Economic indicators suggest that the 10-year Treasury yield could double to nearly 2%, according to Jeffrey Gundlach, and the U.S. could face higher inflation over the next several years.

Economic indicators suggest that the 10-year Treasury yield could double to nearly 2%, according to Jeffrey Gundlach, and the U.S. could face higher inflation over the next several years.

Gundlach spoke to investors via a webcast, which he titled “No End in Sight,” and the focus was on his flagship total-return fund (DBLTX). Slides from that webcast are available here. Gundlach is the founder and chairman of Los Angeles-based DoubleLine Capital.

Since the onset of the pandemic, the yield on the 10-year Treasury bond has not exceeded 1%, although it nearly got there in late May and was at 92 basis points when Gundlach spoke. He warned that if the yield breaches the 1% “resistance level,” it could easily rise to 2%.

In that scenario, the only thing that could arrest further increasing rates would be yield-curve control, whereby the Fed would purchase longer-dated bonds, according to Gundlach.

Moreover, he said, fundamentals do not support today’s Treasury rates. The performance of cyclical/defensive equites and the copper/gold ratio say the 10-year yield should be 2%, according to Gundlach.

He said that now would be a good time for first-time home buyers to take a mortgage, while rates are low.

Gundlach expects inflation will be in the “2.25% range” next year. But it is a “good bet” that inflation will be higher than the mortgage rate of 2.92% over the next several years, he said. That would happen if the Fed went to “true money printing,” which Gundlach defined as “making its debt legal tender.” Until now, the Fed has injected liquidity into the financial system mostly by purchasing bonds, such as through quantitative easing (QE), and not by directly sending money to Americans.

But Gundlach said that there “hasn’t been any inflation” this year and he sees no reason to believe fiscal or monetary policies will lead to it.

Inflation expectations are elevated based on the Conference Board metrics, he said, but are lower in Michigan consumer survey data. The N.Y. Underlying Inflation Gauge has reliably predicted inflation, he said, and it is showing very subdued inflation pressure. The five-year break-even inflation rate has risen from a low of 0.18% in March to 1.85%, but it is still below the Fed’s traditional target of 2%.

Inflation is about the same at yield on 30-year bonds, meaning that its real yield is zero, and much higher than the five-year yield.

A struggling economy

Gundlach gave an overview of a struggling U.S. economy.

He said the COVID case count is declining – slightly – and the case patterns in the U.S. are trailing Europe by a couple of weeks. Deaths in Europe have peaked, but not yet in the U.S.

He is worried about skepticism about vaccines in the U.S. and Europe, especially in France. Even if it is free, he said about a third of Americans are hesitant to take one.

Mobility data, which track the movement of people, has not improved since May or June.

Restaurant activity is down 60% year-over-year, and he fears significant small business closings now that outdoor dining has closed.

Hotels are operating at about 40% of pre-COVID levels, and travel, based on TSA data, has been cut in half, Gundlach said.

“Even LAX was empty for Thanksgiving,” he said.

On a calendar-year basis, the worst economic contraction in the U.S. was in 1932. But 2020 ranks in ninth place, about same as 1919, a century ago after the Spanish flu epidemic.

Public debt, an ongoing source of concern for Gundlach, has risen dramatically as a percentage of GDP. It has surpassed its WWII high. Mortgage debt came down this year, he said, but that was more than offset by the rising federal and state government deficits.

The “law of economic physics,” which is confirmed by the data, shows that incremental debt produces less marginal GDP growth, he said.

The velocity of money supply (M2) has been collapsing, and has fallen in half since the onset of the COVID crisis.

Average hourly earnings have risen this year, but that is because job losses were concentrated among low-paying occupations, according to Gundlach.

“The economy is living off of government support,” he said. In reference to the title of his presentation, he asked, rhetorically, “Will there be any end?” The “mindset,” he said, is to continue that support. It has led to a spike in disposable income, which has generated a divergent response across sectors of the economy; travel and entertainment have suffered, but other consumer purchases have risen.

