Samuelson, Friedman and the Debate that Shaped Economic Policy

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe greatest economic challenge of the second half of the 20th century was over how to fight the crippling inflation of the 1970s. It pitted the monetarist Milton Friedman against the Keynesian Paul Samuelson, and the debate between the two shaped economic thinking and policymaking to this day.

The British journalist Nicholas Wapshott’s Samuelson Friedman, a sequel to his earlier book, Keynes Hayek, promises an exciting Shootout at the OK Corral.

But it doesn’t deliver. (The silly book titles don’t help either.)

Nobel laureates Paul Samuelson, left of center, and Milton Friedman, firmly on the right,1 had much more in common than not – they were both passionate believers in the efficiency and rightness of the supply-demand-price system, which is the organizing principle for any voluntary economy. They were friends and admired each other’s work. While their policy views differed substantially, if they had not had alternating columns in Newsweek from 1966 to 1984, they would not have been cast as opposites in this or any book.

The two men differed on how large a role government should have in society. Don’t we all? Put two economists, or two political thinkers, or two ordinary citizens in a room and you’ll have at least three opinions on the question.

They also differed on whether Keynesian (Samuelson) or neoclassical (Friedman) economics painted a more accurate picture of the forces that shape the economy. In an interview, Wapshott said that Samuelson Friedman was conceived as a sequel to his earlier book, Keynes Hayek, which portrayed two men with similarly contrasting views.

Both men had weaknesses. Samuelson had an oddly soft spot for central planning and infamously forecast that the Soviet Union would overtake the U.S. economically by the 1980s. (He later updated his forecast to the 1990s and eventually abandoned it.) Yet Samuelson’s most renowned work in government was as an advisor to President Kennedy, a cold warrior and no leftist. Friedman’s greatest weakness, a rigid absolutism about monetary policy that set him on a collision course with President Nixon, was also his greatest strength; he did not bend with the political winds and stood firm in his convictions.2

Both men had weaknesses. Samuelson had an oddly soft spot for central planning and infamously forecast that the Soviet Union would overtake the U.S. economically by the 1980s. (He later updated his forecast to the 1990s and eventually abandoned it.) Yet Samuelson’s most renowned work in government was as an advisor to President Kennedy, a cold warrior and no leftist. Friedman’s greatest weakness, a rigid absolutism about monetary policy that set him on a collision course with President Nixon, was also his greatest strength; he did not bend with the political winds and stood firm in his convictions.2

A word on Nicholas Wapshott

Wapshott’s politics are refreshing: Until the end of the book, he takes no obvious side in the Samuelson-Friedman debate and goes out of his way to be fair-minded. He thus avoids the acrimonious tone that poisons many books on political economy. Having been a biographer of many apolitical people – actors Rex Harrison and Peter O’Toole, and director Sir Carol Reed, among them3 – Wapshott is comfortable being neutral. Interestingly, he has kept both his right- and left-leaning credentials burnished: He worked for Tory icon William Rees-Mogg at the Times of London and joined the neoconservative New York Sun as national and foreign editor in 2006, where he spoke admiringly of Ronald Reagan’s legacy; but he also writes for the socialist New Statesman and teamed up with celebrity editor Tina Brown to establish the lefty tabloid Daily Beast. It’s admirable to keep an open mind in the face of intense passions.

That said, the book builds toward a strong preference for Samuelson’s policies that Wapshott keeps well-hidden until he sums up the legacies of the two men in terms of their relevance to the cure for the global financial crisis of 2007-2009. In Wapshott’s view, Keynesian remedies ended a crisis that was caused by letting markets “run wild,” a policy he says that Friedman would have favored.4

Wapshott’s prose is not bad, but it doesn’t sparkle. You have to be interested in Samuelson and Friedman, not in the general debate framed by the two men, for Samuelson Friedman to hold your attention. In addition, as the popular economics professor and blogger Noah Smith said about the Keynes Hayek prequel, “You won’t learn much economics from this book, which is mostly an account of the lives and labors of its two protagonists.”5 That’s disappointing compared to what an author more interested in the history of economic thought could have delivered.

Because of this, I will focus on the economics of Samuelson and Friedman and less on the personalities.

About Paul Samuelson

The public face of Paul Samuelson (1915-2009) is his mega-successful Economics textbook,6 plus his Newsweek column. Among economists, however, he is regarded as possibly the greatest mathematical economist of all time. For the revolution he led in economic analysis, and for his lucid explanation of Keynesian theory, he won the 1970 Nobel Prize in economics, the first such prize won by an American.

Samuelson is also blamed by some for turning economics almost single-handedly from a storytelling discipline, akin to history, into a mathematical nightmare. The last time a top economics journal could be easily read by a non-specialist was in the 1950s, just before Samuelson’s influence peaked.7

Samuelson is also blamed by some for turning economics almost single-handedly from a storytelling discipline, akin to history, into a mathematical nightmare. The last time a top economics journal could be easily read by a non-specialist was in the 1950s, just before Samuelson’s influence peaked.7

At any rate, because of Samuelson’s ubiquitous textbook, a generation of undergraduates from the 1948 first edition to sometime in the 1960s learned (inaccurately) that Keynesian macroeconomics was the only theory that mattered. Then, while personally remaining a Keynes acolyte, Samuelson began to revise his book to reflect a more ecumenical approach, absorbing influences from Friedman and many others. His “neoclassical synthesis” integrated ideas from the older economics of the nineteenth century into the Keynesian framework. He also gradually began to include in his book alternative approaches to macroeconomics such as Austrian free-market economics, Marxian economics, and institutionalism.

Paul Samuelson on investing

Most mainstream economists haven’t contributed much to finance; Samuelson did so lavishly. He developed several of the seminal ideas defining modern portfolio theory and the understanding of investment risk. His 1965 paper, “Proof That Properly Anticipated Prices Fluctuate Randomly,”8 uses theory to demonstrate what Eugene Fama, at roughly the same time, demonstrated using data: it’s hard to beat the market. While Fama’s advocacy of efficient markets is better known, Samuelson’s is just as important in that (with James Tobin, Kenneth Arrow, and others) he established the microeconomic foundations of modern finance. Without these foundations, finance stands alone, separate from the rest of economic theory; with them, it is fully integrated into the larger world of economic thinking.

In a 1994 paper in the Journal of Portfolio Management entitled “The Long-Term Case for Equities (and How It Can Be Oversold),”9 Samuelson addressed time diversification. Many boosters of the long-term case for equities, notably Jeremy Siegel, have proposed that long-term investors face less risk than short-term investors because, in the long run, stocks have time to make up for short-term losses. Historically that has certainly proved to be true – at least in successful countries like the U.S. and U.K.10

But Samuelson countered, “Time spent waiting to recover from crashes is also time spent waiting for more crashes.” Thus, while stocks should be expected to beat bonds in the long run, there is no assurance that this will happen. The risk of being invested in the stock market does not disappear over time. Rather, in nominal terms, the stock market is riskier than fixed-income assets over all time horizons. In real terms, the stock market is still riskier than fixed income unless there is a hyperinflation or the serious threat of hyperinflation.11

Samuelson is correct. To have even the possibility of a high rate of return, an investor must take the risk associated with having a large weight in stocks. However, we must make this choice without relying on any belief that a long holding period eliminates or substantially reduces this risk.

This thinking places Samuelson, mostly celebrated for his macroeconomic insights, in the first rank of academic investment pioneers.

