Big central banks are going to keep shrinking their balance sheets next year, pulling money out of the financial system, even if the fight against inflation looks to be won and interest rate cuts begin. Their aim is to restore the role of markets in supplying and setting the price of money.

It’ll be a bumpy ride. The Federal Reserve and others will be testing a great uncertainty: Just how much in central bank funds do banks need to feel comfortable? The last time the Fed got near this threshold in September 2019, short-term interest rates in money markets went haywire, spiking higher and leaving some hedge funds scrambling for cash.

Wonkish as this sounds, it’s far from a niche interest. Rising rates and declining reserves – the special money used only by banks, central banks and the government – have already helped spark a regional bank crisis and the collapse of Silicon Valley Bank.

US banks are competing fiercely for deposits, a key source of reserves, which some see as troubling. For Mark Cabana, rates strategist at Bank of America Securities, it suggests the Fed will have to stop shrinking its books sooner than it intends. However, the Fed and Bank of England have created new ways to support money markets, giving them greater confidence in testing where the threshold for reserves lies. This could turn into a monetary game of chicken in the next few months.

To grasp the mechanics at work, here’s a quick recap on reserves: This special money is created mostly by government spending, or central banks buying assets like Treasuries or lending against them. Before the 2008 financial crisis, banks in the US, UK and elsewhere mainly got reserves by borrowing them from private sources, like each other. Central banks would just top up any small deficits that appeared in the system. Since then, however, quantitative easing and the flood of cash to get economies through the COVID-19 pandemic left banking systems with a vast excess.

Policymakers aren’t trying to get back to the old system of scarce reserves, but they do want to get the point where reserves are simply ample rather than excessive. But what is ample? The Fed thinks it’s linked to the size of the economy: It will start to slow its balance sheet cuts when reserves equate to 10% of nominal gross domestic product and stop when they get to 9%, according to its last annual report on Open Market Operations.1