Government benefits as a percent of household income went from 10% to 24% as a result of response to the COVID crisis. It came down a bit, he said, but will go up if there is another fiscal stimulus.

“This does not lead to a healthy economy or a harmonious society,” Gundlach said, because so many people are relying on government support.

There is some good news. Consumer-loan and car-loan write offs and delinquencies are down, in part because fewer people need auto transportation. Gundlach called this a “very unusual situation,” which is as a result of government actions.

Consumers still lack confidence in the economy, as measured by the Conference Board indicators. People are worried that government programs might end, he said.

Retail sales took a “big divot” starting in March, he said, but now are back to pre-COVID levels. But people are spending a lot more on durables than on services (due to cutting back on restaurant and travel spending).

Market implications

With the increased federal debt, Gundlach said his call with his greatest conviction is a weak dollar. That started early this year, as the dollar went from 103 to 91 on DXY index, weakening particularly against the euro and some emerging-market currencies.

“The amount of debt in the U.S. is responsible for this,” he said, as are reduced bond purchasing by foreigners and pension plans.

He said he had another high conviction call early this year, which was to buy bitcoin. It is now at approximately 19,000, and has performed much better than gold.

He showed a chart on the China Credit Impulse, an indicator which he said leads industrial metals. It has been increasing this year, which presages strong performance for emerging markets.

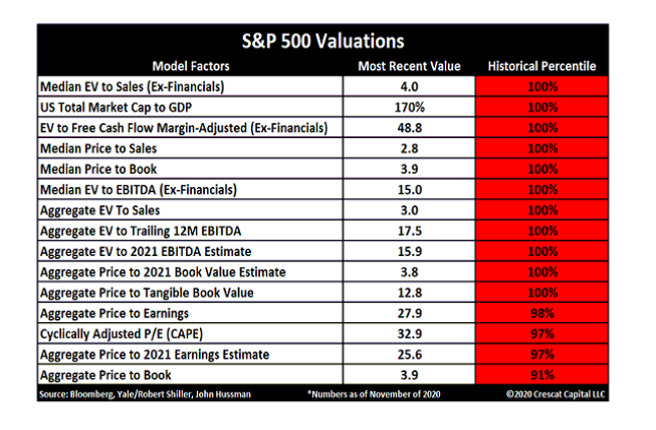

The U.S. stock market is at its all-time high based on the ratio of market capitalization to GDP. “This is clearly a non-undervalued stock market,” he said. It is at the highest valuation across a range of metrics:

There has been a change in the performance in U.S. equities. The FAANGs plus MSFT had outperformed the S&P 500 by 50% since September 2019. But that has “rolled over,” he said, and the “generals may have abandoned the army.”

He showed an indicator based on S&P 500 earnings 24 months in the future. Even that indicator shows valuations at dot-com-lock levels.

The Russell 2000 small-cap index has performed better relative to the overall market over the last month, which Gundlach called a “powerful move.”

He said he is “starting to see a reversal,” with the moves in the dollar, FANGS and small caps.

U.S. equity performance continues to dominate the rest of the world, particularly over the last 10 years.

But Gundlach said that emerging market performance will be superior to the S&P 500 going forward.

DoubleLine on the move?

Gundlach said that he has heard that as many as 700,000 people have moved from California as a result of the pandemic and its 12.3% income tax rate.

He isn’t moving his firm from California, because other states, like Florida and New Hampshire, will impose income taxes as they develop the infrastructure to support businesses moving there.

Plus, he already has a house in Buffalo.

But if California raises its income tax to 16.8%, which is being discussed, he said he will look more closely at moving.

More Global Markets Topics >

Economic indicators suggest that the 10-year Treasury yield could double to nearly 2%, according to Jeffrey Gundlach, and the U.S. could face higher inflation over the next several years.

Economic indicators suggest that the 10-year Treasury yield could double to nearly 2%, according to Jeffrey Gundlach, and the U.S. could face higher inflation over the next several years.