Jeremy Siegel: Expect 10% to 15% Returns on Equities in 2024

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Jeremy Siegel is the Russell E. Palmer Emeritus Professor of Finance at the Wharton School of the University of Pennsylvania and the senior economist at WisdomTree. His book, Stocks for the Long Run, just published its sixth edition, is widely recognized as one of the best books on investing. It is available via the link on this page. He is a “Market Master” on CNBC and regularly appears on Bloomberg, NPR, CNN and other national and international networks.

Jeremy Siegel is the Russell E. Palmer Emeritus Professor of Finance at the Wharton School of the University of Pennsylvania and the senior economist at WisdomTree. His book, Stocks for the Long Run, just published its sixth edition, is widely recognized as one of the best books on investing. It is available via the link on this page. He is a “Market Master” on CNBC and regularly appears on Bloomberg, NPR, CNN and other national and international networks.

This is my 16th annual interview with Jeremy, which in the past we have done just before Thanksgiving. He has been one of the most prescient forecasters among those featured in Advisor Perspectives. You can access our prior interviews here: 2022, 2021, 2020, 2019, 2018, 2017, 2016, 2015, 2014, 2013, 2012, 2011, 2010, 2009, and 2008.

This interview is an abridged transcription of the opening keynote session of the Market Outlook Symposium on December 14.

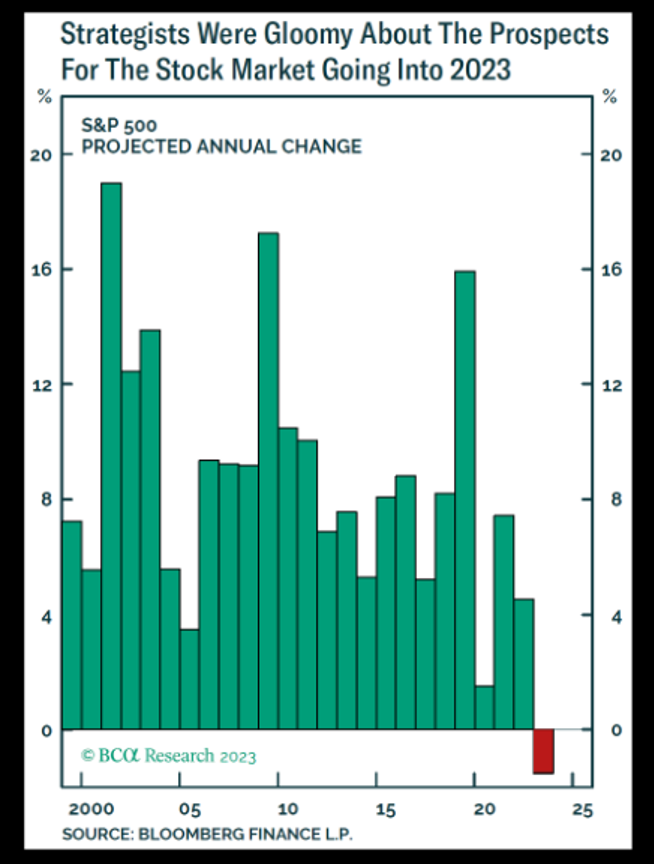

We spoke on December 13 last year, so this is one year and a day since that interview. The S&P closed at 3,991 on that day, and yesterday it closed at 4,566, which is a gain of 14.4%. You correctly predicted that gain when you said last year, “I have never seen so much bearishness in the market, which is a great sign for stock investors.” You said the market was 10% to 15% or more undervalued, and that you would not be surprised to see 4,600 or more by December, where we are now. Yours was also a contrarian view. According to Bloomberg, going into 2023, of the 25 strategists it surveyed, only three predicted S&P returns of more than 14%. More than half of them forecast returns of less than 8%.

Congratulations. Now the S&P forward P/E ratio is nearly 21, and earnings on the S&P were $181 as of June. What is the fair value of the S&P 500?

It's been a pleasure to talk to you over all these years.

What a market. Just last night, the Dow surged to an all-time high. I'm sure the S&P is going to follow with the dovish pivot by Powell, which is very appropriate. I am very bullish for 2024.

We must understand that we have had a tale of two markets this year. The so-called “Magnificent Seven” were up 100%. The Russell growth stock index was up 43.5%, but the Russell value stocks were up only 9.79%. So, those seven stocks really pushed this market up. This was a big change from 2022, when growth stocks collapsed.