About Milton Friedman

While Milton Friedman (1912-2006) was as well-respected as Paul Samuelson as an economic theorist and empiricist, it’s in promoting the public understanding of economics that Friedman was at his best. He is pictured here in his natural habitat, which is in front of a TV camera. His explanations – of how capitalism and freedom are related, how choice empowers the consumer, and how monetary policy was to blame for the Great Depression and the great inflation of the 1970s – are timeless. He influenced a generation of young people, including the incredible 52% of University of Chicago undergraduates who, at the peak of his influence late in the twentieth century, chose economics as their major.12

While Milton Friedman (1912-2006) was as well-respected as Paul Samuelson as an economic theorist and empiricist, it’s in promoting the public understanding of economics that Friedman was at his best. He is pictured here in his natural habitat, which is in front of a TV camera. His explanations – of how capitalism and freedom are related, how choice empowers the consumer, and how monetary policy was to blame for the Great Depression and the great inflation of the 1970s – are timeless. He influenced a generation of young people, including the incredible 52% of University of Chicago undergraduates who, at the peak of his influence late in the twentieth century, chose economics as their major.12

Friedman the monetarist

Friedman is best known for turning the equation of exchange, an old concept expressed by the accounting identity, into a theory of how prices and inflation are determined. (This equation means that the quantity of money, M, times the velocity of money, V, equals the sum of the dollar volume all transactions in the economy, in any given period.) Friedman’s theory, called the quantity theory of money,13 says, all other things equal, an increase in the quantity of money will cause prices to rise by the same proportion. If Friedman’s theory is correct, and it certainly was at the time (it now requires modification because of changes in the institutional structure of the economy), we have a way to explain inflation and, if we can anticipate what the monetary authorities are going to do, a way to forecast it.

His classic 1963 work with Anna Schwartz, A Monetary History of the United States, 1867-1960, showed that the theory held up well over that period in the United States. It has been validated in other countries, including (to a first order) those that experienced hyperinflations such as Weimar Germany. Some recent research shows that the theory is incomplete in that it ignores the effects of fiscal policy that do not show up in the measured quantity of money, but that is a topic for another day.14

Friedman’s influence soared in the 1970s, after the predictions in his 1967 presidential address to the American Economic Association came true. In a PBS television appearance, he said,

[I]n the presidential talk I…argued that, if you tried to follow the policy of using inflation to try to cut down unemployment. you would end up with both more inflation and more unemployment…. [Y]ou can’t keep fooling the people all the time, and people will recognize what’s happening, and as they recognize what’s happening you’ll have to have more and more inflation to achieve that objective. And even that won’t work because people will catch on to it. And what happened in the 1970s [stagflation] was about as clear a demonstration of something that had already been predicted in advance as you could have.15

I’ll return to the 1970s inflation episode later, in the section on Samuelson’s and Friedman’s time in public service.

Friedman and investment management

Friedman was not a finance scholar, but his insights into money have influenced every investment manager. By “money,” I mean what Friedman meant at the time: currency in circulation plus checkable deposits in banks. These were (during Friedman’s lifetime) non-interest-bearing instruments that could be used to trigger a transfer of real resources. All other assets, real and financial, are “not money” and need to be paid for with money – and you would expect to be paid with money when you sell them.16

This bright line between money and other assets has since been blurred by the Fed’s payment of interest on reserves, and by the emergence of new sources of liquidity such as cryptocurrency and lines of credit backed by stock and bond portfolios and by real estate. Thus, Friedman’s quantity theory is not as directly applicable as it used to be. Even while Friedman was still alive and active, money market funds and other new financial instruments required an expansion in the definition of money for the purpose of estimating what inflation might be; we therefore have a whole family of monetary aggregates: M0, M1, and so forth through M6. But the basic principle, that the amount of money in circulation helps to determine the price level, remains sound.

Investment management requires estimates of future inflation for several reasons. One is that investors’ liabilities or spending plans are sensitive to inflation. Another is that inflation is incorporated into asset returns in different ways for different assets: unexpected inflation hurts nominal bonds, leaves the value of TIPS bonds unchanged, and typically hurts equities in the short run but not in the very long run. An industry of “Fed watchers” has grown up around the perceived ability to predict inflation, as well as real output, based on the actual or expected behavior of the monetary authority. While Fed watchers do more than just look at monetary aggregates to forecast inflation, it is an important part of their job.

