Given their small size, narrow focus and high degree of specialization, it is reasonable to expect that active sector funds generate alpha. New research shows this is the case – but with a lot of caveats.

Given their small size, narrow focus and high degree of specialization, it is reasonable to expect that active sector funds generate alpha. New research shows this is the case – but with a lot of caveats.

Studies such as the S&P Active Versus Passive Scorecards (SPIVA) persistently show that the vast majority of active managers fail to outperform their risk-adjusted benchmarks and that there is little evidence of persistence of performance beyond the randomly expected.

But sector funds are generally smaller and have not yet experienced the well-documented diseconomies of scale in active management. Their narrow sector focus should give them a skill advantage – they develop domain knowledge about a narrow universe of firms with similar business operations and can therefore more easily identify the winners and losers in their target sectors.

Huangyu Chen and Dirk Hackbarth sought the answers to those questions with their study “Active Sector Funds and Fund Manager Skill,” published in the September 2020 issue of The Journal of Portfolio Management. They limited their study to sector funds that reside under a single fund family. This allowed them to control for the organizational diseconomies of scale in the active fund management industry. As benchmarks, they used the S&P 500 Index and 10 passively managed sector ETFs from SPDR, whose underlying stocks reconstitute the S&P 500 Index. To examine factor exposures, they employed three asset pricing models: the five-factor model from Fama and French (2015), the four-factor model from Carhart (1997), and the investable-index four-factor model proposed by Cremers, Petajisto and Zitzewitz (2013). The resulting data sample was 40 Fidelity active sector funds and covered the period September 1998 to June 2016.

Following is a summary of their findings:

- A passive indexation strategy equal weighting (and monthly rebalancing) the 40 actively managed sector funds earned an annual benchmark-adjusted (using the S&P 500 as the benchmark) return of 5.70% and a monthly alpha of 27 bps.

- The strategy’s outperformance is present in market downturns (i.e., resilient to tail risk) and robust to change of rebalancing frequency and inclusion of expenses.

Their findings led them to conclude: “Efficient diversification and underappreciated skill, illustrated by an alpha-arithmetic to guide similar strategies, explain the strategy’s success.” In other words, investors don’t appreciate the skill of these active-sector--fund managers. Thus, they under-allocate to them. The result is that the funds don’t face the diseconomies of scale that larger funds face. And the equal weighting diversifies individual manager and sector risks.

Before jumping to any conclusion, a few issues with the study should be considered:

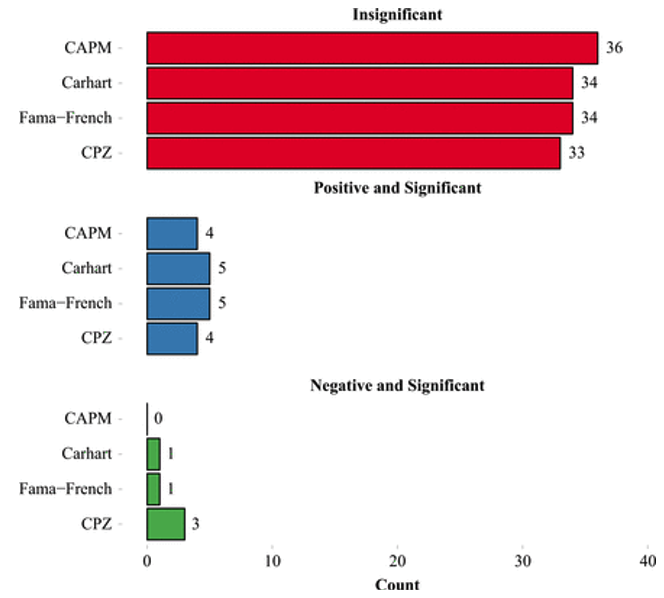

- As the authors noted, while an equal-weighted portfolio of sector funds outperformed, “Active sector funds individually show only weak evidence of selection skill.” As illustrated in the chart below, the large majority of the active sector funds failed to show statistically significant alphas. Depending on the asset pricing model used, between 33 and 36 of the 40 active sector funds failed to generate statistically significant alphas, and as many as three showed statistically significant negative alphas. A maximum of five showed statistically significant positive alphas.