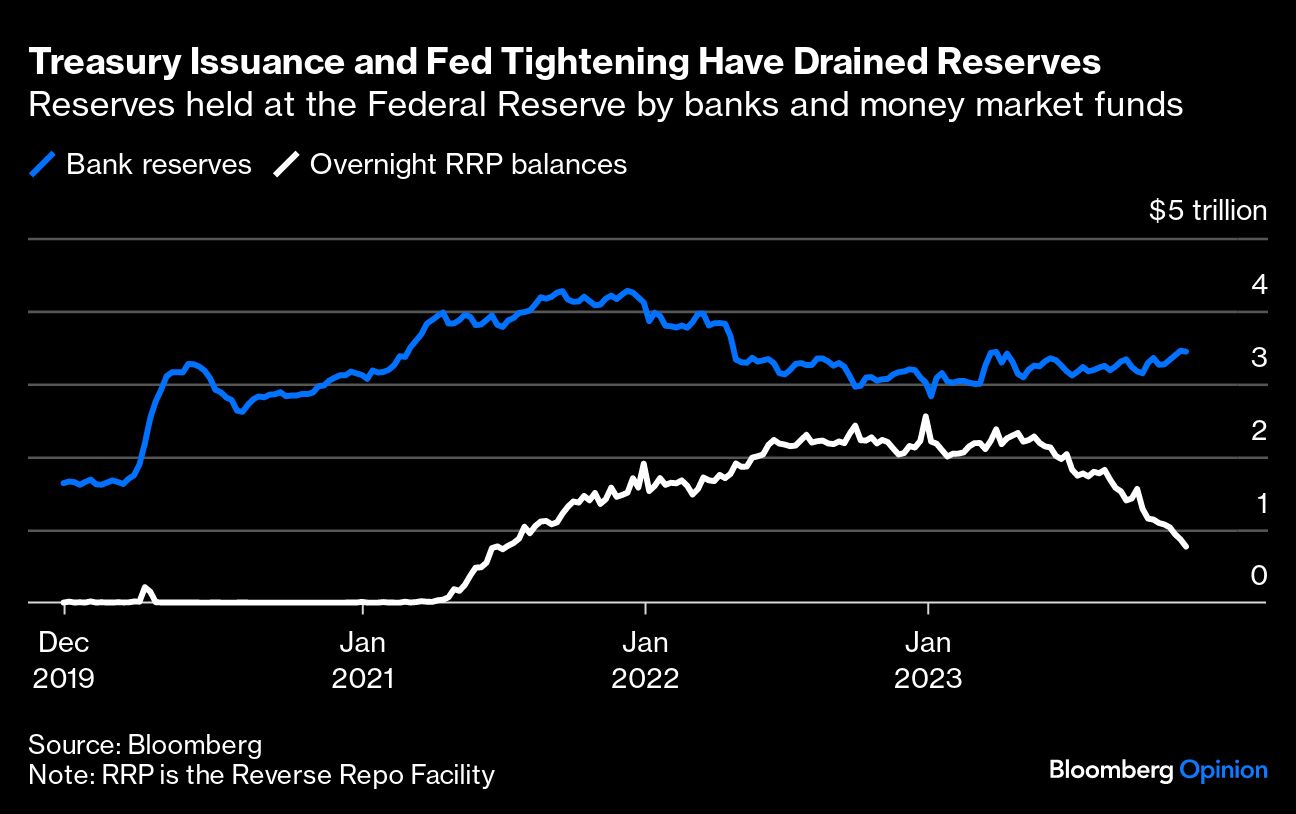

Right now, reserves held by US banks are down to about $3.4 trillion, having peaked at $4.28 trillion in December 2021. The Fed’s rule of thumb suggests the threshold for ample reserves is about $2.6 trillion, based on current nominal GDP and forecasts for 2024 growth. That’s well below where life got tough for regional US banks early this year when reserves were $3 trillion. Bank of America’s Cabana reckons the level where things get troublesome for money markets is only somewhat below that.

Banks have managed to keep reserves high this year even as the Fed shrank its books and the Treasury launched a borrowing binge after the debt ceiling fight was settled. Both these things suck money out of the system, but rather than banks losing out, the reserves came instead from money markets funds. These had been lending trillions of dollars back to the Fed through its Reverse Repo Facility. The funds have cut the cash invested here to just $770 billion now from $2.4 trillion at the end of March, switching a lot of money into new Treasury bills instead.

The rubber will really hit the road when money market funds decide they have pulled as much from that facility as they wish. Analysts disagree on exactly where that minimum level is, but even if it’s zero, we’ll get there in less than four months at the current pace.

So there’s a chance that sometime in the second quarter of 2024 the Fed’s squeeze on reserves will create the kind of disruptions seen in late 2019. Back then, overnight secured borrowing rates jumped as high as 9% for the most needy borrowers at a time when Fed interest rates were just 2%.

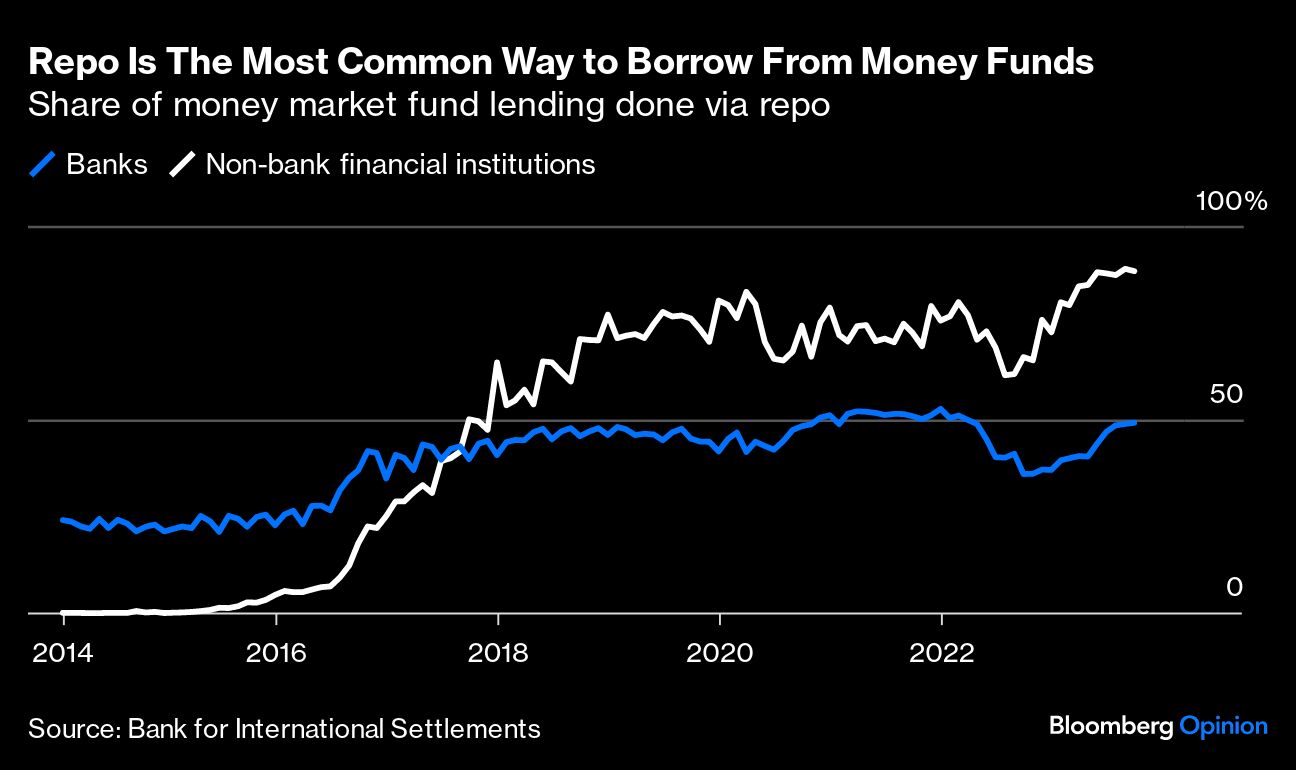

This is where the Fed’s new defenses come in. Money markets have changed a lot in the past five or six years in terms of how money flows between banks, money market funds and investors that want to bet with borrowed cash, such as hedge funds. In the old days, banks used to lend to each other and borrow from money market funds without any collateral as a guarantee. Now, most of money moves as secured lending via repos — this is short for repurchase agreements, in which a borrower sells a bond to a lender and agrees to buy it back later.

