High-yield investors beware. Junk bonds that were financed at low, fixed rates will eventually mature and, according to Jeffrey Gundlach, weak issuers that cannot refinance at higher rates will default.

Gundlach spoke to investors via a webcast, which he titled “Survivor,” and the focus was on his flagship total-return fund (DBLTX). Slides from that webcast are available here. Gundlach is the founder and chairman of Los Angeles-based DoubleLine Capital.

High-yield defaults were delayed as bonds were financed at low, fixed rates, he said. During the Q&A portion of the webcast, Gundlach was asked how defaults will look at higher rates, once those bonds mature.

“The cycle has been delayed,” he said, “but if the economy is struggling with high rates and weak GDP growth, we will have the highest default rates of all time.”

Gundlach chose the title of his webcast because very few investors have survived the high rates and inflation of the 1970s. Indeed, he said, many have not survived the ultra-low rates prior to 2022.

That lack of experience among investors with a rising-rate environment fuels the danger in high-yield debt.

“We will see significant defaults in CCC loans,” Gundlach said. Those are floating-rate bonds, and interest rates on them have been ratcheting up as the Fed has raised rates.

Lending standards are going up, and defaults are just starting to rise. Portfolios should be upgraded in credit quality, he warned, and DoubleLine has done so over the last 18 months.

“Get out of high yield,” he said, “because spreads have not risen in response to equity market declines.”

Deficit doomsaying

Gundlach reiterated his prior warnings about the rising federal deficit.

“We are getting to a moment of awareness on the deficit,” he said. The Social Security trustees have warned its system will run out of money in the next nine years, and that forecast does not include a recession. The problem with Social Security must be addressed by 2028, according to Gundlach.

He noted that federal unfunded liabilities are 10 times GDP and that deficits have gone from 4% to 6% of GDP since the 1970s.

The debt ceiling debate will end with the sides “yelling at each other” and then the problem will be “papered over,” he said.

“This is a big problem,” he said. “It is no longer your grandchildren’s problem. It is our problem.”

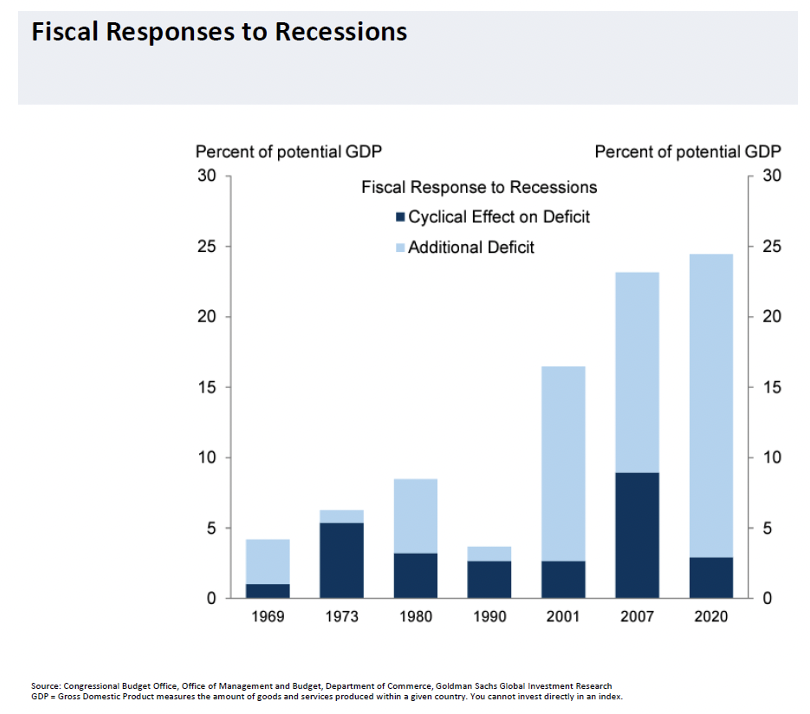

The fiscal responses to recessions have worsened the problems with the deficit. In the 1990s, there was no fiscal cost to the response to the recession; but in this century, he said the costs have been profound, as shown in the graphic below:

Federal interest payments were below $1 trillion until the pandemic, he said, and then they “exploded.” If the Fed raises rates by 50 basis points, as he expects, those payments will go “straight vertical,” Gundlach said.

The two-year Treasury yield is up 91 basis points since the last Fed meeting, and the yield curve has become more inverted. The two-10-year spread is 105 basis points, which is the most in decades, and the yield curve continues to invert. That inversion trend has been in place for 15 months, Gundlach said.

With the two-year Treasury yield at 5.01%, it corroborates the idea that the Fed will take its funds rate to 5%, he said, unless the unemployment rate surprises to the downside. Unemployment data will be released on Friday.

But the increased level of yield curve inversion does signal an imminent recession. He said a recession doesn’t happen until the curve de-inverts (i.e., becomes less steeply inverted).

The copper-gold ratio, which Gundlach closely follows, says the 10-year Treasury yield is about 100 basis points too high. It looks like 4.25%, which occurred in late October 2022, will be the high on the 10-year, he said.

Gundlach noted several unique aspects of the economic and market data: the Fed funds rate is now higher than the core PCE rate, which is 4.71%.; the 60/40 is now earning less than the one-year Treasury yield, which is above 5%; and the commercial paper yield is higher than the S&P earnings yield.

Recession indicators

Gundlach acknowledged that the recession indicators haven’t changed much in the last three months, since his prior webcast.