In 2024, I believe we're going to have a reversal. The value and small stocks are finally going rouse from their lethargy and be the winners over the next year. I'm not saying these large-growth stocks won't do well. They've got incredible franchises and growth prospects. But I'm bullish on small- and mid-cap stocks, which have much lower prices. I believe the overall market will be up 10% to 15% from today's level by the end of 2024.

The money supply, as measured by M2, declined from December of last year until April of this year, and it has been flat since then. You were critical of the Fed last year for its monetary tightening. This year, inflation has subsided, as you correctly predicted. Was that a result of the decrease in money supply, higher interest rates, or a reduction or elimination of supply-chain issues? Core CPI is 4.0% and headline is 3.2%. What is your outlook for inflation?

You're right, I was critical of the Fed. I was worried when I saw the money supply decrease. Money began to increase somewhat toward the middle of the year. But now, it has turned down again. That's why I welcome this pivot by Powell. We should get lower interest rates in 2024. We've got to get liquidity growing again with M2 growth going back to 5%, consistent with inflation back to 2 to 2.5% and real growth at a similar level.

Inflation has gone down because of higher interest rates and lower money-supply growth. The supply-chain constraints normalized as well. But I'm going to say the tightness of the money supply was the main reason the inflation rate fell.

I thought the Fed was tightening too quickly. But I have been surprised at the resilience of the economy to the stagnant money supply and higher real rates. I thought that we would see a bigger downturn because of the Fed’s monetary policy. I'm very pleased, of course, that there hasn't been a recession. The indications for a soft landing are certainly increasing. I would say the odds of a recession are less than 50-50 for 2024.

Inflation will be sticky. But it'll be down to the 2.5% range by the end of next year.

You correctly said the economy would grow 3% to 4%; for the first three quarters of this year, it has grown at 2%, 2.1% and 5.2%. But you said that if the Fed did not ease, we would face a recession. You expected the Fed funds rate to be between 2% and 3%, but it is 5.25 to 5.5%, and the Fed seems to have engineered the immaculate soft landing. What is your outlook for economic growth, a recession and for the likely path of Fed policy?

As right as I was on the stock market, I was wrong on interest rates. In fact, it looks more like 2024 will play out the way I thought 2023 would play out.

I pivoted around July to believing high rates would not be as devastating to the economy as I had believed. I voiced this in my appearances on CNBC and other media. I had looked at the data and revised my estimate higher of what the neutral level of interest rates would end up. I saw the economy could withstand higher interest rates.

One of the reasons why rates will be higher is the fact that bonds are not as good a diversifier to risk assets in an inflationary environment. Because of the double whammy we saw in 2022 [both the stock and bond market were down double digits], investors need higher interest rates to hold bonds. Another factor is that faster economic growth also raises interest rates.

I still think rates are going down in 2024. The Fed penciled in three rate cuts. We may have five or six rate cuts. I think that the Fed funds rate should finally get to 3% to 3.5%, not at 5.25%, as it is now.

You forecast that the long bond would go below 3% this year. The yield on the 10-year Treasury at the start of the year was 3.5%. It was as low as 3.4% in March. It peaked at 4.9% in October and is now 4.1%. Where will the yield be on the 10-year over the coming year?

That low estimate was because I had been much more bearish on what yields were going to end up because I thought the economy would slow more. Then, as I had indicated, I revised my estimate of rates upward.

The 10-year will not go down to 1.5% to 2.5% in the new equilibrium because of faster economic growth and the fact that people are more suspicious of the hedging ability of bonds. The 10-year is going to settle between 3.5% and 4%.

We also spoke about TIPS last year. You said they would eventually move to their equilibrium rate, which is 0%. But real rates have actually increased across the TIPS yield curve and are now approximately 2.25%. Are TIPS cheap? If real rates come down, what does that mean for stocks?

TIPS rates will move down, but not as much as I thought last year, for the same reasons given above. Already, 10-year TIPS is in the 1.60% range. I expect TIPS to be 1% to maybe 1.5% in the new equilibrium. If you have 2.5% inflation, you get a 3.5% to 4% nominal interest rate on the 10-year bond.

There was certainly a lot of money that could have been made for TIPS investors over the last two-month period.

You said last year that housing prices would decline about 10%. The Case Shiller index did decline modestly in December, but it is up about 7% since we spoke. The explanation I have heard is that the spike in home mortgage rates has deterred sellers and reduced supply. What is going on with housing prices, and what do you expect in 2024?

I have spoken to Professor Shiller, the originator of the Case-Shiller index. We are seeing quite a few cash transactions at the high end of the market that might be distorting the index upward. There are fewer transactions at the lower end of the market, which is not holding up as well as the top end.