In addition, labor and materials costs and consumer spending are affected by inflation, so it is important for investors to monitor monetary policy. Not all investment managers are monetarists in the Friedman sense, but all are aware of the importance of monetary policy and of resulting changes in the price level.17

Samuelson and Friedman in public service

I’ve drifted from my original goal, which was to appraise Wapshott’s narrating of the tension between the two great economists of the last half of the twentieth century. Let’s now return to the book and look at the area in which Samuelson and Friedman came into conflict the most, and where Wapshott focuses his attention: public service.

Samuelson and Friedman got their start in public affairs by advising John F. Kennedy and his presumptive 1964 opponent Barry Goldwater, respectively. While the two candidates differed on practically every economic issue, it was an amicable time; the candidates liked each other so much that they hoped to conduct the campaign together as a barnstorming tour – in Goldwater’s private plane. And both were engaging, charismatic fellows with a gift for oratory. It would have been the campaign of the century.

Alas, it was not to be. Kennedy was assassinated and his successor, Lyndon Johnson, had little interest in Samuelson’s theories, although he kept him on his team.

Meanwhile, Richard Nixon, another candidate with a limited interest in economics, rose to the top of the Republican Party and was elected president in 1968. Friedman would have been a natural advisor to the Republican who had defended free markets in his 1960 debates with Kennedy, but Nixon clashed with Friedman at every turn. Tevi Troy in The Wall Street Journal writes:

In September 1971, Milton Friedman attended a meeting at the White House with President Richard Nixon and George Shultz, who was then director of the Office of Management and Budget but had previously taught at Friedman’s University of Chicago. Nixon somewhat graciously tried to defend Shultz from Friedman’s free-market wrath, telling the professor that Shultz hadn’t been responsible for what Nixon called a “monstrosity” of a policy. Friedman’s response was blunt: “I don’t blame George. I blame you, Mr. President.”

Friedman never again visited the Nixon White House or spoke to Nixon, but he was right. The freeze would have disastrous effects. Fortunately, Friedman’s time advising presidents wasn’t over… After [Ronald] Reagan was elected president in 1980, a very important someone in Washington was once again listening [to Friedman].18

Friedman, Reagan, and Thatcher

The Reagan administration or, as Wapshott describes it, the tightly coordinated Reagan-Thatcher administration in the U.S. and U.K., adopted Friedman’s purist free-market message wholly. Reagan and Thatcher also adopted a hardline monetarist cold-turkey cure for the inflation that was then raging out of control (13.3% in the U.S. and 18.0% in the U.K. in 1980).

