Investment-banking deals have a reputation as bloody affairs of rainmakers and traders fighting it out in a kind of full-contact version of musical chairs.

But UBS Group AG looks like it can avoid the worst of this in its takeover of Credit Suisse Group AG. Many of the people that UBS doesn’t want have already walked away, and those it does want to keep will help it fill gaps in its capabilities.

UBS agreed in March to pay just under $3.5 billion in stock to rescue its local rival in a deal that closed this month. Hundreds of Credit Suisse bankers have bailed on their employer, especially since Swiss authorities stepped in to prevent it from collapsing chaotically when it suffered a run on deposits this year.

Sergio Ermotti, UBS’s recently returned chief executive officer, is happiest to get his hands on Credit Suisse’s wealth-management business. If it can keep most of its rival’s clients then the increase in assets under management for UBS will be equivalent to more than seven years’ worth of organic growth.

The investment bank and trading businesses are a different matter, however. Credit Suisse did a lot of riskier, capital-hungry fixed-income trading that UBS had abandoned since the 2008 financial crisis. It also used its balance sheet to win advisory work on mergers and acquisitions in a way that UBS had also long ago stopped doing.

UBS had already launched an effort to hire bankers and become a bigger player in US dealmaking, where it saw itself as sub-scale compared with its wealth business. It wants to double the revenue it generates from advising on M&A in the US. Before the Credit Suisse takeover, UBS planned to hire Marco Valla from Barclays Plc to become co-head of global banking, along with Barclays’s team of technology, media, and telecoms bankers. UBS confirmed those hires recently.

Even though many Credit Suisse bankers have left, UBS has managed to keep the key healthcare, consumer, and industrials specialists that it was targeting, according to insiders who weren’t authorized to speak publicly about the integration.

Many of the US-based Credit Suisse bankers who left are in areas where UBS has its own capabilities. These include equity and debt capital markets staff, who help companies raise funding, and leveraged-finance bankers, who underwrite and trade junk-rated loans and bonds, often to fund private equity deals.

UBS does want to win more business with private equity firms and has the appetite to expand its leveraged-finance business more aggressively when that market reopens. This could have been an area where Credit Suisse and UBS bankers battled for roles and where the different cultures clashed. UBS’s business is much smaller and more focused, while Credit Suisse’s US bank was heavily skewed towards this activity.

During recent months, however, Credit Suisse’s business crumbled even faster than the slowdown in the broader market. In the past three years, US and European leveraged finance accounted for up to almost 20% of Credit Suisse’s advisory and capital markets revenue, according to data from Bloomberg league tables and company reports. In the first quarter of 2023, its contribution dropped to less than 10%.

Many of the Credit Suisse people in this business have also left since the rescue deal: Spain’s Banco Santander hired several of that team and other Credit Suisse dealmakers for its own push into US banking. This all makes it easier for UBS to wash its hands of that unit, although it will have unwanted loans to sell or manage down over time.

It also wanted to keep a lot of the bankers in Asia that came with the deal because Credit Suisse was historically strong in Southeast Asia, while UBS is a bigger player in China and Australia. However, Jefferies Financial Group has swooped in to pick up about 20 mainly junior staff from Credit Suisse’s teams as it pursues an Asian expansion, Bloomberg News reported on Friday.

UBS will still have to cut thousands of other Credit Suisse jobs, particularly in supporting roles in many countries as well as in many parts of the markets businesses.

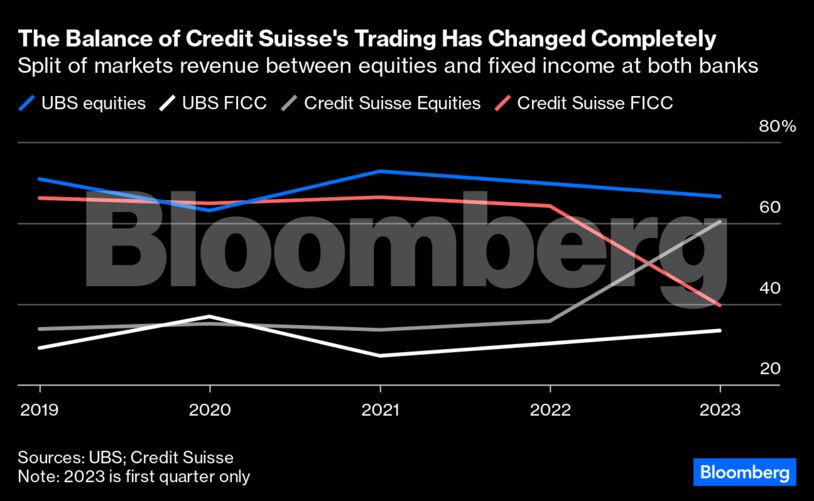

A lot of Credit Suisse’s bond and currency trading operations will be culled, although UBS wants to retain some capabilities in emerging market credit and complex derivatives linked to government bonds and interest rates. The collapse of leveraged-finance trading and Credit Suisse’s sale of its securitized products business to Apollo Global Management also seems to have reset the balance between fixed income and equities trading to better suit UBS without new management having to lift a finger.

On the equities side, UBS wants Credit Suisse’s electronic trading specialists including quants, technologists, and salespeople who can rebuild those platforms on UBS’s systems.

Across the investment bank, UBS’s approach is to take the people it wants and ditch all its former rival’s technology, systems, and corporate entities. This ought to help make the integration smoother, but means that it could take UBS longer to recapture Credit Suisse’s revenue.

UBS might say more about how much of its rival’s sales it expects to keep after the takeover when it reports half-year results at the end of August. But it won’t be until 2024 that the actual outcome of the deal will start to become clearer. Even then markets will need to pick up for UBS to get close to its longer-term run rate.

There will be plenty of challenges getting the remaining Credit Suisse bankers and traders to settle into the UBS way of doing things and bring their clients with them. But the kind of open warfare that typically flares up when two banks merge shouldn’t be nearly as bad in this takeover.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.