The conventional wisdom is that the pandemic induced a trend of de-globalization, as major economies decreased the reliance of their supply chains on other countries. But, according to Louis-Vincent Gave, globalization will thrive, and the focus will shift from China to India and other southern hemisphere countries.

The conventional wisdom is that the pandemic induced a trend of de-globalization, as major economies decreased the reliance of their supply chains on other countries. But, according to Louis-Vincent Gave, globalization will thrive, and the focus will shift from China to India and other southern hemisphere countries.

Gave is the founding partner and chief executive officer of Gavekal Research. He co-founded Gavekal in 1999 with his father Charles and Anatole Kaletsky. Gavekal started as an independent research firm; it evolved in 2005 to include fund management and in 2008 to include data-analysis services.

Gave was a keynote speaker at John Mauldin’s Strategic Investment conference on May 5.

Gave’s corollary to his outlook was that commodity prices will perform well in the coming year.

U.S. investors don’t have enough exposure to emerging markets and commodities, Gave said. But the performance of those asset classes will be accelerated by a weakening dollar, more corporate scandals (like FTX and Theranos), and instability in the U.S. banking sector.

Don’t give up on China, though. Gave said it will grow strongly in the second half of the year and will “bring along” Japan and Korea.

Let’s look at how Gave developed his views.

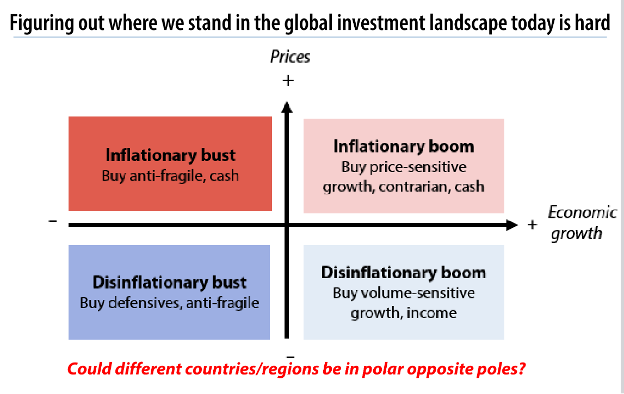

He began by noting that his investment discipline starts by asking where the U.S. and other major economies are in the familiar two-by-two matrix of inflation and growth:

Gave said, “Having done this for roughly 25 years, I don't think it's ever been as hard as it is today.”

He admitted that he could make a case for any of the four scenarios, but his outlook is clearly for an inflationary boom.

He said that David Rosenberg and Lacy Hunt persuasively argued for a deflationary bust. That is supported by metrics of the U.S. economy: The leading economic indicators (LEIs), the ISMs for manufacturing and services, an inverted yield curve and slow money supply growth all point towards a recession.

His uncertainty around the economic outlook is highlighted by the recent failures of several banks at the heart of the technology ecosystem, starting with Silicon Valley Bank. Yet the Nasdaq performed well, led by Meta, Microsoft and other technology giants.

The workforce in most developed countries, including the U.S., is shrinking, which is usually deflationary, because there will be fewer consumers of goods. But Gave disagreed. He cited the example of Japan, which suffered decades of deflation starting in the 1980s as its workforce shrank. But he said that was partly because of Japan’s real estate collapse and mostly because of the growth of the Chinese work force and economy, which brought an onslaught of cheap goods. His conclusion was that we should not assume that the shrinking workforce or slower productivity will be deflationary.

Nor should we expect the growing tensions between the U.S. and China to be deflationary. He cited a clever quip, which he attributed to the analyst Luke Gromen, “If truth is the first casualty of war, then bonds come in a close second.”

Bond prices, Gave said, did poorly after Russia’s invasion of Ukraine and will continue to do so as what he called a “cold war” between the U.S. and China escalates.

The supply of U.S. Treasury bonds will grow by $2.5 trillion annually for several years, Gave said, and this too will be inflationary.

All major central banks, including the U.S., Great Britain, China, and Japan are expanding their balance sheets, he said, and pursuing procyclical fiscal policies.

“Is this really an environment where I should be lying awake at night,” Gave asked, “worrying about a big deflationary bust?”

The debate between deflationary bust versus inflationary boom comes down to whether you look at levels or changes, Gave said. If you look at changes, then things are “dicey.” The falling ISMs, money supply and bank loans, among other metrics, are deflationary.

But looking at levels gives him optimism. Consumers make decisions based on levels, not changes. For example, although mortgages rates have gone up, so have wages, and the U.S. residential real estate market is still strong.

“For all these reasons, the US economy will avoid a recession,” Gave said.

China is a source of optimism for Gave. He expected China’s economy to surge once its COVID and other restrictions were lifted. But that did not happen, he said, because its “animal spirits” were dampened. In part, that was because the Chinese government did not pursue aggressive fiscal measures until after the lockdown ended, whereas the U.S. had those policies in place during the worst of the pandemic.

Now China is growing, Gave said, and bank loans, money supply and construction are expanding. During COVID, China expanded its manufacturing sector, and is now the second largest global exporter of automobiles.

“In my career, when I've seen China stimulate, when I've seen China press on the buttons,” he said, “then global growth re-accelerated.” That was the case in 2003, 2009, and 2015-2016, he said.

That optimism does not translate to the dollar, according to Gave. There has been a paradigm shift that no longer favors the dollar. The dollar was strong for the last two years, he said, as the Fed hiked and the interest-rate advantage drove capital to the U.S.

Now there is a “de-dollarization,” he said, with too many dollars “floating around” the global economy. This can be seen through our current account deficit, which grew from $100 billion to $275 billion per quarter over the last year. Much of that money flowed to Chinese entrepreneurs, he said, creating a “dam of liquidity” during its COVID lockdown.

Now that dam is breaking, and he expects the dollar to trend lower.

The other big trend that Gave highlighted was the growth of India and other southern hemisphere economies. He cited new Apple factories in India, a rail line that China just built in Pakistan, and trade agreements between Saudi Arabia and Iran.

The byproduct will be a need for infrastructure and commodities.

“In a world in which we're thinking there's not going to be any growth in the U.S or in China,” he said, “the infrastructure spending growth that you're going to see in that ‘yellow crescent,’ for lack of a better word, is going to be absolutely gargantuan over the next 10 years.”

“I have been, and I remain in the inflationary camp,” Gave said. “I think that big parts of the world are entering an inflationary boom of epic proportions. I think it's the case of pretty much all emerging markets.”

Robert Huebscher is the founder of Advisor Perspectives and a vice chairman of VettaFi.

Read more articles by Robert Huebscher

The conventional wisdom is that the pandemic induced a trend of de-globalization, as major economies decreased the reliance of their supply chains on other countries. But, according to Louis-Vincent Gave, globalization will thrive, and the focus will shift from China to India and other southern hemisphere countries.

The conventional wisdom is that the pandemic induced a trend of de-globalization, as major economies decreased the reliance of their supply chains on other countries. But, according to Louis-Vincent Gave, globalization will thrive, and the focus will shift from China to India and other southern hemisphere countries.