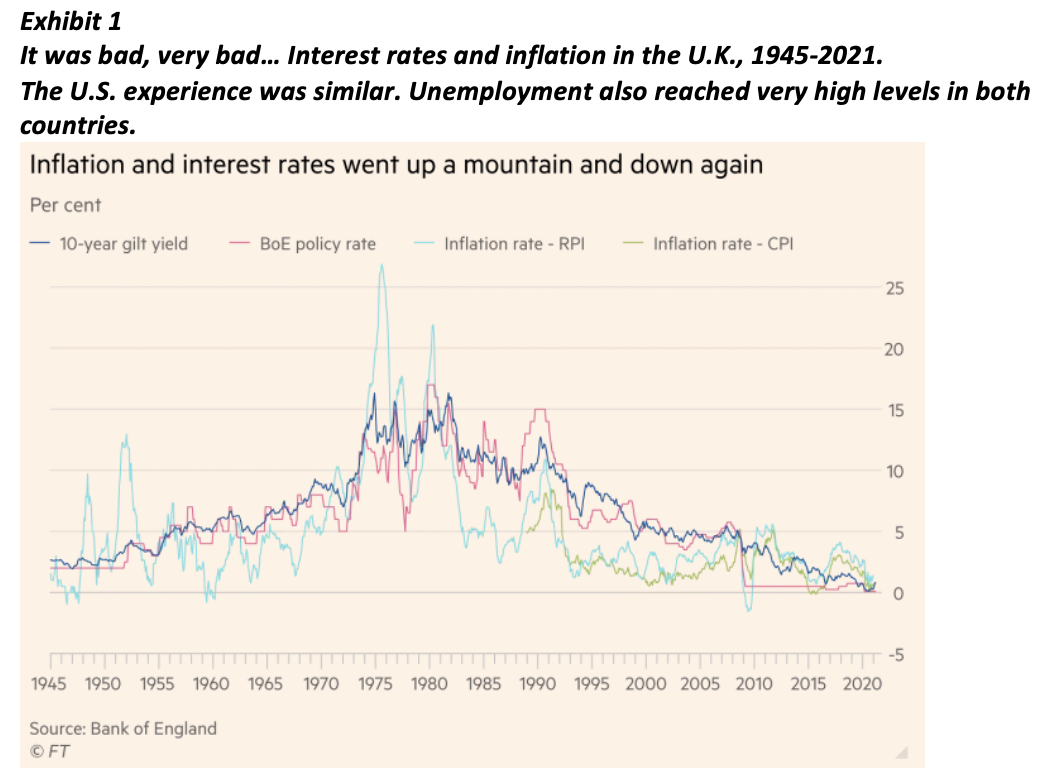

As Exhibit 1 shows, the cure involved sending both economies into a deep recession by hiking interest rates to unprecedented levels: 22% in the U.S. and 17% in the U.K.19

Younger investors who didn’t live through this period should study the exhibit closely. Many now think of the 1970s and early 1980s as a historical oddity – or they don’t think of them at all. I thought likewise of the crash of 1929 when I was a young analyst 40 or more years ago. I should not have done so, and younger investors should not do so now. It’s unlikely, but it could happen again.

The experiences of the U.S. and U.K. in this period were parallel but not identical. In the U.K., it took the 1978-1979 “winter of our discontent,” which was awful (see Exhibit 2), for the people to elect – out of desperation, a large Conservative majority whereby its leader Margaret Thatcher got Friedman’s policy prescriptions enacted.

U.S. President Jimmy Carter’s “malaise” speech, in which he didn’t use the word malaise but should have, reflected, as in the U.K., not only a decade of capital destruction and a wrenching dislocation in the labor market but a general sense that the country was declining, perhaps beyond the hope of recovery.

U.S. President Jimmy Carter’s “malaise” speech, in which he didn’t use the word malaise but should have, reflected, as in the U.K., not only a decade of capital destruction and a wrenching dislocation in the labor market but a general sense that the country was declining, perhaps beyond the hope of recovery.

The call for “somebody to do something” grew from a whisper to a roar – until somebody, the voters, did do something. And, in both countries, it was a monetarist and free-market prescription that stopped inflation and kicked off a generational bull market. But it also displaced old-economy workers, many of them forever. We are still feeling the reverberations of this disruption.

The economic ice bath worked wonderfully to bring down inflation. By 1983, the U.S. inflation rate had fallen to 3.1%, and the U.K. rate to 4.6% – but the sky-high interest rates required to bring down inflation froze the economy and generated equally sky-high unemployment. There was a widespread perception that the Friedman-Reagan-Thatcher team had overdone it.

Was there a less painful way to stop the destructive inflation of the 1970s and early 1980s? Probably not. Inflation happens because someone benefits from it: governments (which are typically net debtors), corporate and individual debtors, some trade unionists. To stop inflation, you have to stop providing those “rob Peter to pay Paul” benefits, meaning that Paul will be unhappy. Following a corollary of Frédéric Bastiat’s nearly 200-year-old maxim,20 those who are unhappy (with any given policy) scream bloody murder all day and night, and those who are happy sit quietly so as not to rock the boat. The inertia behind the status quo, in this case high and accelerating rates of inflation, is powerful.