The leading indications (LEIs) are very recessionary, he said, and “the momentum continues to be gathering.” Based on LEIs levels prior to previous recessions, he said tongue-in-cheek that “we are two months into a recession, but just don’t know it.”

The ISM manufacturing prices suggest that inflation will come down to 3% by mid-year. But looking at the PMI, he said, a recession will start now. The lags of monetary policy will start weakening the manufacturing sector soon, given that tightening began last May.

“We are getting close on a lot of these indicators,” Gundlach said.

Consumer expectations are showing a “harbinger” of a recession, he said. They indicate that a recession is coming but not here yet. The same is true of consumer revolving credit. Credit card usage has risen significantly over the last two years. Consumers are not borrowing because they want to, Gundlach said. “It is not bullish for the economy. It is because food, energy, rent and car prices have risen. Consumers are buying certain necessities with borrowed money.”

Unemployment (3.4%) is at a very low level, but its 12-month moving average is 3.7%. When the unemployment rate crosses that moving average it is a recession indicator. Based on economists surveyed by Bloomberg and data from the Fed, Gundlach said unemployment will increase by 120 basis points and those rates will intersect. This led him to conclude that the Fed is implicitly forecasting a recession – and not a mild one. He said 1.75 million jobs could be lost. More than half the states are losing jobs and 74% of the U.S. population lives in those states.

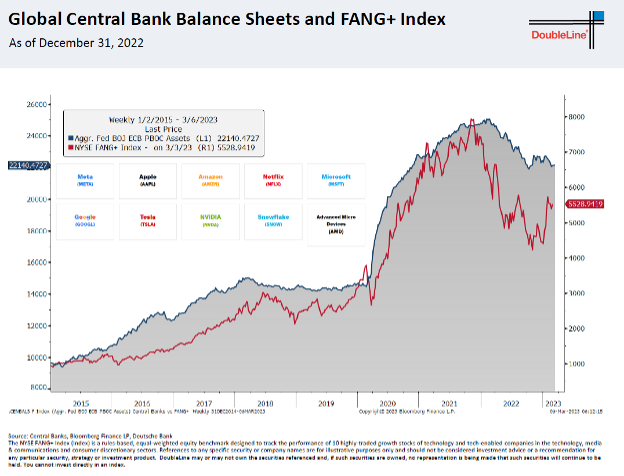

The FANG-plus index follows the Fed balance sheet, as shown in the graph below.

The Fed is committed to quantitative tightening (QT), he said, “so you should not own the FANGs.” When the Fed is increasing its balance sheet, it is encouraging risk and fueling momentum. “Investors will get killed again when the market reacts to rate hikes,” Gundlach said.

The VIX typically moves in sync with the probability of a recession, but not this time. The VIX, therefore, is likely to go up and will do so as the market loses value, according to Gundlach.

Real rates increased about a year ago, which was when the equity market fell. Real rates went down in October and went up starting in February. “Real interest rates are driving the [equity market] picture,” Gundlach said.

About two and a half years ago, he started recommending European stocks, and those stocks started outperforming U.S. stocks about 18 months ago. If the dollar resumes its downtrend, Gundlach said, which was in place last year, the rest of the world will outperform. That dollar downtrend was in place last year.

Europe has outperformed year-to-date, but not emerging markets (EM). The S&P 500 has outperformed EM since 2010, but EM will outperform when the dollar weakens.

Inflation

The CPI is 6.4% and excluding food and energy it is 5.6%. The PCE is 4.7%. Gundlach concluded that inflation is approximately 5% based on that data. He said that Fed Chair Jay Powell now looks at core PCE excluding housing, which is also 4.7%. But Gundlach doesn’t like that approach, and said that housing is a big part (28% of the CPI basket) of consumer expenses. (I wrote about this issue a year ago and argued that housing – other than rental costs – should not be part of the CPI basket.)

Gundlach likes to look at export and import prices as a measure of inflation, and he said that those have “crashed” over the last year. Those prices are increasing at less than 1%, which suggests that inflation will come down. But Gundlach said he is not sure if that will happen fast enough for the Fed.

Money supply growth, as measured by M2, is now negative year-over-year. It suggests inflation is coming down.

The Bloomberg commodity index is not important as an inflation indicator when the Fed raises rates, Gundlach said. “Commodities need to increase by 10% before they impact inflation.”

In the Eurozone, inflation was lagging the U.S., but its inflation is now 8.5%. Excluding food, alcohol and tobacco, inflation is 6.5% in Europe. The Eurozone needs to get more aggressive, Gundlach said, which will lead to a weaker dollar.

Housing prices are still higher than they were two years ago but have fallen over the last six months. Gundlach said there is not a default problem facing homeowners, because those homes are not “underwater,” have positive equity and can be sold if necessary.

Mortgage payments for first-time buyers doubled in the last 18 months. Housing is less affordable than in 2006 and at its worst level since 1997.

Mortgage-backed securities (MBS) prices are attractive because prices are down and don’t face the risk of calls/prepayments. Refinancing is your friend, Gundlach said, although it is unlikely. “This has not happened before.” Another way of saying this is that convexity is no longer negative; it is zero. MBS spreads are about 130 basis points above Treasury bond yields.

The Fed has stopped buying MBS and has let the ones it owns mature, Gundlach said. That has reduced supply and increased MBS yields.

Robert Huebscher is the founder of Advisor Perspectives and a vice chairman of VettaFi.

Read more articles by Robert Huebscher