The CFP Board is Confusing and Misleading Consumers

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The CFP Board has strayed from its mission of improving life for the consumer. Instead, it is generating as much confusion as possible for the furthering of its own interests. Make no mistake – transparency is not on its agenda. This is a massive disservice to the public.

Why the debate is important

My guests and I exposed the numerous pitfalls of the CFP Board in a recent podcast debate.

The debate participants were John “JR” Robinson, Scott Salaske, and Robert Wright. JR took a lead role in the debate; he has a 15-year history of exposing the CFP Board’s transgressions and has written numerous articles on this subject.

These podcasts are important to the profession because they open conversations that are central to the role of the financial planner: questions of ethics, governance, advocacy, transparency, and what it means to truly deliver the fiduciary standard.

We’ve debated these topics in depth in two podcasts. Please listen to the CFP Debate Part One and Part Two when you have a moment.

The CFP Board’s non-transparent and misleading regime

There are two major ways that the CFP Board has failed to serve consumers: an intentionally vague search tool and misleading advertisements. They have taken actions that allow predators to use the market to freely prey upon the unwitting.

1. Advisor search tool leads you into lion’s den

Go to the “Find a CFP® Professional” tool on the CFP Board website. Just click here.

Now, enter your zip code and get the names of the first 10 advisors who pop up. Then research them on the IAPD or FINRA BrokerCheck site.

What do you find?

Disclosures!

And what’s scary is that the retail consumer will never do this, leaving them open to being preyed upon by unscrupulous CFP® certificants that this tool points directly to. Sadly, the CFP Board only indicates if the advisor has been disciplined publicly by the CFP Board or has declared bankruptcy.

Bankruptcy?

Who cares?

Do you think that because somebody had five years of medical debt leading them to go bankrupt that they aren’t a suitable advisor? And showing if they’ve been disciplined by the CFP Board isn’t saying much either, given that in 2020 only 84 disciplinary actions were taken. Given there are 92,814 certificants, this is 0.1% (CFP Board, 2022).

The CFP Board should tag anyone with an IAPD or FINRA disclosure history on their search tool so that unsuspecting consumers aren’t led by a trail of breadcrumbs directly to the lion’s den.

The unscrupulous individuals should be removed altogether. Some disclosures are frivolous – for example, you got caught using your brother’s fake ID in college – but that is still an infraction of the law. If you have broken the law, the consumer should be told clearly and be given the option to decide about whether that matters to them.

Instead of bankruptcy, the way the advisor is compensated (fees, commissions, or both) should be freely disclosed on the search tool.

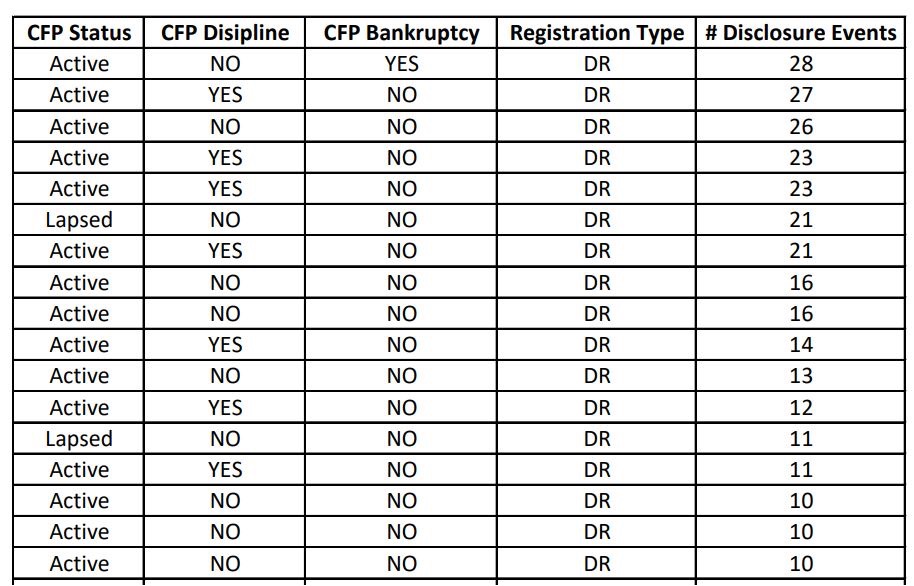

According to JR Robinson, there are some people in the directory “with disclosure histories that would make Bernie Madoff blush.” This table below, used with permission by JR, shows some CFP® certificants with more than 20 disclosures – too much to be bad luck. Yet the CFP Board does nothing to protect consumers.

Source: IAPD, Finra BrokerCheck, Advisor U4’s, JR Robinson

You had 28 disclosure events and still active? Gimme a break – you practically have to be a convicted felon to get your CFP taken away.

2. Misleading advertisements

Advisors

Advisers

Advicers

Agents

Fee-only fiduciary

Fiduciary standard

Suitability standard

Hybrid advisor

Are you confused yet?

And if that isn’t bad enough, the CFP Board is posting obfuscating ads, making matters worse! Take the following (awful) examples of CFP advertisements, past and present.

Implying the CFP is more trustworthy than the non-CFP professional

In frame 0:25 of this CFP advertisement video, it says, “If they’re not a CFP® pro, you just don’t know.” And if that is not a blatant endorsement, I don’t know what is! This is an old advertisement that is not in active circulation, but it does reflect a past transgression.

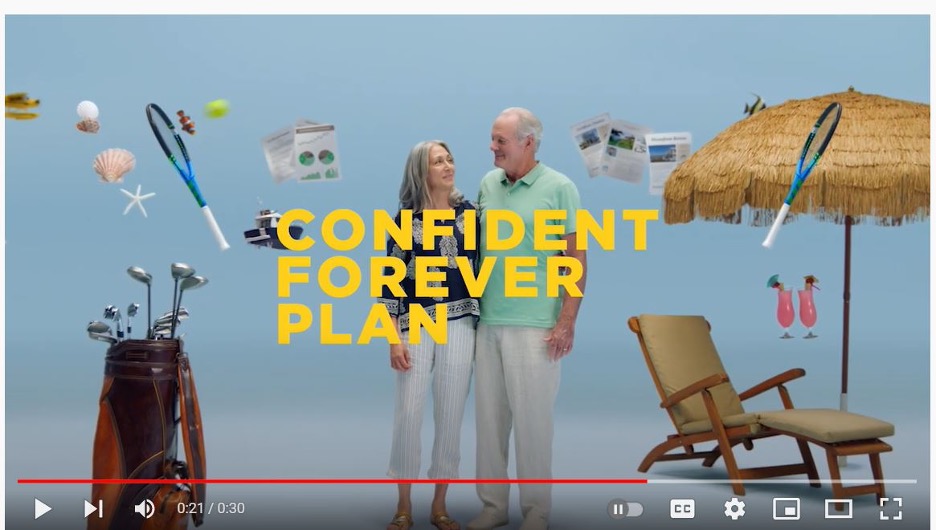

Misleading terminology

See frame 0:21 of this CFP advertisement video, “confident forever plan.”

You don’t think that’s a little misleading?

It implies that you create one plan and you’re done with financial planning. The phrase sounds so promissory – there’s a reason no compliance officer will ever let you so much as utter the word “forever.”

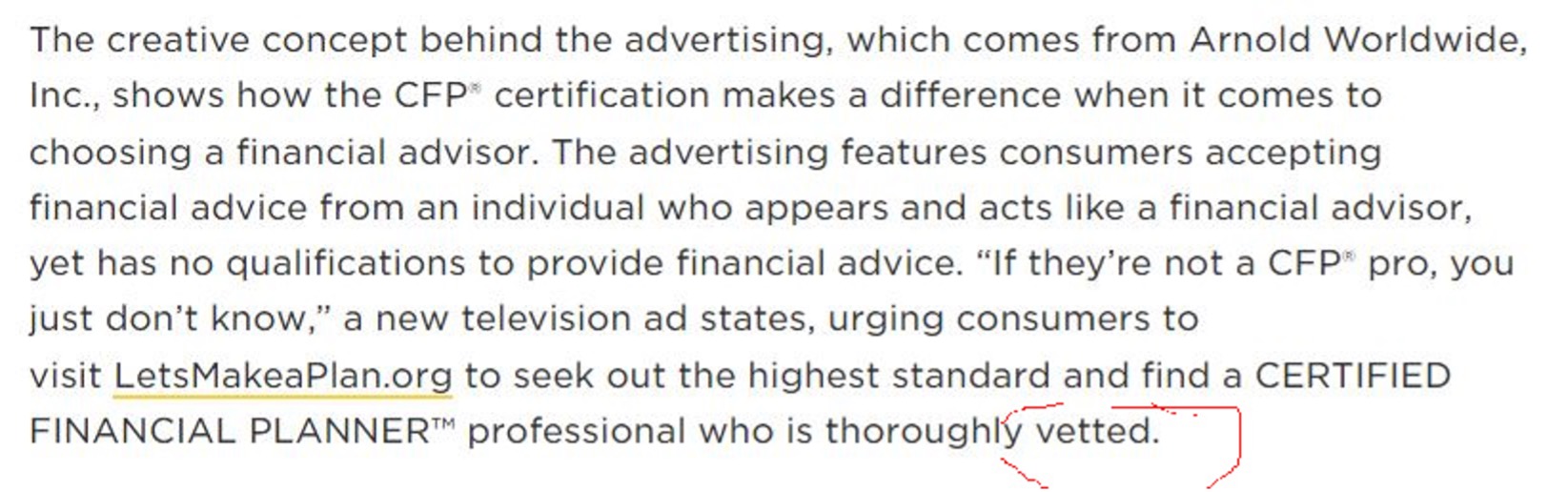

False assertion of vetting

From a 2014 press release:

Vetted? These people are vetted? As I just explained – they are clearly not!

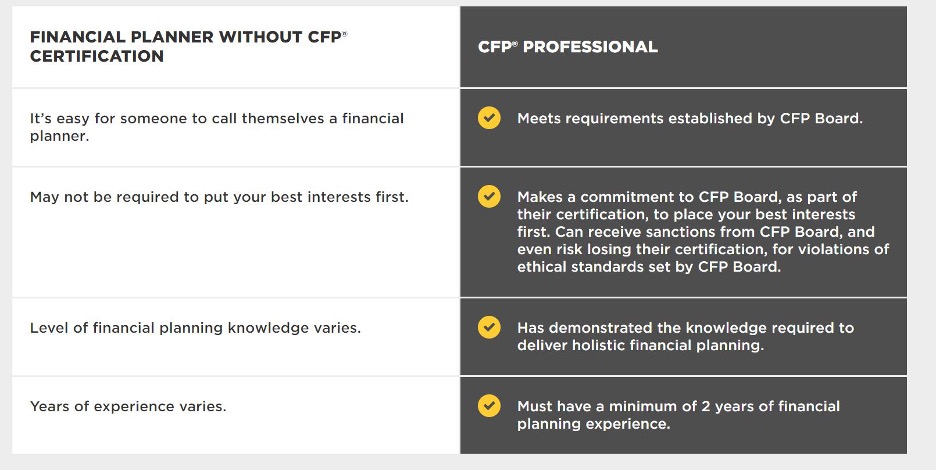

Unsubstantiated advantages over non-CFPs

From the CFP website:

Wow, just wow.

It’s laughable that they are touting the two-year experience requirement as reason that you should pick someone with this certification. The average amount of experience for a paraplanner is four years, and eight years for an associate advisor, according to a Kitces article.

As we’ll get to in a minute, not everyone who holds the designation acts in the best interests of the client, given that over 75% of certificants are not pure fee-only fiduciaries.

It’s serious to mislead consumers, and it becomes even more worrying when the financial planners who hold the designation start repeating these ideas, or even worse, use the designation’s merits to defraud. Some have used the credential to help them defraud consumers. About 20 years ago, there was a well-known financial planner and radio personality named Bradford Bleidt who ran a $30 million Ponzi scheme. He confessed to have used the CFP designation for credibility to help himself pull it off.

3. The code is a falsely marketed abridgement of the fiduciary standard

The CFP Board Code and Standards is the highest standard, according to the CFP Board.

Really!

The highest standard?

That would be the fiduciary standard.

Here are a few examples of what’s wrong with claiming that the CFP code and standard represents the “highest standard” (above the fiduciary standard, that is):

- There is no guarantee that a CFP® professional is following the fiduciary standard 100% of the time. Remember that 70% of CFP® certificants are licensed insurance agents, and 85% of them are paid by both fees and commissions.

- In 2009, the CFP Board proclaimed fiduciary status without providing their certificants with any training. It is only over the last few years that they have begun to do some training to provide their certificants with the background to be able to do so.

- According to Section A.5 of the CFP code, you’re required to disclose material conflicts of interest; not material facts as you would under the real fiduciary standard, allowing CFP certificants not to disclose what they earn in insurance commissions, for example.

- The CFP code doesn’t require disclosures to be made in writing whereas they are by the SEC law.

Consumers are utterly confused about who is a fiduciary and who isn’t, and obfuscations like this are one of the reasons why.

4. Represents interests of insurance companies, not the consumer

The CFP Board increased its fees by $100 this year! It would be palatable if the increase were for a good reason, but it has lost its mission. Its leadership should have just said, “Instead of raising your dues by $100, we’d like you to make a $100 donation to your local state insurance commissioner and we’ll call it even.”

Its mission is supposed to be benefitting the public, no?

Then what in the blazes happened to the emphasis on community outreach? Teachers are getting scammed in their ESP’s, widows and veterans are getting funneled into sham annuities, and the CFP Board is more concerned with playing nice-nice with the insurance companies.

And on top of that, the CEO Kevin Keller makes $1 million a year!

Have you lost your mind, bro? $1 million?

It’s not like he won the Nobel Peace Prize for his amazing contribution to society.

Sara’s upshot

The CFP Board has lost its mission, straying from educating and protecting the consumer and instead focusing on increasing membership and garnering political clout. It acts more like a political party than a professional certification organization.

But there’s a new force materializing in the industry, one with the power to eclipse all that have come before.

It is the dawn of transparency.

The Transparent Advisor Movement’s mission is to promote ideals of clarity, modesty, integrity, dignity, and client advocacy in all aspects of financial advice, with a special focus on advice-only, flat-fee, and hourly service models. There is an emphasis on clear disclosure of services and their related fees.

The goal of the Transparency Movement is to create the country’s best financial advisors – the most ethical, effective, and successful financial advisors that the industry has seen in its history. To do this, we are dismantling many of the norms and reconstructing them with a sheer focus on the experience of the end client, something that has never been done before.

The Transparency Movement is the future of the industry – we welcome anyone who believes in our values and wants to be a part of it. Please join us.

Our next meetup is October 12, and we welcome anyone who wants to make history alongside us as the first truly transparent movement in this industry. Sign up here.

Acknowledgements

I would like to humbly thank the following people for their invaluable contribution to this article.

- Knut Rostad – I’m grateful to Knut for proofreading this blog, for his defense of the Fiduciary Standard, and also for including the Transparent Advisor Movement in his work with the Institute for the Fiduciary Standard.

- JR Robinson – JR was the driving force behind this debate. I’m amazed at his perspicacity, initiative, and ability to remain committed to protecting the consumer in the face of resistance.

- Robert Wright – I give Robert a lot of credit for being the outspoken voice in this debate. Without him defending the CFP Board, it would not have been possible to debate and I’m so grateful for his grace, poise, and strength of character.

- Scott Salaske – Scott always brings a down-to-earth perspective to my podcasts. His experience as a successful flat fee advisor is an unbelievable source of strength for the Transparent Advisor Movement.

Sources

- Certified Financial Planner Board of Standards. (2019, February 6th). [Video]. Cal and Val. https://www.youtube.com/watch?v=jvsgkbwOLWk

- CFP Board. (2014, February 2nd). CFP Board To Consumers: Ask For Cfp® Certification, The “Highest Standard” For Financial Planning Advice. https://www.cfp.net/news/2014/02/cfp-board-to-consumers-ask-for-cfp-certification-the-highest-standard-for-financial-planning-a

- CFP Board. Why Choose A CfP® Professional. https://www.letsmakeaplan.org/how-to-choose-a-planner/why-choose-a-cfp-professional

- CFP Board. Code Of Ethics and Standards Of Conduct. Section 8.5. https://www.cfp.net/ethics/code-of-ethics-and-standards-of-conduct#

- CFP Board. Verify a CFP® Professional. Verify an individual’s CFP® certification and background. https://www.cfp.net/verify-a-cfp-professional

- FINRA BrokerCheck. https://brokercheck.finra.org/

- Kitces, Michael. (2017, October 16). 2017 Financial Advisor Compensation Trends And The Emerging Shortage Of Financial Planning Talent. https://www.kitces.com/blog/how-much-financial-advisors-make-salary-bonus-compensation-latest-industry-benchmarking-data/

- Mason, Bob. (2011, November 11th). Mason Law PC. Veterans Scam Alert: Happening At An Assisted Living Facility Near You!. https://www.masonlawpc.com/veterans-scam-alert-happening-at-an-assisted-living-facility-near-you/

- PR Newswire. (2014, February 3rd). CFP Board to Consumers: Ask for CFP® Certification, the "Highest Standard" for Financial Planning Advice. https://www.prnewswire.com/news-releases/cfp-board-to-consumers-ask-for-cfp-certification-the-highest-standard-for-financial-planning-advice-243349151.html

- RMH Advisors. (2016, November 22nd) [Video]. CFP Board Commercial Can You Tell the Difference 30 second TV Ad. https://www.youtube.com/watch?v=nXv6lkweUmc

- SEC IAPD. Investment Adviser Public Disclosure. https://adviserinfo.sec.gov/

- SEC Release 1092 on the Investment Advisers Act of 1940: Applicability of the Investment Advisers Act to Financial Planners and Other Persons Who Provide Financial Services, 45 Wash. & Lee L. Rev. 1139 (1988). Available at: https://scholarlycommons.law.wlu.edu/wlulr/vol45/iss3/10

- SEC. (2021, July 13). SEC Announces $97 Million Enforcement Action Against TIAA Subsidiary for Violations in Retirement Rollover Recommendations. https://www.sec.gov/news/press-release/2021-123

- Snider, Susannah. (2018 August 16th). US News. Who Can Be a Financial Advisor? https://money.usnews.com/money/personal-finance/family-finance/articles/2018-08-16/who-can-be-a-financial-advisor#

- U.S. Securities and Exchange Commission. (2013, March). Staff of the Investment Adviser Regulation Office. Division of Investment Management. Regulation of Investment Advisers by the U.S. Securities and Exchange Commission. https://www.sec.gov/about/offices/oia/oia_investman/rplaze-042012.pdf

- U.S. Securities and Exchange Commission. 17 CFR Parts 270, 275 and 279. [Release Nos. IA-2256, IC-26492; File No. S7-04-04] RIN 3235-AJ08. Investment Adviser Codes of Ethics. Final rule. https://www.sec.gov/rules/final/ia-2256.htm

- U.S. Securities and Exchange Commission. 17 CFR Part 276. Commission Interpretation Regarding Standard of Conduct for Investment Advisers. [Release No. IA-5248; File No. S7-07-18]

- U.S. Securities and Exchange Commission. [Rel No. I092] Applicability of the Investment Advisers Act to Financial Planners, Pension Consultants, and Other Persons Who Provide Investment Advisory Services as a Component of Other Financial Services. https://www.sec.gov/rules/interp/1987/ia-1092.pdf

- Weisman, Robert. (2009, January 20.) Boston.com. An earlier Ponzi pain lingers. http://archive.boston.com/business/articles/2009/01/20/an_earlier_ponzi_pain_lingers/

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All