Big US banks will have to clear significantly higher capital hurdles under long-awaited proposals announced by regulators Thursday. The good news for investors is that most of them are already there — and the few that aren’t should easily meet the tougher demands well before they need to.

The biggest lenders contend that higher capital requirements will increase costs for customers and could threaten some kinds of lending or trading activities. This might be partly true, but at the same time stiffer standards should make the banking system more stable, and they could bolster depositors’ faith in smaller banks by forcing them to manage risks as prudently as their bigger rivals.

Capital requirements for JPMorgan Chase & Co., Bank of America Corp., and the US’s six other global systemically important banks — plus Northern Trust, the only very large bank not part of the top eight — will rise by an average of 19%, according to the proposal.

Regulators estimated that five of these nine banks would fail to meet the new requirements based on their books at the end of 2021. However, even the largest shortfall was far smaller than the average annual profit of the biggest banks over the past seven years, the proposal said. This is what makes regulators confident that all shortfalls can easily be made up within two years even as the banks continue to pay dividends.

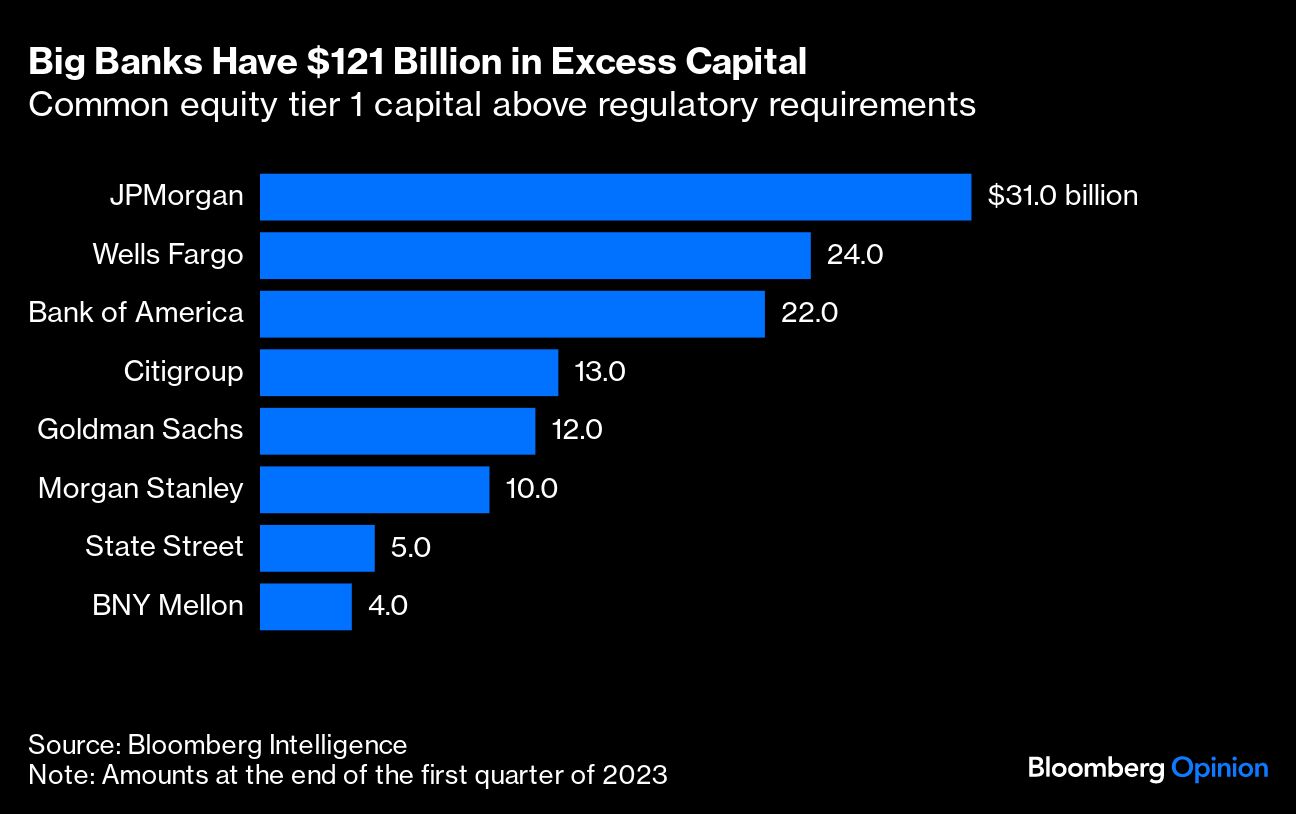

Still, the effect will be significant for all these banks. The higher demands will likely eat up most of the $121 billion of excess capital that the top eight US banks are sitting on, according to Bloomberg Intelligence. That is a lot of money, but it was almost all accumulated since June last year during a time when banks were still paying dividends and repurchasing stock.

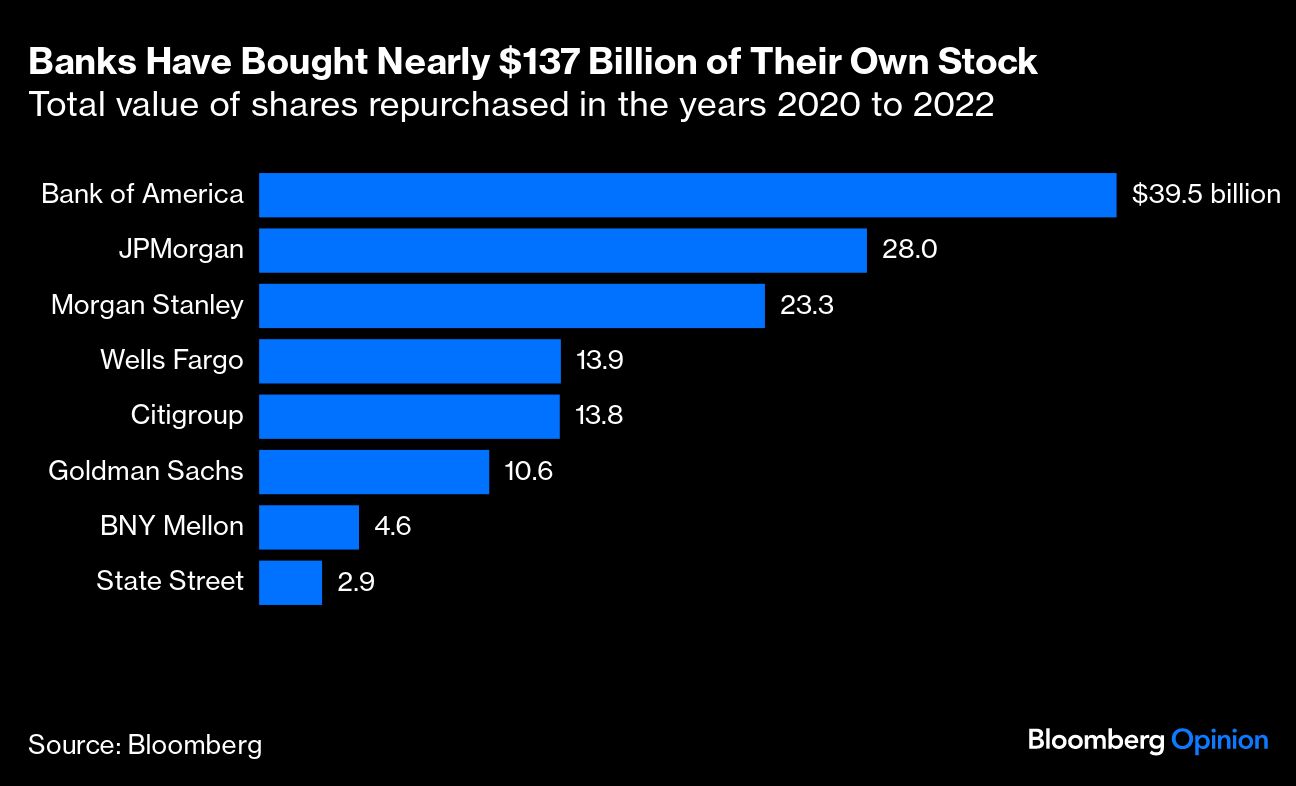

Just to underscore how much money the biggest banks make: Total share buybacks done by the top eight from 2020 to 2022 — which includes the Covid-19 pandemic — amounted to nearly $137 billion, according to Bloomberg data.

The proposals also won’t be finalized for a full year, and the banks will then have three years from the start of 2025 to reach the required levels. In other words, no bank is going to struggle to meet these requirements unless profitability collapses.

There is also a chance that the final demands could turn out to be lower than regulators’ projections. One of the main changes in the proposals is that operational risks will be included in the calculation of risk-weighted assets, which is the balance-sheet measure used to set capital requirements. Bankers are worried that this means they could get charged for the same risks twice: Operational risks, which include losses from cyberattacks, fraud, or rogue traders, are already included in the stressed capital buffers, which are calculated from the Federal Reserve’s annual stress tests.

But there’s a good reason to think that this shouldn’t be a problem. Stress tests look at how much money banks could lose in a crisis beyond what they already have capital for. The more that operational risks are reflected in minimum requirements, the smaller the extra crisis-type losses should be. In other words, the big banks’ stressed capital buffers could end up being smaller as their minimum requirements rise.

Among midsize lenders with total assets of less than $700 billion but more than $250 billion, such as PNC Financial and US Bancorp, capital requirements will increase by 10% on average. And for those with $100 billion to $250 billion, such as KeyCorp, Citizens Financial and American Express, the increase will average about 5%. All of the midsize and smaller banks already have enough capital to meet these demands, regulators said.

For smaller banks, the costs of adapting to stiffer capital rules aren’t only in the capital requirements but also in the extra work they’ll need to do for regulatory reporting and performing annual stress tests. There ought to be a payoff for this though: The more they are seen as being as strong as larger lenders, and the more they are forced to manage similar risks in a similar way, the safer they ought to appear to depositors.

Of course, they could still make bad lending or investing decisions or end up with a deposit base that is too concentrated among a similar group of clients — there could be a repeat of Silicon Valley Bank. But still, the more prudently smaller banks are regulated, the cheaper and more stable their funding ought to be.

There’s a long way to go until these rules are finalized and even longer before they’re fully in place, but the industry looks as if it can take these changes in its stride.

A message from Advisor Perspectives and VettaFi: VettaFi’s Fixed Income Symposium was the biggest virtual event of the summer. Register here for the replay link to learn from the experts and thought leaders who participated in the event.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies