The Price Advisors Will Pay for Ignoring Flat Fees

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

I’ll take an order of flat fees (otherwise known as retainers) with a side of financial planning. Customers are lining up out the door for this.

Shall we dig in?

Defining some terms

Even within the advisor community, there’s a huge lack of clarity as to what a flat-fee advisor is and is not.

A flat-fee advisor (in its purest, truest sense) is somebody who:

- Charges a fixed fee that does not vary over the length of the contract;

- Provides both financial planning and investment management services for that fee; and

- Is also referred to as a “fixed-fee advisor.”

A flat-fee advisor is not somebody who:

- Provides financial planning for a flat fee, and investment management services for an AUM fee;

- Provides financial planning for a flat fee, and receives commissions for selling insurance or brokerage products;

- Offers clients the option to be charged either a flat fee, a commission, or an AUM fee. No multiple fee options provided; there is only one option provided;

- Makes more money when the value of the assets in the client’s portfolio goes up;

- Works for a wirehouse;

- Is dual-registered;

- Is a hybrid advisor;

- Charges an AUM fee in addition to a flat fee;

- Charges commissions in addition to a flat fee;

- Earns commissions for selling insurance in addition to a flat fee; or

- Provides only financial planning services (this is called ‘advice-only’; not flat fee).

Some flat-fee advisors:

- Adjust their contracts for inflation; and

- Provide differing levels of service for different flat-fee amounts.

Flat fee versus AUM fee

A flat-fee advisor doesn’t necessarily make the same amount of money from the relationship than someone who charges a fee for AUM. In a down market or when a retired client is taking distributions, the flat-fee advisor may earn more.

The flat-fee model is more aligned with how we normally buy things as consumers. When we think about buying things, we think in dollars, not in percentage terms. A flat fee is the most straightforward way you an advisor can charge; there is clarity and zero ambiguity, allowing clients to feel more in control.

Prospect: What’s your fee?

Advisor: I charge 0.75% on AUM for planning and investment management.

Prospect: Wait, what’s 0.75% of $900,000? Is it $675 or $67,500?

(Invisible)

versus

Prospect: What’s your fee?

Advisor: I charge $10,000 a year for planning and investment management.

Prospect: Ah, I see. That’s $10,000. I usually save about $60,000 a year by using an advisor, so that means I’ll be saving $50,000. I’m okay paying for this.

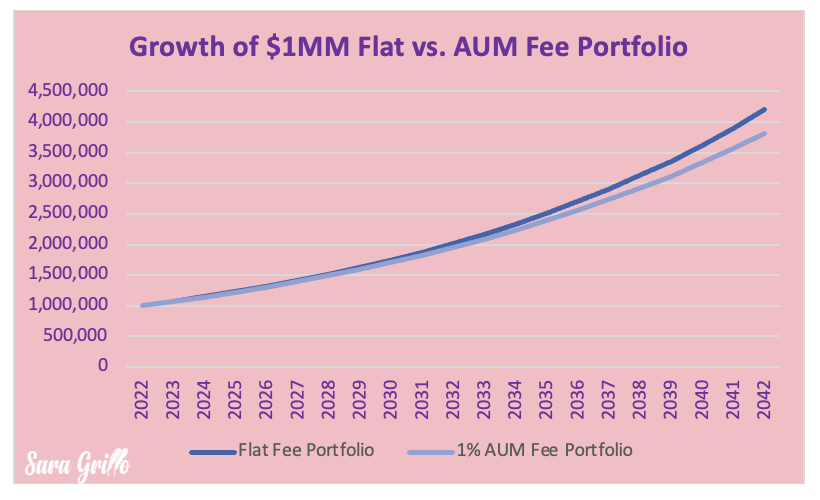

The graph below illustrates the difference between a hypothetical $1MM portfolio managed with a $10,000 per year flat fee versus a 1% AUM fee.

Assumptions: 1% fee on AUM, $10,000 annual flat fee, 8% annual nominal growth rate, fee debited at end of year, no withdrawals, contributions, or transaction costs. Projections are entirely hypothetical; future performance is not guaranteed.

You can see there is quite a delta. The flat-fee portfolio reaches $4.2 million while the 1% AUM portfolio only gets to $3.8 million.

It’s becoming a movement

I wrote about flat fees several years ago and at that point I didn’t see much potential. Frankly, I hadn’t seen anyone who impressed me by using them back then.

Since then, I’ve seen flat-fee advisors multiplying, and it’s not start-up advisors or one-person shops. There are established firms like Facet Wealth and Abundo Wealth who are serving clients in big numbers.

For the advisors who embrace it, it’s not about making more money. They do it because they believe that this is the most transparent and fairest way to work with clients.

I’ve heard amazing success stories and seen value propositions that you wouldn’t want to be competing with. I am calling it “the flat-fee movement.”

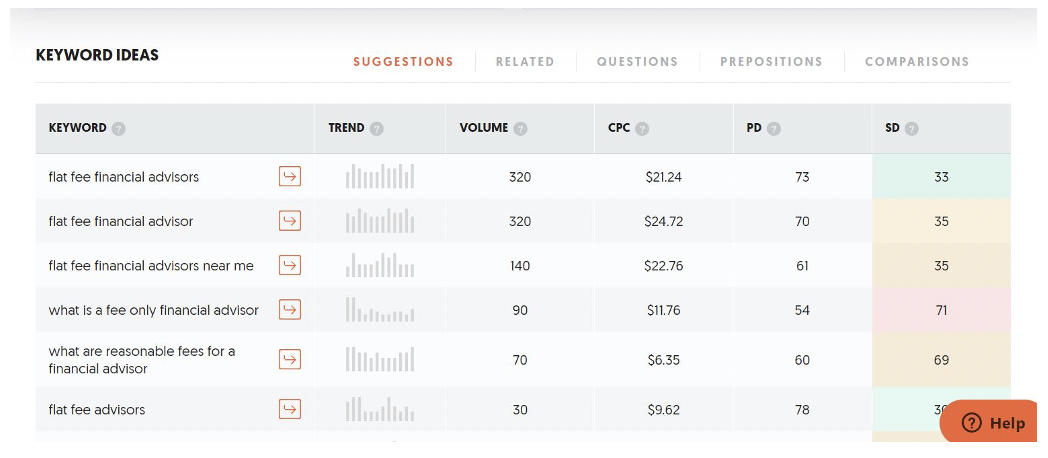

There is evidence of an uptrend for this information online. Look at this data from Ubersuggest displaying the monthly Google search volumes for this term.

It’s not nearly what the search volume is for fee-only advisors (well over 1,000 a month) – but still, these search volumes are nothing to overlook.

This is not about fees; it’s about value

Before we launch into a debate about which fee model is the best (which isn’t going to get us far), let’s pause for a moment and talk about the real issue:

The industry’s inability to articulate its value compellingly

Let me say it again, with absolute clarity:

There is a glaring hole where an advisor’s value proposition should be.

Advisors are tongue-tied when asked to justify their value. In the past, it has been based on:

- A product

- Investment performance

- AUM

The fact it’s AUM and not “assets under advisory” says a lot about who is in control of the narrative. Yet most advisors aren’t actively managing risk to protect the portfolio gains, even though that is what their clients pay for. But consumers have caught on, and value is going to be harder to justify.

To a rational person, it’s not worth it to pay 1% for an advisor to direct your money into a model portfolio of passive funds that may not achieve benchmark results (before fees). Or even worse, it’s invested in expensive mutual funds.

Financial planning is an eMoney printout given for free so an insurance agent or broker can justify a product sale.

Held-away assets (bitcoin, real estate, 401k) are often not given the attention they deserve because they aren’t included in AUM.

Tax planning is an afterthought or a “nice to have.”

Flat fees shift the value proposition to financial planning.

The flat-fee model offers a stronger value statement

Let’s look at year one for a married couple getting ready to retire with $1,200,000.

They sign up with an advisor charging 1% and pay $12,000 a year or more if the portfolio does well that year.

They have to pay $5,000 the first year for a financial plan and ongoing planning fees henceforth.

They have a gain in a mutual fund that the advisor sells to fit the portfolio into the model, so that he can make AUM fees on all the client’s money. This garners the client a $5,000 tax bill that year. The advisor’s fee isn’t affected because the client pays out of pocket to the IRS.

We’re looking at $22,000 (or more) out of the client’s pocket in year one.

Versus

They sign up with a flat-fee advisor who delivers an annual financial plan and manages the portfolio for $10,000.

The advisor implements a tax plan that manages the cost of the liquidated position, selling gradually. They still pay capital gains tax, but it is managed responsibly. The advisor makes the same fee whether or not the position is included in the portfolio.

It’s clear who the winner is.

Example of a strong flat-fee advisor value proposition

Andy Panko of Tenon Financial is an unbelievable example of a flat-fee advisor success story. He started a flat-fee practice and reached capacity in a little over two years.

He planned his practice while working at another job, and obtained licenses during that time, so he could be operational on day one.

He established flat-fee pricing and communicated it clearly on his website.

He specified an ideal client profile: those who need retirement and tax planning advice at a certain level of complexity.

He marketed his practice in a focused manner, establishing a Facebook group where he hosted non-sales discussions about tax planning, attracting qualified candidates.

He devoted full focus to his clients’ Medicare and retirement planning needs while investing their portfolio in low-cost ETFs.

He advises on held-away assets that he does not custody.

He kept overhead low by working out of a home office.

He planned his practice’s profitability responsibly.

He kept his client base uniform and turned away anyone who did not fit his ideal profile, limiting the amount of time and money spent randomly.

Mind blowing.

Listen to this podcast about flat-fee advisors for the full discussion.

It’s no panacea

Before I sound like an ode to flat fees in C sharp, let me pause. There is no perfect, universally applicable fee structure and the flat-fee model is no exception.

Some may argue that is not well-suited for clients who are smaller or who don’t demand much service.

A flat-fee that is not indexed to inflation and may compromise profit margins, and it may be hard to scale such a practice.

It may not work for clients whose complexity was not understood at the onset of the relationship, clients who truly need customized investment management services, or who seek active management of their assets.

The flat-fee model is for the professional advisor who:

- Can map out a plan for how they want to grow their practice, and follow it;

- Is undistracted;

- Runs their practice instead of letting it run them;

- Uses technology instead of piling on inefficient employees;

- Markets actively and in a focused way;

- Turns away clients who don’t fit the profile;

- Do math well enough to plan out their practice’s finances; and

- Control profit margins;

Like any feed model, not for everybody. And even if it were, a change in fees isn’t going to fix what is ailing the financial industry. There’s a much bigger change that is in order.

We need a “reputational reset”

Maybe flat-fee advisors are the next step in our evolution as a profession. O, maybe the market will tell us that. But changes in fee models alone are not enough.

It’s not fees that make it so hard and costly to get new clients; it’s the lousy, distrustful reputation the financial industry has. It’s not the fees that need to change – it’s the way we justify (or don’t justify) them.

Whatever form evolution takes, the only way reputation will improve is a focus on true, absolute value – delivering it, and articulating it clearly – instead of flexing on lower fees, fiduciary standards, higher AUM, licenses or whatever flavor of icing we using to decorate the cake.

We need a reputational reset as an industry – and here’s what needs to happen.

Evolve or advance?

To not just evolve into another form of what we have been, but to truly advance, is going to take higher objectivity, empathy, and mitigation of bias. It will mean that at every point of client engagement – from the marketing to the sale, onboarding and onwards – we need to routinely pull ourselves away for long enough to ask the hard questions.

These questions:

- Am I delivering what this client expects?

- Am I delivering what this client needs?

- If this were someone else’s client, would I be critical of how they’re being treated?

- Is the value of what I am giving much higher than what the client is paying – and do they perceive it to be that way?

Are my biases leading me to service this client sub-optimally?

Could somebody else provide more value to the client at the price I am charging?

We’re only as valuable as the honest answers to those questions, and if we continue to run away from them the future will be another version of the past. To advance, this shift must happen in all of us: the media, vendors, consultants, custodians, advisors of every kind, standard of care, and fee model.

And then we can call ourselves a profession.

Sara’s upshot

Here is where I share more of my thoughts.

I have established this resource sheet to support the flat and hourly fee advisor movement. Please avail yourself of it if you are a flat or hourly planner.

I’m a prolific blogger.

I have launched a series of talks regarding the evolution of financial services.

I have a podcast where I discuss financial advisor marketing and practice management topics; here is how to subscribe.

Sara Grillo, CFA, is a marketing consultant who helps investment management, financial planning, and RIA firms fight the tendency to scatter meaningless clichés on their prospects and bore them as a result. Prior to launching her own firm, she was a financial advisor.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All