Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

As the Federal Reserve continues to tighten and banks accelerate their pullback from middle-market lending, private credit’s stability, strong downside protection and floating rate yields make it an attractive fixed income alternative.

The past 12 months have been challenging for individual investors who followed a tried-and-true strategy: Invest in equities for long-term capital appreciation and bonds for stability and income. As the Federal Reserve began aggressively raising certain benchmark interest rates to combat high inflation, the stock market tumbled. That much was anticipated, but investors did not expect their “stable” bond portfolios to follow their equities downward.

This selloff in bonds was not driven by worries of underlying credit quality but by the reaction of fixed-rate assets to rising interest rates, also known as “simple interest-rate risk.” Even institutional fixed income investors got this cycle wrong – they understood the risks posed by rising interest rates but generally underestimated the timing and magnitude of the shifts. Many regulated banks also underestimated the effect rising interest rates could have on their reserves and “flighty” deposits, driving the recent banking crisis and continuing to reduce many banks’ ability to lend.

Private credit as a solution

As they navigate this turmoil, investors are exploring options to mitigate the interest rate risk of fixed income products while simultaneously addressing higher inflation and interest rates. The continued growth of the floating-rate private-credit market presents investors with a unique option to meet this goal.

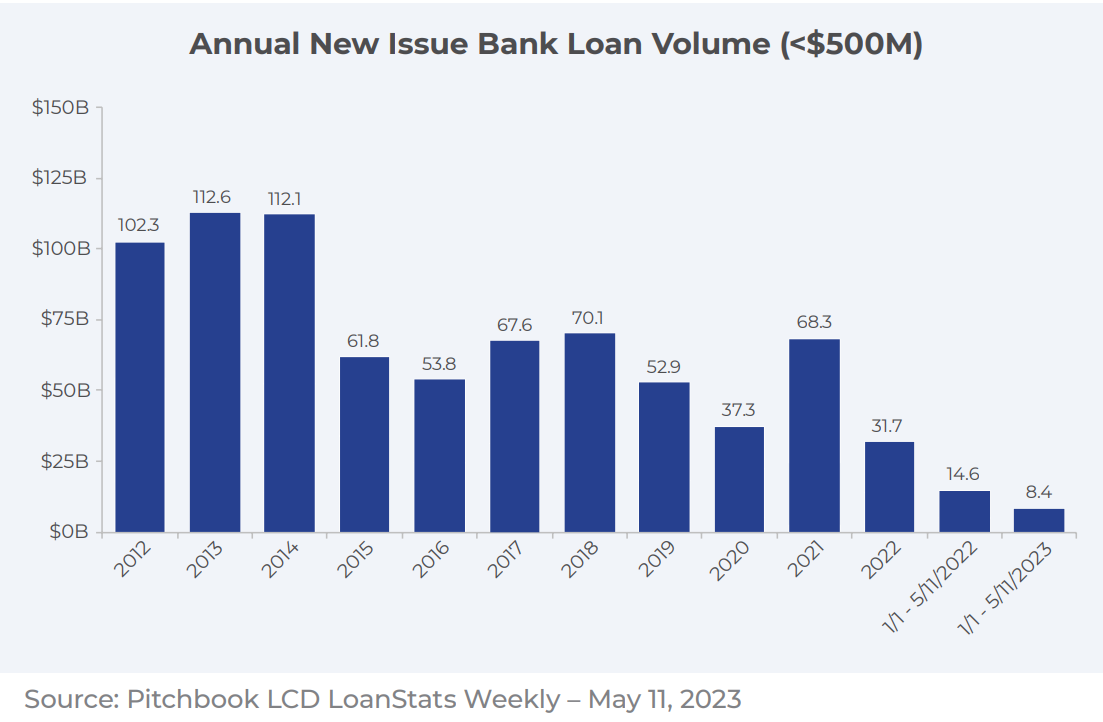

While private credit has its roots in the 1990s, this asset class grew dramatically in the wake of the 2008 financial crisis. New regulations in response to the crisis limited lending by U.S. banks to middle-market businesses, and the private credit asset class filled the void. The asset class had an estimated $1.4 trillion of assets under management as of year-end 2022, up from nearly $500 billion in 2014 (Source: Preqin). As the chart below illustrates, middle market companies’ reliance on private credit is only expected to grow as the current banking crisis accelerates regulated banks’ retreat from middle market lending.

Private credit has a long history of stable returns and low loss rates, which continues to draw investor capital into the asset class. The Cliffwater Direct Lending Index (CDLI), which tracks approximately 12,000 directly originated middle-market loans, has an annualized return of 9.31% since 2004. In the current high interest rate environment, the yield of the CDLI, assuming loans are refinanced or paid off after three years, has risen to 11.01% as of December 31, 2022.

A key component of generating these stable returns is low realized loss rates as demonstrated by the CDLI’s loss rate of 1.03%, compared to 2.3% for U.S. Bank Commercial & Industrial Business Loans (CDLI) and Federal Reserve (Fred: CORBLACBS). The Cliffwater Direct Lending Index – Senior (CDLI-S), which tracks loans made by managers focused on first lien senior secured loans, has a realized credit loss rate of 0.13% since its inception in September 2010. Private credit loans have migrated up the capital structure as direct lenders increasingly focus on senior secured loans to fill the void left as banks exited the senior secured loans market. Senior secured loans represent 78% of the overall CDLI as of December 31, 2022, up significantly from 38% at year-end 2009.

Key considerations

Compared to fixed-rate debt instruments, private credit generates high current cash flow and serves as an effective inflation hedge. Senior-secured-direct loans are predominantly 100% cash pay and floating rate, allowing their return to adjust to interest rates and inflation levels. In the current interest rate environment, with base rates driven by the Fed’s ongoing battle with inflation, this means cash pay yields in excess of 11%.

To increase exposure to private credit, there are multiple options including publicly traded business development companies (BDCs), unlisted private BDCs, and traditional commingled institutional funds with a defined investment period and harvest period. These private credit investment vehicles are generally structured to match asset/liability duration. This helps eliminate the issues at the core of the recent banking crisis – short-term liabilities (“flighty” deposits) and longer-term assets (illiquid loans).

Floating rate private credit can help investors navigate high interest rates and inflation while generating generous cash pay yields underpinned by a long history of stable returns. Equity returns continue to be uncertain and volatile while fixed-rate instruments will leave investors open to material interest rate risk. Given that the Fed continues to be hawkish on inflation, floating rate private credit can provide a good alternative.

Mr. D’Angelo is a founding partner of Stellus Capital Management and co-head of the private credit strategy and serves on its investment committee. He has over 25 years of investing, finance, and restructuring experience.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Read more articles by Dean D’Angelo

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.