hidden cost of investing. We're interested in producing attractive after-tax returns given the structure of our client base. Not all of our clients are tax-payers, but many, if not most, are.

Jay Hill: We are.

Bob Wyckoff: We are, of course, and we eat our own cooking here at Tweedy.

Last year, I asked you about the risks that you were most concerned about, and your response was you were worried about rising corporate tax rates and the possibility of Russia turning off its gas supplies to Europe. Those seem insignificant compared to what we face today, particularly the situation in the Middle East where Israel is fighting a battle on five fronts. The U.S. is involved, and Iran has proven to be an underlying, destabilizing force and a source of funding for terrorism. Do you share my view that the geopolitical risks now are far more elevated, and does that factor into your approach to investing?

Andrew Ewert: They're always elevated in some ways. It's just a matter of the circumstances. There was a fear that Europe last year would run out of gas last year as a result of the Russian gas was related to the Ukraine war, which is obviously still with us today.

These events can create opportunities and dislocations … fear can breed bargains.

Roger de Bree: You have to distinguish between the terrible things that happen in all these places and how it affects economies. Some of our companies have had to withdraw from Russia. That has been painful in some cases and maybe a little bit less painful in other ones. But none of this, terrible as it is, and cruel as that sounds, has in a major way affected the world economy.

The political climate in China has had a big effect. That doesn't make the headlines in such a spectacular way, but that's more impactful for the businesses we own.

If major fighting breaks out in the Middle East, that will be terrible. What has happened so far is terrible, but will it sink the businesses of most our investments? I don't think so.

John Spears: The geopolitical picture with Iran, North Korea, Russia and China, with the dictators of the world joining up is terrible. But what are you going to do? You still have to buy things.

You're not going to have major businesses trying to sell off their plants and trucks, and buy gold bars, as if that will help. The businesses will adapt as well as they can, and we're going to try to adapt as well as we can.

Roger de Bree: There are side effects of the side effects. The gas prices in Europe were a real thing for many companies. I remember speaking to CEOs, many of whom, were saying, "I buy a lot of gas and it's 10X compared to a year ago. What do I do?" That's closer to home for us.

Bob Wyckoff: Bad macroeconomics often translates into investor anxiety, which often translates into opportunity. Ben Graham had this wonderful parable called Mr. Market. The ultimate lesson from the Mr. Market parable is that markets are here to serve us as investors, not to guide us as investors.

Difficult macro environments often create opportunity, as they create a level of sturm and drang, and overreaction.

John Spears: You have to be an optimist. Let's say there's nuclear war. Well, what's cash going to do for you? If there's nuclear war, bye, because God doesn't take cash. Who cares?

Bob Wyckoff: John’s referencing a firm war story from the 1960s. We had a partner, Joe Riley, who was at the trading desk. Howard Browne either was going to lunch or coming back from lunch, and he saw Joe Reilly furiously buying stocks. This was during the Cuban missile crisis, as the Russian ships were on their way to Cuba with the missiles.

His question to Joe was, "Joe, how can you be so confident we're not going to face nuclear war here? Why are you so eager to buy securities?" Joe said, "Well, either the world is going to come to an end, and it's not going to matter for any of us, or this is going to be one of the greatest buying opportunities of all time." It turned out to be the latter.

Many investors are looking at short-term Treasury yields of 5% or more and are questioning why they should take on the risk of equity investing. What guidance do you offer those investors?

John Spears: Look at your after-tax return for tax-paying investors. Look at your after-inflation return and after taxes. You get a much better shot in equities.

Jay Hill: The way I've always thought about it is we're trying to buy companies for 70 cents or less on the dollar, and we're hoping that the business is worth a dollar. If you buy a business at 67 cents and it goes to a dollar within a reasonable timeframe, let's say four or five years, it's roughly a 50% return.

If that 67 turns into 100 in less than 5 years, your annual return is over 10%. I've always felt like equity investing is about attempting to make a 10% return. The long-term nominal return for equities over the last 100 years is something like 8% or 9%.

That's still quite a bit above 5%, but you are right. You can get 5% now with zero risk, at least pre-tax. That is one of the reasons why there's going to be multiple compression, because there's an alternative that is attractive to some.

John Spears: If you buy a dollar for 67 cents and sit with it, let's say it goes four years, you've got some chance with diversification that some of them will grow. Not necessarily 20% a year, or anything like that, but they'll chug along.

In the meantime, they are paying dividends. It's not like having a coupon where you know exactly what you're going to get. But the odds are very attractive if things work out.

Frank Hawrylak: That 5% yield that you get from a short-term, fixed-income instrument implies you're paying 20-times earnings for something that doesn't grow. I could create a portfolio of dividend-paying stocks that yield around 5%. That's without them paying all their earnings out as dividends, so they are reinvesting a portion of their earnings.

Or if you start buying things at 10 to 15 times earnings and that money gets reinvested, you have a better shot over time of beating a 5% hurdle rate.

I think about the mathematics that way. That doesn't mean you shouldn’t park your money for a little bit. But with a 5%, one-year instrument, you are taking risks beyond what John says in terms of after-tax returns and inflation. There is a reinvestment risk as well. You don't know what that's going to look like when that security matures.

Compared to the alternatives, there's plenty of things in the stock market that can get you a better return than 5%.

Robert Huebscher is the founder of Advisor Perspectives and a vice chairman of VettaFi.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits