Jerry Miccolis is the chief investment officer of Giralda Advisors LLC and the lead portfolio manager of The Giralda Fund (GDAMX) and Giralda Risk-Managed Growth Fund (GRGIX). He maintains a focus on applying innovative risk management techniques with a goal of delivering long-term capital appreciation to investors while also protecting against the effects of adverse market conditions.

Jerry has more than four decades of experience in the risk management, actuarial, and investment management fields, and he shares his expertise through various publications, speaking engagements, and as the co-author of the book Asset Allocation For Dummies®. Prior to joining Giralda Advisors, Jerry was a principal at Brinton Eaton Wealth Advisors and, prior to that, a principal and global practice leader of the enterprise risk management (ERM) consulting practice at Towers Perrin.

Jerry has a bachelor’s degree in mathematics from Drexel University. He holds the Chartered Financial Analyst® designation, is a CERTIFIED FINANCIAL PLANNERTM practitioner and is a fellow of the Casualty Actuarial Society (FCAS). He is also a Member of the American Academy of Actuaries, the Financial Planning Association (FPA) and the New York Society of Security Analysts (NYSSA). He received the Chartered Enterprise Risk Analyst® certification for his pioneering work in the ERM field. He has chaired several professional committees and is a widely quoted author and speaker on the subject of strategic risk management, investment management, and their interaction.

I spoke with Jerry on May 9.

You have two funds - The Giralda Fund (GDAMX) and Giralda Risk-Managed Growth Fund (GRGIX) – that were introduced approximately five and two years ago, respectively. What is the history of your firm and what led to the introduction of those two funds?

Giralda Advisors was born inside of a wealth management firm, Brinton Eaton Wealth Advisors, based in New Jersey. We created the original flagship fund, The Giralda Fund, for Brinton Eaton’s wealth management clients for their exclusive use. We developed a risk-managed equity strategy for them, and it turned out that the most efficient way to deliver it to them was through a ’40 Act fund, so we created one in the summer of 2011. We ran it solely for those clients for a number of years.

The fund (GDAMX) established a solid track record over the years. It was doing well against its objectives. We knew based on conversations with other wealth advisors that there would be some interest outside of Brinton Eaton, so we later launched the separate fund, the Giralda Risk-Managed Growth Fund (GRGIX), for that potential audience.

The only difference between the two funds is the fee structure. In the original fund, GDAMX, since it was launched within a wealth management firm, the management fee within the fund was waived for Brinton Eaton clients. For outside clients, clearly we did want to charge a management fee. You can’t have two share classes within a single fund that charge two different management fees, so we created the clone fund, GRGIX, for that purpose.

Giralda Advisors is the investment advisor to both funds. It was created as a spinoff from Brinton Eaton and is now a separate entity.

Giralda’s tag line is risk-managed investing. What does that mean?

We provide exposure to domestic large-cap equities and add several layers of downside risk management. More specifically, there are two types of risk that you face with equities. One is recurring bear market risk and the other is a sudden, “nobody saw it coming” market crash. The 2000-2002 period is an example of the first and 2008 is an example of the second. We have two different types of risk management devices to address each of those equity-market risks, respectively.

What sent you down the road of risk-managed investing?

We were at Brinton Eaton Wealth Advisors in the wake of the 2008-2009 market crash. Our clients needed to be in equities for their long-term financial health, to make their financial plans work and keep them ahead of inflation. But many clients who needed to be in equities were now afraid of doing so.

We set about finding a way to keep them in equities and allow them to sleep at night. We spent over a year looking for solutions in the market, doing our own research and analysis, and ultimately developed our own strategy, to allow clients to stay in equities but attempt to mitigate the most dangerous of those downside risks.

Let’s talk about how it seeks to mitigate those risks. Can you talk about the portfolio composition of the funds?

The composition of the funds is the same; each contains two separate risk management devices.

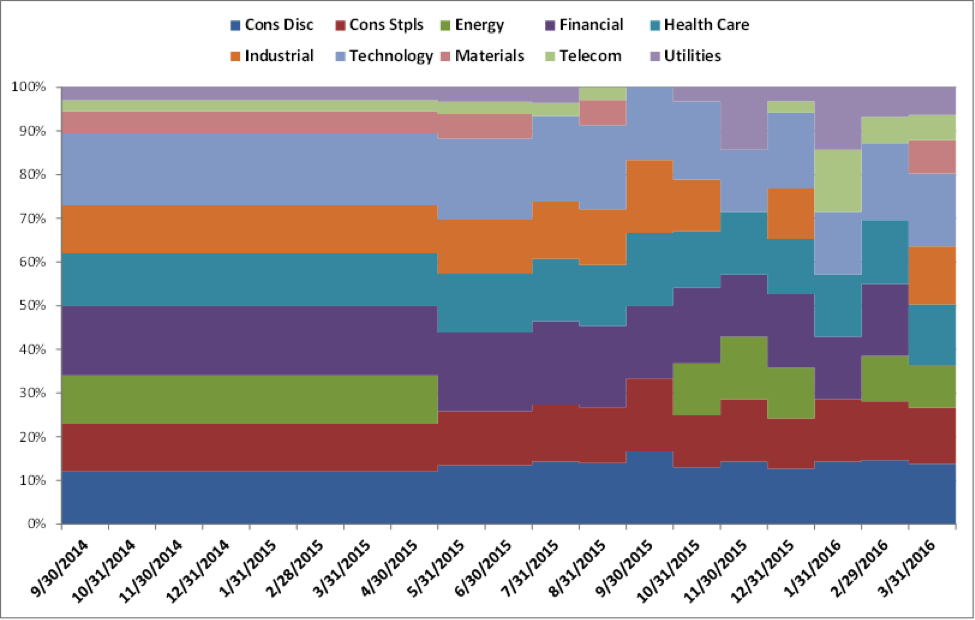

The risk management device that seeks to mitigate bear market risk is a sector-rotation strategy. We have our own momentum algorithms that tell us when it is advisable to get out of certain industry sectors. By sector, I mean the classic 10 industry sectors that make up the S&P 500 – healthcare, financials, consumer staples, technology, etc. That algorithm helps us determine when sectors ought to be exited. It’s not a predictive tool; it doesn’t try to predict turning points in the sectors. It just tries to identify a sustainable downward trend early in its development and then get out of its way. We found it is a very effective and reliable way to manage an equity portfolio against a typical bear market.

It’s usually one or a small number of industry sectors that leads the market decline. For example, in 2000 it was technology and in 2008 it was financials. In some cases, the decline drags other sectors along, but it is very much a sector-by-sector phenomenon.

If you can exit the misbehaving sectors and stay invested in the still-healthy sectors, that can be a very effective way to manage bear market risk. It is not designed to outperform the market when the market is doing just fine on its own. It is designed as a risk management device that seeks to avoid significant downturns in your equity investments during a traditional bear market.

Right now we happen to be invested in all 10 sectors.

[Below is an illustration of the sector allocations in The Giralda Fund and the Giralda Risk-Managed Growth Fund at each month-end since 10/31/14.]

Can you describe how you hedge against the second type of risk – that of a sudden decline?

Not all declines are as well behaved as the typical bear market. The typical bear market takes a while to develop. It announces itself. It stays around for a while, and it allows a momentum-based strategy to respond. But there are some market declines that aren’t as well behaved, come out of nowhere and fall dramatically off the table like 2008. They develop so fast that a momentum strategy doesn’t have time to react. In our view, you need to supplement that risk management device with something else: a hedge that will respond almost instantaneously. To address that, we have a suite of tail risk hedges that are designed to appreciate dramatically when equity markets have these sudden drawdowns.

We implement this hedge with derivatives. Essentially what we are trying to do is be long volatility – that is, invest in volatility – and capture and monetize the sudden spike in volatility that typically accompanies a sudden drawdown in equities. You can think of it like a put option, but it is much more cost-effective.

