U.S. Treasuries shook off the steepest jump to consumer-price inflation in four decades and absorbed a 10-year note sale, with the figures reinforcing already widespread anticipation that the Federal Reserve will start raising interest rates in March.

The December inflation figures were in line with the bond market’s expectations, and while benchmark Treasury yields initially rose moderately across the curve soon after the release, buyers soon emerged. The year-on-year jump in the consumer price index matched a forecast increase of 7%, while the core rate, which excluded food and energy prices, was a little hotter, expanding at a pace of 5.5%, versus an expected 5.4%.

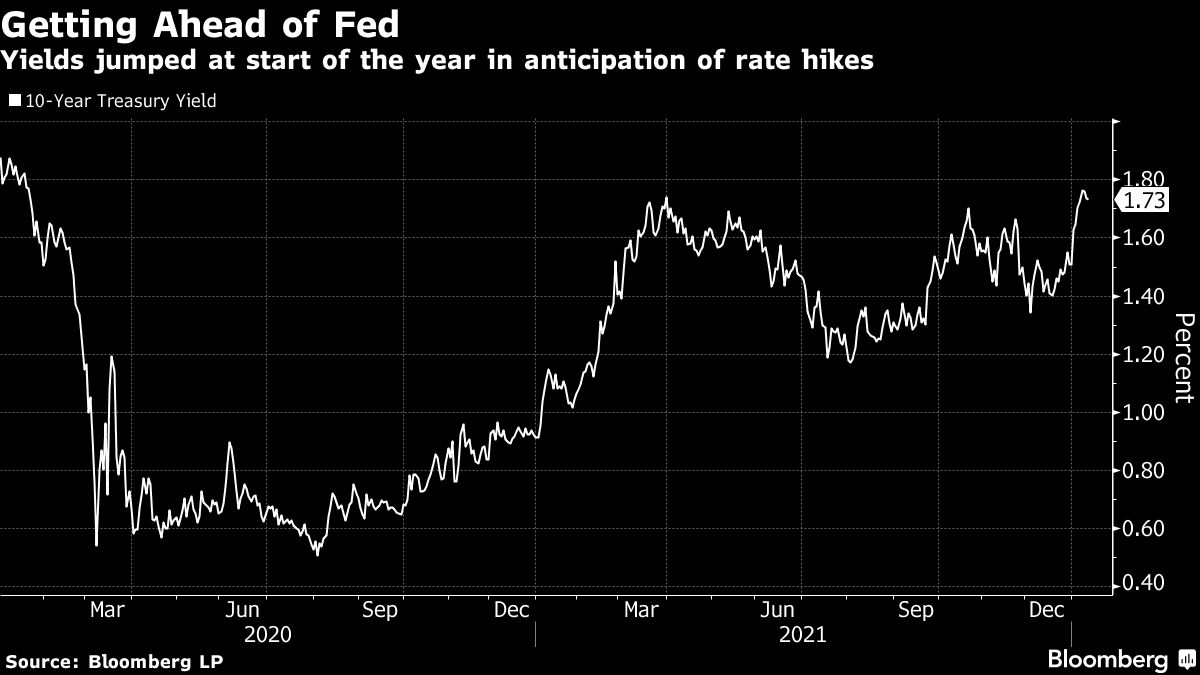

The reaction was muted in part because yields have already surged since the start of the year as traders brace for the Fed to begin hiking rates and wrapping up the bond purchases that have flooded markets with cash for nearly two years. Ahead of the inflation report, positioning in the broad Treasury market was the most net bearish since late 2017, according to the latest survey by JPMorgan Chase & Co.

“The market has aggressively repriced expectations for tighter Fed policy since the start of the year and it’s not a surprise to see some consolidation,” said Gregory Faranello, head of U.S. rates at AmeriVet Securities.

The policy sensitive two-year note yield was up 3 basis points at 0.91%, while the benchmark 10-year note yield was down 1 basis point at less than 1.73% following a brief jump above 1.75%. Interest-rate futures continued to reflect an 88% probability of a quarter-point rate hike in March.

The market absorbed the sale of $36 billion 10-year notes on Wednesday, with primary dealers left with a 16.6% share, a touch above the recent average, according to BMO Capital Markets. The reopening arrived at the highest yield since January 2020 and after a sharp rise in the benchmark’s yield from 1.51% at the end of last year.

As the U.S. economy endures a period of elevated inflation pressure and wage gains are growing at a robust pace, the bond market started the year with a steep selloff on anticipation that the central bank’s loose monetary policy is poised to be rolled back. Fed Chair Jerome Powell said the central bank will use its tools “to prevent higher inflation from becoming entrenched” at his confirmation hearing before the Senate Banking Committee on Tuesday.

“If we see inflation persisting at high levels longer than expected [and] we have to raise interest rates more over time, we will,” Powell told lawmakers. Other Fed officials have recently lent weight to the idea of raising rates in March, while advocating shrinking the central bank’s $8.8 trillion balance sheet later this year.

The bond market has looked past high inflation reports in recent months, with many expecting a moderation over the coming year as long-term disinflationary trends of technology, greater automation and aging populations offset the current pandemic-related pressure. Treasury breakeven rates over the next 5 and 10 years peaked last November and were down around 4 and 5 basis points, respectively, after the latest figures were released on Wednesday at 2.88% and 2.53% respectively.

“The Fed’s focus is not on CPI per se; its wages, and there are good reasons to expect higher wage inflation in the coming year,” said Steven Blitz, chief U.S. economist at TS Lombard. “The inflation psychology takes hold when people expect their wages will go up.”

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Michael MacKenzie