In that case, the Case-Shiller index is overstating what has happened to housing prices. We initially had a huge surge, a 45% increase in housing prices from the pandemic in March 2020 to March 2022. Then the index began going down, but recently has come back up. I think an index of lower-priced houses would not show the bounce back.

That said, if rates are going down then I don't look for a significant decline in housing prices. There won't be a boom like after 2020, but we could have a rise of 5% to 10% in housing prices in 2024.

Last year, you correctly predicted the outperformance of dividend-paying stocks, and you said that was part of a multi-year trend that would favor value over growth. But over the past 12 months, growth has been the winner. For example, the Vanguard Value ETF (VTV) returned 0.60%, but the Vanguard Growth ETF (VUG) returned 28.95%. Do you still favor value stocks? Are there other sectors that are exceptionally over- or under-valued?

Last year, 2023, was a year for growth stocks. That was very unusual, because normally when you have a bear market, the leadership for the next bull market is different. This is one of the very few times when the leadership of this new bull market is very similar to the leadership before of the last bull market that ended in January 2022. Usually leadership shifts.

But it is a much sounder bull market than the one is 2021. The speculation that took place in the pandemic darlings, in the crypto and NFT markets, and in the SPACs is gone. The quality-growth stocks reasserted themselves this year – Google, Nvidia, Tesla, Microsoft, Amazon, Alphabet, and Meta.

But we still have a big gap between the valuation of value and growth stocks. We also had that gap at the beginning of last year. That's one reason I thought value would come back in 2023. But it might happen in 2023. If we're not going to have a recession, which is looking more likely, that's when value stocks will do well.

Since the Fed meeting [on December 13], I'm beginning to see money flowing towards value. Not that tech will do badly – they're great companies. But the valuation difference between growth and value is large. Small- and mid-cap stocks are selling at 12- to 13-times earnings. The Magnificent Seven are at multiples of 25 to 30 and more. You don't need much growth when you're at 12- or 13-times earnings to get great returns; but you need a lot of growth if you are 25- to 30-times earnings.

I did some analysis. I combined the 2022 and 2023 returns. It's very interesting – 2022 was terrible for growth, but great for value; 2023 was bad for value, but great for growth. Over the two years, growth and value had almost exactly the same return and both were flat. The S&P was also flat over the two years. What was not flat were small stocks. They are down around 10% to 15% from where they were two years ago.

Last year, you favored international stocks. The Vanguard non-US ETF (VXUS) returned 7.9% over the last 12 months, versus 14.4% for the S&P 500. Do you still favor non-US equities? Are there any geographies that look particularly attractive?

It's very interesting because, if you look at Europe and Japan, their return in dollars was almost the same as the S&P this year.

Emerging markets did not do as well. There's something very important to remember when you invest in international stocks. You're basically investing in value stocks. Growth stocks are in the U.S. There are very few growth stocks outside the U.S. You're in a value situation in Europe and Japan, and their value stocks far outperformed value stocks in the United States. Actually, it was a very good year for EAFE (Europe Asia and Far East) index investors.

Emerging markets did have problems because of the strength of the dollar and higher interest rates.

The dollar is going down if the Fed eases. That should be good for international stocks going forward. P/E ratios in Europe are 11 to 12 and in Japan at 13 to 14. These are very reasonable value P/Es. You don't need much growth to get a good return from a P/E ratio like that.

I believe 2024 will be strong for international stocks because of its value orientation.

We’re heading into a presidential election year. When we speak a year from now, we’ll know the results. Given the likelihood of a Biden-Trump rematch, what are your expectations and, more importantly, do you foresee and changes to tax policies or other measures that would affect investors? Is either a Trump or a Biden victory better for the markets?

In 2016, when everyone feared Trump, the S&P futures on election evening, when the polls indicated he would win, went down. Then, suddenly investors said, "Just a minute. Republicans are pro-market. They're pro-economy, pro-tax cuts." Within a matter of hours, the S&P started moving up rapidly. It was a great stock market year. Republicans have always been more capital friendly for the market.

I don't like tariffs. I didn't like Trump's tariffs. So far, Trump has not mentioned tariffs as much as he did eight years ago. So, I'm not as fearful. In fact, Biden actually kept a lot of the Trump tariffs and didn't reverse them. The tariff issue may not be different between the Republicans and Democrats.

What is very important for everyone to concentrate on is that most of the Trump tax cuts are going to expire in 2025, no matter who wins the White House. This means that, unless the Republicans take the presidency, the Senate, and the House of Representatives, which is a tall order, those tax cuts will not be extended as they are now.