When the ice bath began to have its effect, with inflation rates falling rapidly, there was concern among economists and politicians that the expected post-recession prosperity would kindle the inflationary fires once again, and that the wrenching economic adjustments that had brought down inflation would be for naught. There is some justification for pursuing the anti-inflationary policies with great vigor, as Reagan and Thatcher did.

But Wapshott does not think so:

But Friedman’s simple dogma, which seemed to make sense to a number of financial journalists, market analysts, and a clique in the Conservative leadership in the mid-seventies, ended its British life as an apologia postscript to a decade of unnecessary mass unemployment and painful lost opportunities.

Conclusion

The mismatch between the promise and delivery of the book begins with the subtitle, “The Battle Over the Free Market.” (When a book title or subtitle doesn’t match the contents, I charitably blame the publisher, not the author.) The tension in the book is between monetarist and Keynesian macroeconomic theory and policy, not between free and centrally directed markets. That latter battle is a much grander question, and while Friedman was as effective a defender of free markets we’ve ever had, Samuelson was equivocal, neither fully advocating central planning nor favoring Friedman’s nearly anarchic capitalism. Samuelson sensibly positioned himself as a centrist, favoring an only slightly modified form of capitalism. As a result, the contrast to Friedman doesn’t work.

Readers interested in the historic battles over how to fight the great inflation that peaked in the 1970s in the U.S. and the U.K. will find much of value in Samuelson Friedman. Those interested in the larger questions, including many raised by Friedman and Samuelson in their long and multifaceted careers as economists, should look elsewhere.

Laurence B. Siegel is the Gary P. Brinson Director of Research at the CFA Institute Research Foundation, the author of Fewer, Richer, Greener: Prospects for Humanity in an Age of Abundance, and an independent consultant. His latest book, Unknown Knowns: On Economics, Investing, Progress, and Folly, contains many articles previously published in Advisor Perspectives. He may be reached at [email protected]. His website is http://www.larrysiegel.org.

1Economically but not socially; Friedman was a libertarian, probably the best-known one of all time.

2But Friedman was not that inflexible: In https://www.thedailybeast.com/nicholas-wapshott-a-lovefest-between-milton-friedman-and-jm-keynes (gated but free to first-time viewers), Wapshott writes,

[In] his buried essay on Keynes, Friedman …[a]bruptly dismiss[ed] Hayek’s notion that big government tends to curb the rights of individuals… report[ing] that, in Britain, where government was administered with integrity and honesty, governments have grown large without endangering the public good.

From his time in England, Friedman learned that “Britain retains an aristocratic structure, one in which noblesse oblige was more than a meaningless catchword. Britain’s nineteenth-century laissez-faire policy produced a largely incorruptible civil service, with limited scope for action, but with great powers of decision within those limits. It also produced a law-obedient citizenry that was responsive to the actions of the elected officials operating in turn under the influence of the civil service.

While big government in Britain did not tend to be tyrannical, it was “very different in the United States,” which “has no tradition of an incorruptible or able civil service.” Quite the contrary...

The “buried” essay is https://www.richmondfed.org/~/media/richmondfedorg/publications/research/economic_quarterly/1997/spring/pdf/friedman.pdf.

3Also, oddly, the pop star George Michael (in a book co-authored with Wapshott’s brother Tim).

4Wapshott also, absurdly, blames the Trump presidency and the attempted “coup” of January 6, 2021 on the pernicious influence of Friedman’s small-government thinking. Friedman would have thought the anti-intellectual Trump repulsive. I suspect that none of the thugs and clowns who broke into the Capitol in 2021 had heard of Friedman or could explain why “that government is best which governs least” (Thoreau’s, not Jefferson’s, aphorism).

5http://noahpinionblog.blogspot.com/2012/11/keynes-hayek-by-nicholas-wapshott.html

6Still in publication and still mega-successful, with later editions co-authored with 2018 economics Nobel Prize winner William Nordhaus.

7In 1987 the American Economic Association founded a nontechnical or “storytelling” journal, the excellent Journal of Economic Perspectives, specifically to address that problem. A few specialties in economics, especially economic and business history and the history of economic thought, are still (somewhat) nonmathematical.

8Samuelson, Paul A. 1965. “Proof That Properly Anticipated Prices Fluctuate Randomly.” Industrial Management Review, Vol. 6 (Spring), pp. 41-49. Note that this groundbreaking finance paper was published in a fairly obscure journal even though Samuelson was probably the world’s best-known economist at the time. I’m guessing that is because mainstream economics journal editors didn’t think finance was in their bailiwick.

9Samuelson, Paul A. 1994. “The Long-Term Case for Equities.” Journal of Portfolio Management, Vol. 21, issue 1 (Fall), pp. 15-24.

10An extensive literature on “survival bias” asks whether the experience of long-term successful countries like the U.S. and U.K. is representative, or more likely, upward biased in that it overstates the returns that can be expected when you don’t know in advance whether a country’s stock market will succeed. See various chapters in Goetzmann, William N., and Roger G. Ibbotson, 2004, The Equity Risk Premium: Essays and Explorations, Oxford, UK: Oxford University Press.

11The discussion in this and the next paragraph is paraphrased from Siegel (1997), which I wrote after I heard Paul Samuelson speak on the topic. Siegel, Laurence B. 1997. “Are Stocks Risky? Two Lessons.” Journal of Portfolio Management, vol. 23, no. 3 (Spring), pp. 29-34.

12Personal communication from the Dean of the College, John Boyer. (He thought the percentage should be lower, and it now is.) Full disclosure or true confession: I applied to the University of Chicago from high school in hope of studying with Friedman, but when I found out how tough a grader he was, I only audited the course. I nevertheless became acquainted with him through other channels. He had such a casual manner that when I met him for the first time, I thought maybe I was meeting a different short Jewish man in his sixties; I expected a dominating personality, but he was modest and kindly. He signed my dorm’s MonopolyTM board, adding the flourish “Down with monopoly!”

13Friedman was not the first to call this the Quantity Theory of Money, but he is the person most closely associated with it.

14See Cochrane, John H. The Fiscal Theory of the Price Level. Book draft, https://www.johnhcochrane.com/research-all/the-fiscal-theory-of-the-price-level-1. The Cochrane book is very long and technical. With two colleagues, Thomas Coleman and Bryan Oliver, both of the University of Chicago, I am writing a short, nontechnical book about the Fiscal Theory, part of which will soon appear as a brief on the CFA Institute Research Foundation web site, https://www.cfainstitute.org/en/research/foundation/publications.

15https://www.pbs.org/fmc/interviews/friedman.htm (undated).

16In the classic textbook explanation, this is the “medium of exchange” function of money. The other functions are as a unit of account and a store of value.

17I am mostly referring to active managers, including those who allocate actively between asset classes, but I really think all managers should be aware of monetary policy and its consequences because every pool of assets is gathered to pay for some sort of spending, which is affected by inflation.

18https://www.wsj.com/articles/milton-friedman-nixon-reagan-free-market-price-controls-11629327291

19These are short-term, central bank interest rates. Long-term bond yields peaked at 15.8% in the U.S. and 16.3% in the U.K.

20Bastiat said (I paraphrase) that any policy that benefits a small group of people will be sought by those people with great passion and effort, while it will only be opposed very mildly by those paying for it because that particular policy will only cost them a few sous (pennies). So government naturally grows and grows. My example of Paul being vocally unhappy when his ox is being gored is the back side of the Bastiat principle.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All