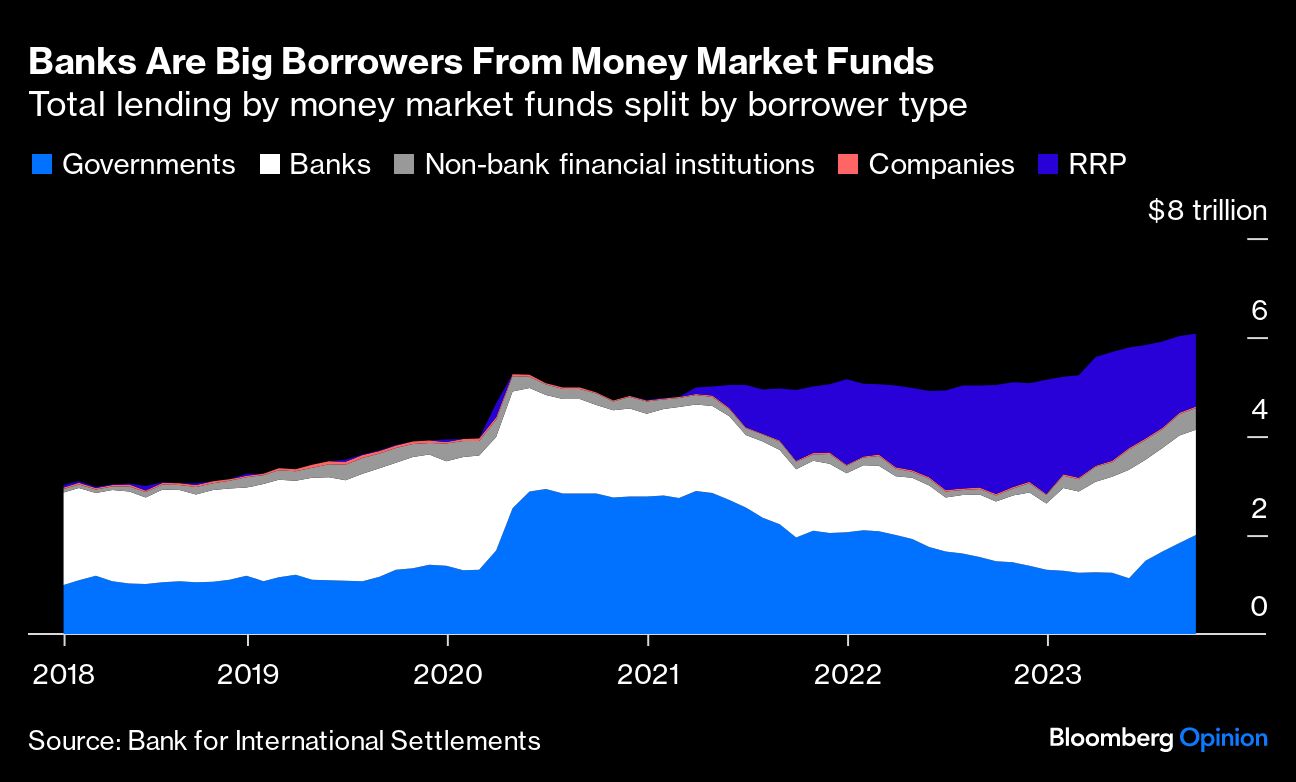

This changing character was becoming the case in 2019 and is even more true today, as shown in new research from the Bank for International Settlements, published on Monday. Money market funds lend a bit to hedge funds, almost exclusively through repo, and they lend even more to banks, who in turn use repo to lend to hedge funds and other asset managers.

In 2019, some of the biggest US banks stopped, or severely restricted, repo lending as they got worried about their own levels of reserves. The banks were fine, but many leverage-hungry clients were hurt by the spike in borrowing rates. Now the Fed has a new way to put money into repo markets that didn’t exist before: Its Standing Repo Facility should allow banks to lay off the borrowing demands of clients to the Fed if they don’t want to lend themselves.

The good thing about this facility is that it shouldn’t carry the same sort of stigma that banks worry about if they borrow money from the Fed for their own needs: That can lead their customers to think the bank is in trouble, thereby creating a bigger problem. The Bank of England created a similar facility last year, for the same purpose.

These programs are meant to give central banks a signal when they reach the low point of how much reserves the banking system needs. However, because they are new, banks might not be fully ready to use them, which make them less effective than hoped. Still, they are giving the central banks confidence to push on and find that point.

The rest of us aren’t going to have to wait that long now to find out just how bumpy the ride to the lower limit for bank reserves is going to be.

1See page 36 here: https://www.newyorkfed.org/medialibrary/media/markets/omo/omo2022-pdf.pdf

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies