Even as stocks rallied back during the monetary panic last week, big disruptions in the world of Treasuries threaten fresh pain for a host of hedging strategies on Wall Street.

Benchmark bonds capped their worst weekly selloff of the year Friday, with yields touching the highest in 15 years. For portfolios that rely on the world’s largest bond market to mitigate volatility elsewhere, the selloff has proved particularly troublesome. A Bloomberg gauge of the popular 60/40 model has slumped roughly 6% since the July peak, while the largest risk-parity exchange-traded fund is down 12%.

The synchronized selloff eased Monday as the Middle East conflict sparked a haven bid for Treasury futures while equities dropped. Yet in-tandem moves between both asset classes in recent months are reigniting a debate over the hedging power of Treasuries in an era where stocks and bonds are both prone to selloffs amid concerns of further Federal Reserve tightening.

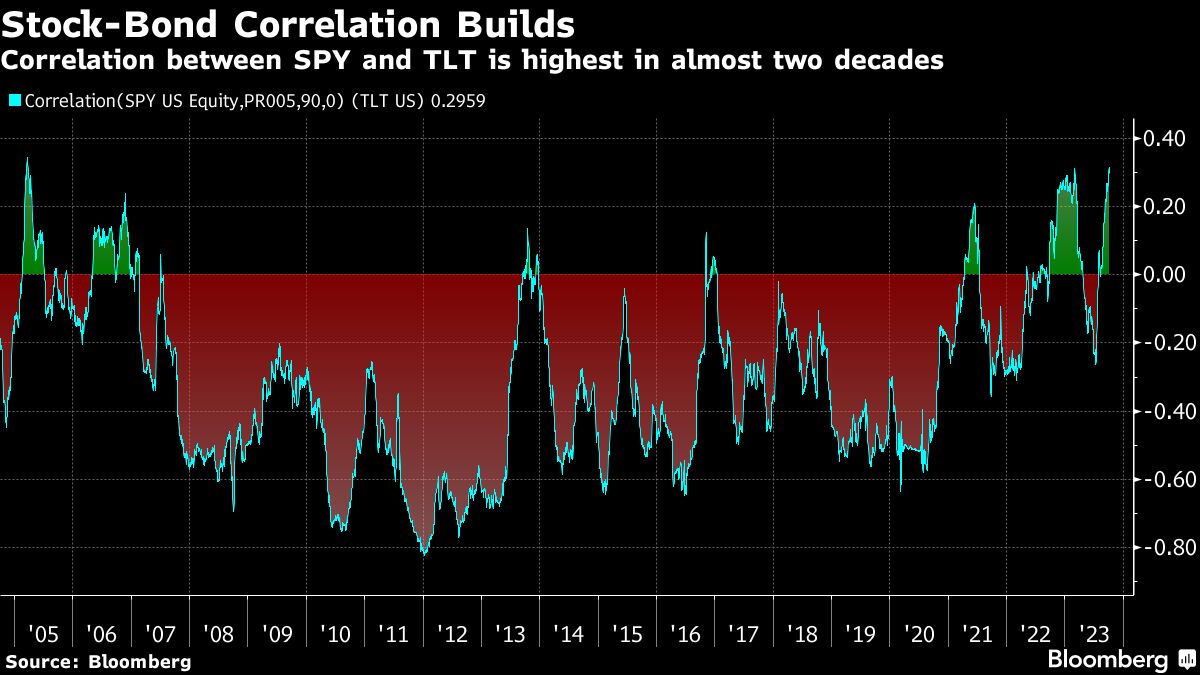

The 90-day correlation between the $37 billion iShares 20+ Year Treasury Bond ETF (ticker TLT) and $398 billion SPDR S&P 500 ETF Trust (ticker SPY) reached the highest since 2005 last week, according to data compiled by Bloomberg.

“For investors in the 60/40 portfolio, the ongoing volatility in a high rates environment is stomach-churning,” Apollo Global Management chief economist Torsten Slok wrote in a recent note. “With an outlook of high rates and slowing earnings — which is needed to get inflation under control — the outlook for the 60/40 portfolio remains negative.”

Textbook portfolio math says that combining fixed income assets with equities is supposed to dampen overall volatility while providing reliable payouts streams. However, the high correlation is subverting that relationship. Assuming that the stock-bond correlation moves from negative 0.35 to positive 0.50, that expected volatility of the standard 60/40 mix rises from about 8.5% to 11.5%, according to Bloomberg Intelligence.

“The relationship between US stocks and bonds, which has been largely negative for several decades, has rapidly turned positive,” Bloomberg Intelligence analysts Christopher Cain and Gina Martin Adams wrote in a report. “If it sticks, this shift in their correlation hints we could be entering a new era that would have massive implications by increasing the risk of the standard 60% stock and 40% bond portfolio.”

Benchmark 10-year Treasury yields have skyrocketed in recent months, reaching 4.89% last week — the highest since 2007. The climbing cost of capital has helped knock almost $3 trillion from US equity values since July.

“It has pretty profound portfolio-construction implications,” said Scott Ladner, chief investment officer at Horizon Investments. “It’s not that you need the bonds to do well when the stocks are doing well. The diversification trick is, ‘I’ve got to have the bonds do well when stocks go down the toilet.’”

The 60/40 strategy is on track for a third straight month of losses after dropping nearly 4% in September, according to data compiled by Bloomberg. Risk parity funds, which divide a portfolio across asset classes based on the perceived risk of each, have also buckled in recent weeks, with the $860 million RPAR Risk Parity ETF (ticker RPAR) languishing near its lowest level in over a year.

To be sure, stocks have still eked out double-digit gains this year. At the same time higher yields mean that while the current prices of bonds are falling, investors should collect larger interest payments over time, boosting returns over the longer term.

Still, that’s unlikely to stop them from searching further afield for ways to more effectively hedge now, including turning to lesser-known alternatives such as option overlay strategies, asset-backed structures, private assets and infrastructure.

“Usually, the stock market falls due to growth fears, which causes bonds to rally,” said Jay Hatfield, chief executive and founder of Infrastructure Capital Management. “In this market, we have overly tight global monetary policy, which means that any signs of strong growth are negative for policy which is bad for both stocks and bonds.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Katie Greifeld, Emily Graffeo