European sovereign debt issuers are in the land of milk and honey, racing to get as much as possible of this year’s issuance completed before the summer lull. With so much monetary stimulus sloshing about, governments even have an eye on getting ahead of next year’s budget plans as well.

The European Central Bank’s latest 600 billion-euro ($683 billion) batch of quantitative easing, and the European Union’s (still to be agreed) pandemic recovery fund, have created perfect conditions for a debt-raising bonanza. Given the deep uncertainty about how quickly economies will rebound from the coronavirus lockdowns, and whether there will be a second wave of Covid-19, it would be foolish for issuers to miss out on a golden moment.

Investors are piling into bonds right now as yields are still slightly higher than they were before the crisis, even though the markets have been more stable than in the early days of the lockdowns (at least until Thursday’s rout). This incentive might not last, once the wall of ECB money starts to hit.

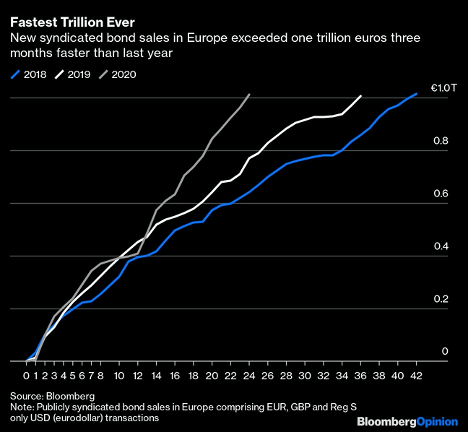

This happy confluence of keen sovereigns and eager investors is creating record order books for bond issues, and is allowing issuers to sell debt at longer maturities. Total syndicated bond sales — where a group of banks runs the process — have broken the 1 trillion-euro ($1.14 trillion) barrier at the earliest time of the year ever.

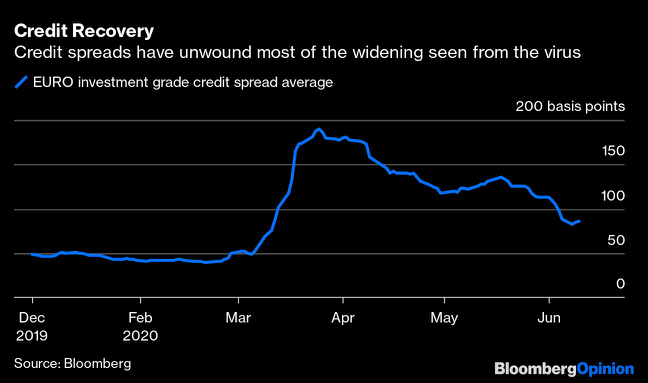

New issues that offer a juicy premium, when compared with similar existing debt, are especially popular. But this will doubtless all change as the ECB’s overall 1.35 trillion-euro QE program is increasingly put to work. Sovereign yields might fall and credit spreads (the difference between corporate bond yields and their benchmarks) might tighten further. The ECB has bought almost every eligible new corporate deal recently.

Raising money via syndicated issues is clearly catching on for governments, who have tended in the past to prefer auctions. These sales comprise nearly a third of all government debt issued this year. It may be a marginally more expensive process because of the investment banker fees but it’s a surer way of gauging demand for bigger and longer-maturity issues.

This week alone has seen syndicated issues by Germany and the U.K. of 30-year maturities, 20-year sales by Spain and Finland, and 10-year issues from Ireland, Croatia and Greece. Tuesday was a record day for European syndicated issuance, with 21 deals raising more than 40 billion euros.

Italy brought a 14 billion-euro 10-year syndicated deal last week, with a record order book of more than 107 billion euros. Rome has raised nearly 50 billion euros in just three weeks, bringing its bond sales so far this year to 290 billion euros. That’s 40% quicker than last year’s fundraising pace. Italy is so confident that it plans to issue a new type of retail investor bond, called the BTP futura, next month. That’s what the unequivocal backing of the ECB does for a country, regardless of their fundamental weakness.

Although European sovereigns are having to raise their fund-raising substantially to cover the spiraling lockdown costs, they are still getting ahead of their annual debt-issuance targets. Spain has already done three-quarters of its necessary bond sales. Belgium is in a similar position.

Nonetheless, the summer months do quieten down in the markets. As state borrowing requirements are only going up, it makes sense to load up now. This window won’t stay open forever.

Bloomberg Opinion provided this article. For more articles like this please visit bloomberg.com/opinion.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Marcus Ashworth