- In examining how the equal weighting of sector funds influenced the outcome, with monthly rebalancing the equal weighting of the 40 active funds did outperform the S&P 500 by a statistically significant 5.7%. However, the equal-weighted sector ETFs also outperformed the S&P, although by a lesser 3.7%. Thus, the outperformance is reduced by almost two-thirds when comparing the strategy to the equal-weighted sector ETFs instead of the S&P 500. And while the remaining difference in performance of 2% is economically significant, the difference in returns was no longer statistically significant (t-stat = 1.7). The lack of statistical significance is especially important in light of the large degree of freedom the authors had in choosing their data set. I’m not accusing the authors of data mining; however, at the very least, one should examine the performance of other active sector funds before drawing any conclusions.

- When we examine the returns against the factor models, we find that against the Fama-French five-factor model, the alpha of the equal-weighted active sector fund strategy is basically cut in half, from 27 bps per month to 14, and is not statistically significant at the 5% confidence level (although it is close). Again, we should consider the degrees of freedom in designing the test. And while the alpha is a statistically significant at 22 bps per month using the Carhart model, that model does not consider profitability. The regression against the Fama-French five-factor model does consider profitability, and it shows a statistically significant loading on that factor. Thus, the statistically significant alpha measured using the Carhart model could be explained by exposure to profitability.

- The funds with the highest alphas have the highest volatility of those alphas. As the authors noted, this is part of the conundrum of identifying funds with alpha ex ante. They also showed that the factor loadings of the individual funds showed wide dispersions on market beta, as well as other common factors, demonstrating the importance of diversification across funds.

- The relatively short sample period, 1998-2016, with only two major U.S. equity market downturns, may cast doubt on the robustness of their finding of outperformance during downturns.

- While the 10 SPDR ETFs are based on the GICS sector classification, and Fidelity follows the GICS classifications, the 40 funds are at different levels in the classification structure. For example, there are GICS sector funds, like Energy (FSENX), Industrials (FCYIX) or Consumer Discretionary (FSCPX) but also several industry group or industry funds. For example, within consumer discretionary, there are separate funds for automotive (FSAVX), leisure (FDLSX) and retailing (FSRPX). Some funds, like gold (FSAGX), are even at the subindustry level (this one within the materials GICS sector). The 40 Fidelity funds do not seem to systematically cover different levels of the GICS classification system, such as having one fund for each GICS industry. For example, consumer staples has a sector fund but no additional industry or subindustry funds. As a result, equally weighting the 40 sector funds will not produce the same sector compositions as equally weighting the 10 SPDR sector ETFs.

In summary, the authors themselves stated: “The outperformance of mutual funds is hard to capture. Although some funds do earn higher benchmark-adjusted returns compared with the EWS [equal-weighted sector] strategy, it is a formidable task to predict in advance which will be best.” Their results are certainly interesting. However, unless an investor was willing to build an equal-weighted portfolio of 40 Fidelity active sector funds and rebalance them, the results don’t have any practical relevance, even without considering the statistical issues raised. It would also be interesting to see how the results hold up out of sample. Hopefully, this paper will stimulate further research.

Larry Swedroe is the chief research officer for Buckingham Wealth Partners.

The information in this article is for educational purposes only and should not be construed as specific investing, accounting, tax, and legal advice. Indices are not available for direct investment. Their performance does not reflect the expenses associated with an actual portfolio nor do indices represent results of actual trading. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. R-20-1269

Read more articles by Larry Swedroe

Given their small size, narrow focus and high degree of specialization, it is reasonable to expect that active sector funds generate alpha. New research shows this is the case – but with a lot of caveats.

Given their small size, narrow focus and high degree of specialization, it is reasonable to expect that active sector funds generate alpha. New research shows this is the case – but with a lot of caveats.