Obviously, if all three of the branches are captured by the Republicans, then all the tax cuts could be extended. But if one branch of the government (either the House, Senate, or presidency) goes to the Democrats, there are going to be many changes in taxes at the end of 2025.

On the presidency, it is important to remember that between Biden and Trump, we do not have a socialist running for presidency – someone really far left and very anti-capitalism. Both Biden and Trump want the stock market to go up (about 60% of Americans now own stocks).

So, who wins the presidency may not be that important. The Fed is much more important.

When we spoke about risks last year, our discussion focused on China’s COVID policy and whether it might import deflation to the rest of the world. Those seem like small risks now, compared to what is going on in Israel, which is fighting a war on five fronts. The war in Ukraine is ongoing, and there even appears to be a new strain of COVID that may have originated in China. What keeps you up at night?

This year, I've changed what I think is a primary risk. We must protect our internet and our digital communication systems from hacking, especially from interference from abroad.

Recall the hacking that took place at some of the big casino companies a few months ago that stopped operations. Can you imagine the chaos if people woke up in the morning and tried to get their bank account, or their brokerage accounts, and they couldn't access them?

The security of our data is extremely paramount. Resources must be made available to make that data secure. I'm also speaking about government data. Security on the internet is a risk that we must devote resources towards going forward.

I don't see big risks from current wars. We already have oil below the level that prevailed before Russia invaded the Ukraine. There's a lot of oil and we are energy independent. A rise in the price of oil doesn't have the impact on our economy that it had in the 1970s.

Investors can get a risk-free return of 5% or more in Treasury bills out to one year. What would you say to investors who are perfectly happy with that return, versus taking on risk in equities?

This is a good question. Investors ask, "Prof. Siegel, you're talking about a 5% return on stocks? I can get that in Treasury securities."

My prediction is that stocks are going to have between a 5% and 6% return after inflation over the next three to five years. That's a little bit lower than their long-term historical average, but much higher than a 5% nominal return from the Treasury market. If we have 3% inflation, a 5% nominal return is only a 2% real return.

If you want a real return on a Treasury bond, you must go to the TIPS market. The 10-year TIPS is 1.65%. That's all you're going to get after inflation and this bond does not have good tax qualities. You should only own them in your retirement account.

If we're talking about returns, stocks are claims on real assets. My long-term research is definitive: Over time, stocks completely overcome and compensate owners for inflation. They are perfect long-term inflation hedges.

Year-to-year, stocks are not a perfect hedge by any means. But long-term, there's no question that stocks compensate investors for inflation. The 10-year bond is now under 4%, but what is inflation going to be over the next 10 years?

You don't have to worry about that question for stocks.

By the way, I don’t want to put down TIPS too much. I'd much rather own the TIPS than nominal bonds. I just think stocks are going to do so much better. Clearly, some people want that guaranteed, 1.7% real return.

For a long-term investor, someone in the accumulation phase who is saving over a 20- or 30-year time horizon, what is the overall asset allocation that you recommend?

I don't think stocks are overvalued today. TIPS, currently at 1.7%, are less than half the yield of where they were when they were first introduced in 1997. I recommend a 75% stocks/25% bonds portfolio, with bonds mixed between Treasury securities and high-grade corporates.

By the way, for years the only bonds I've held long-term are junk bonds. Their returns are almost like stocks over the long term – about 1% or 2% below the S&P 500.

Jamie Dimon testified before Congress last week that the government should shut down crypto. Do you agree? Does crypto belong in a retirement portfolio?

No, we should not shut it down. Not that I'm a great fan of crypto, but there's no reason to shut it down. We should make sure that crypto has the same money laundering rules that banks must report. Crypto exchanges need to help stop ransomware and money laundering. But we shouldn't shut crypto down.

One of the disappointments of crypto has been that its price has been very correlated with the stock market. In fact, its correlation with the NASDAQ up through last year was approximately 85% to 90%. You're not getting diversification. This was one of the arguments in favor of crypto, and it is not panning out.

I don't hold any crypto, but I don't criticize those who do. Crypto is a response to a lazy banking sector. We should be able to transfer funds for 5 or 10 basis points on a 24/7 basis. Crypto is basically saying, "Hey, banks, wake up. Internationally and domestically, you can do better."

I want to make our money transfer system on the banking side much more efficient than we have today. Right now, it makes no sense to me. Merchants are charged 3% and then I get 2% back on my card. That's a wasteful transfer. We should be able to do better than that.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All