Robert Gordon dismissed concerns that the stock market is in a bubble and further predicted that the unemployment rate will drop to below 3%.

Robert Gordon dismissed concerns that the stock market is in a bubble and further predicted that the unemployment rate will drop to below 3%.

Gordon is a highly distinguished economist and professor at Northwestern University with a lifelong interest in productivity growth. He spoke at the NABE 60th Annual Meeting in Boston on September 30, you can view the presentation slides here.

I will explain why Gordon said we should expect a recession in 2020-2021, but first let’s look at why’s he doesn’t believe there’s a stock market bubble.

The economy’s stable expansion will continue in 2019

The current economy is at a “golden” moment, Gordon said, and is undergoing a stable expansion.

Throughout the recovery, we have had an extended period of low inflation at or below the Fed’s target of 2%. The average GDP growth rate was 3% in the first half of the year.

We have also seen a consistent decline in unemployment, dropping from 10% in October 2009 to 3.9% in August 2018. Labor markets are tightening across the U.S. economy, Gordon added. There are 18 U.S. states currently reporting unemployment rates at 3.5% or below.

How low can unemployment go? According to Gordon, “we’ve got a ways to go still.”

He predicted that job growth will continue, and the unemployment rate will go on to fall below 3%.

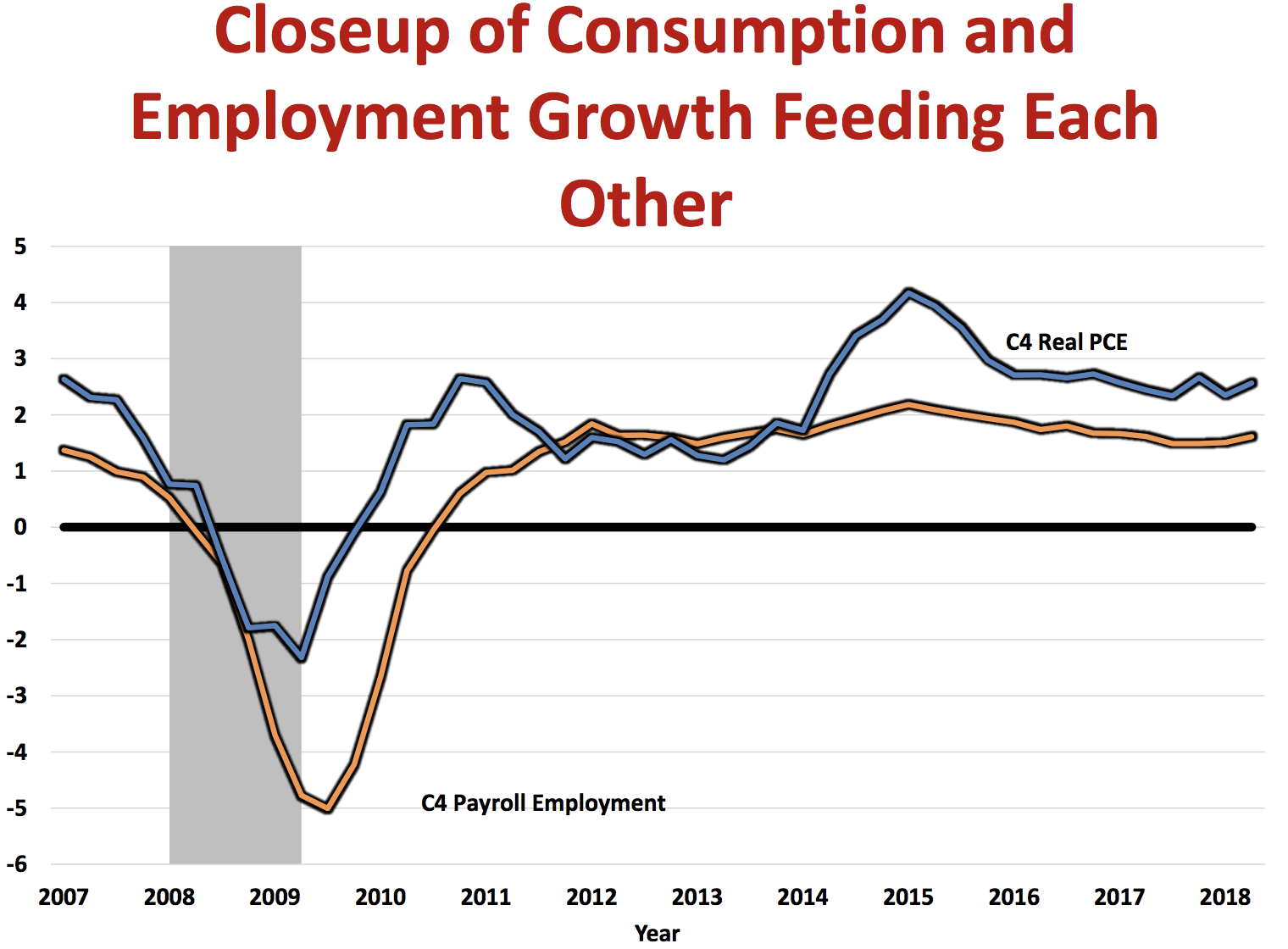

In the last four years, the growth in employment has been incredibly stable, Gordon said. In that time, consumption has grown steadily at a higher rate than employment.

This is a healthy sign that the two expansionary economic forces are feeding each other, Gordon explained. When employment growth generates a rise in income, it translates to higher consumption levels. This virtuous cycle generated the consistent 2% GDP growth, and we can expect that 2% growth to be generated every year until something slows it down, according to Gordon.

This is a healthy sign that the two expansionary economic forces are feeding each other, Gordon explained. When employment growth generates a rise in income, it translates to higher consumption levels. This virtuous cycle generated the consistent 2% GDP growth, and we can expect that 2% growth to be generated every year until something slows it down, according to Gordon.

Current expansion into next year

“What’s unique to the current expansion,” he said, “is that deficits are getting bigger very late in the expansion.” Historically, fiscal deficits grow during economic downturns, not during expansions.

Last year we had the steady 2% GDP growth rate that we’ve had for years. When this was boosted by fiscal stimulus, he said, it accelerated the expansion. We have already seen GDP growth jump from 2% in 2017 to 3% for the first half of 2018.

That 1% jump from fiscal stimulus can be broken out into two sources of added growth, according to Gordon. The tax cuts added 0.3% GDP growth 2018-2019. The budget expenditures added 0.8% GDP growth 2018-2019.

According to Gordon, investors can expect to see the 3% expansion we have now to repeat again next year, since nothing will be slowing it down and the boost from fiscal stimulus will still be there.

Along with that repeated 3% growth next year, Gordon said, investors can expect an added boost to the expansion from the stock market.

The S&P 500 has increased 36% since Nov 8, 2016. “The increase in the stock market that has already happened will raise GDP growth by 0.5%.”

The expansion driven by fiscal policy and the stock market will cause GDP growth to accelerate from the steady 2.0% growth we’ve had for several years to 3.5% GDP growth.

“I don’t see how a recession can start by 2020,” he said, “I think 2019 is in the bag.”

Why the bears are wrong

Gordon and Wharton professor Jeremy Siegel are among a small minority of scholars and analysts who aren’t concerned about market overvaluation and are instead predicting high returns.

“It’s not patently obvious we’re in a stock market bubble,” Gordon said.

“Clearly increases in stock market returns will be less, if not zero, going forward,” he said. But the idea that we’re on the verge of a 30-40% decline in the stock market is way too pessimistic, according to Gordon.

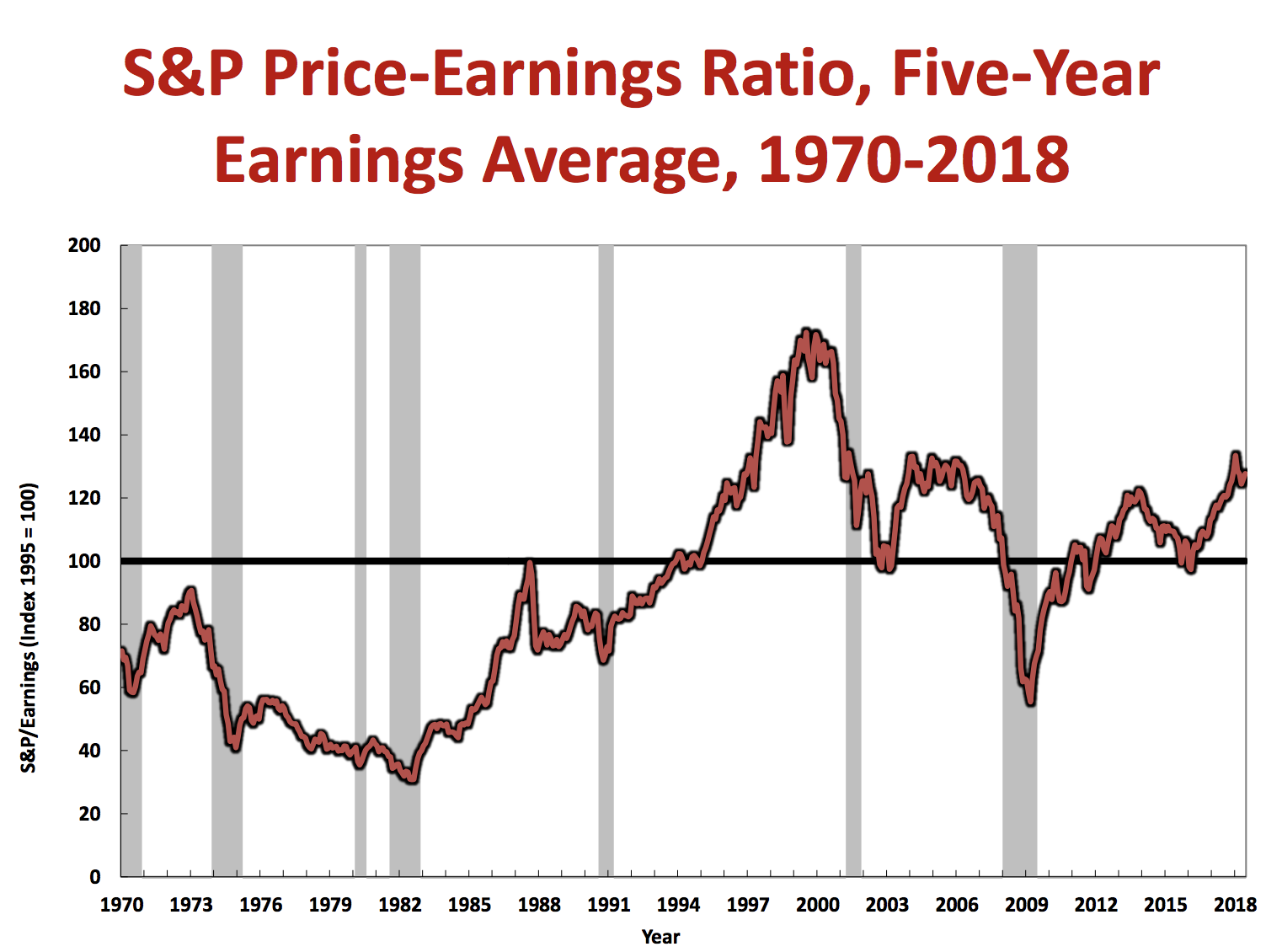

Gordon echoed recent remarks by Siegel and argued that the cyclically adjusted price-to-earnings (CAPE) ratio, conceived by Yale professor Robert Shiller, does not provide a valid forecast of future prices.

“It’s crazy to look at the Shiller index,” Gordon said, because the trailing 10-year earnings average overweighs poor performance during the financial crisis.

“It’s crazy to look at the Shiller index,” Gordon said, because the trailing 10-year earnings average overweighs poor performance during the financial crisis.

“Instead look at price-earnings ratio with a five-year earnings average 1970-2018,” he said, “and now this doesn’t look so bad.”

Gordon’s prediction: Monetary policy will be the expansion killer

Nouriel Roubini, also dubbed “Dr. Doom”, recently predicted that by 2020 we will be ripe for a financial crisis, which will be followed by a global recession.

Roubini released his list of ”expansion killers,” the 10 reasons why he believes the next crisis is a couple years away. Fiscal and stock market reversals are Roubini’s the top concerns.

But according to Gordon, the reversal of fiscal and stock market stimulus will not send us into a recession. It will just remove the “spur” from 2% to 3% growth, he said.

Gordon’s nominee as the number one expansion killer is the Federal Funds rate. Monetary policy and inflation are what could make the market crash, he said.

As long as there’s not a significant upturn in inflation in the Fed’s forecast, we’re going to see a modest continued rise in short-term rates up to the 3% range, Gordon said. “But that’s contingent on a Federal Reserve inflation forecast that is simply out of this world,” he said.

The Fed is forecasting 2% core PCE inflation for this year, and 2.1% for 2019-2020. That is “simply unbelievable,” according to Gordon, who noted core PCE inflation has already accelerated.

For the Fed’s forecast to be right, Gordon explained, the unemployment rate needs to continue to drop at the rate it has been dropping. It assumes the unemployment rate will go down below 3% and drop further at its existing pace, when since 2009 the unemployment rate has already declined from 10% to 3.9%.

According to Gordon, even if employment did grow as needed, it would require an unlikely bounce back of productivity growth to offset tightness in the labor market. That is the only way to reach the consensus GDP forecast, he said.

As unemployment goes down, we’ll get higher inflation, “rising above the benign almost unbelievable forecast by the Fed that inflation is going to stay where it is for the next 2.5 years.”

Gordon predicted that the higher inflation will shake financial markets even before the Fed acts.

According to Gordon, when this starts to happen, the Fed will react by raising rates faster than markets expect. This will cause markets to have a tantrum, he said, marking the end of the expansion period.

However, he said, the markets won’t drop by half as much as they did in the last two recessions. It will result in a mild recession, but not a financial crisis, he said.

Marianne Brunet is a financial markets analyst at Advisor Perspectives.