That’s the trick in these tail-risk hedges, because there is no shortage of them in the market. The goal is to find one that’s not going to bleed you to death while you hold it during periods when in retrospect you really didn’t need it. It’s very easy to lose a lot of money holding hedges. We have developed a very cost-effective way to do that, so you hedge when you need it but you don’t have huge carrying costs in the meantime.

Our combination of bear-market and market-crash risk-management devices is quite unique.

As you say, a risk-managed strategy must have some costs. How low does the performance drag need to be for the risk management to be worth it?

We did some quantitative analysis to answer that question. We looked at the S&P 500 over the last 80 years or so. With that data, we asked if you had protection of a certain degree how much drag could you afford to live with during periods when you didn’t need the protection. [Here is a link to that analysis.]

First, you’ve got to describe the protection. We thought a useful way that would cover just about any kind of solution was to think of it in terms of a co-pay and a deductible, like major-medical insurance. The deductible is how far down the market needs to go before the protection kicks in. You don’t want to protect against every dollar of every shallow decline in the market. That’s not cost-effective.

The co-pay is how much of any subsequent decline beyond the deductible you are protected from. For example, if you had protection that kicked in after a market correction, which is typically defined as a 10% drawdown, that is your deductible. If your protection insulates you from not all of the subsequent decline, say only 75% of it, then based on that 80-year history it turns out that you can have a performance drag during bull markets of 600 basis points – six full percentage points a year. If for the same 10% deductible, the solution you are interested in provides 50%, instead of 75%, protection against any subsequent decline, then you could absorb a cost of 410 basis points, or 4.1%, per year of a performance drag during a bull market.

Those are pretty high numbers. When we did the analysis, we were surprised how high those tolerable costs were, but it makes sense actually when you think about it. This is the way the math of positive and negative returns work. If you lose 20%, you’ve got to gain 25% to get back to where you started. So, avoiding a decline is the economic equivalent of achieving a gain of even greater percentage magnitude.

What is the level of protection that you target now in your funds, expressed in terms of a deductible and a copayment?

As you know, since we launched in 2011 we haven’t had a market decline of any real substance. We’ve danced around the correction level of 10%, but hasn’t gone any further than that. It is our view that you don’t want to spend time and effort and expense protecting against routine market corrections of 10% or shallower. That’s not a good use of resources. Those 10% declines are very easy to recover from. You want to protect against declines worse than that. So our strategy is designed to start providing protection beyond that point.

With respect to the copay, as I’ve said, we haven’t had a market decline beyond our 10% drawdown deductible since we’ve launched, so we cannot definitively calibrate the copay percentage yet. But we have modeled our strategy over prior periods that did include deeper market drawdowns and we believe that a copay percentage of 50% to 75% is a very conservative estimate.

So, the combination of a 10% deductible and a 50% to 75% copay would imply that our strategies could still be cost-effective even if they had a cost in terms of performance drag of approximately 500 basis points, or 5%, per year.

The Giralda Fund has returned 6.7% since its inception in July 2011, outperforming the Morningstar Long/Short Equity benchmark, which returned 2.6% over that period, but underperforming the S&P 500, which returned 12.2%. The Giralda Risk-Managed Growth Fund has returned 3.1% since its inception in May 2014, versus -1.2% for the Morningstar Long/Short Equity benchmark and 6.4% for the S&P 500. Those numbers are as of March 31, 2016. What is the appropriate way to assess the performance of your funds and has that performance been in line with what you expected?

The way to view performance for a strategy like ours is against other strategies that are trying to do the same thing. In Morningstar’s world, that is its long-short peer group. Against that peer group we are a top-tier fund. We are currently in the top 4% of funds in that category over the last three years. There are over 150 funds in that category. That’s the substance of the five-star rating that Morningstar has given us. Against other funds that are trying to do the same thing, we are a very, very solid performer.

If you are going to compare our funds against a non-risk-managed benchmark, like the S&P 500, then that’s got to reflect the cost of providing downside-risk management. What’s a fair magnitude for that cost? That is the analysis I just went through. For a strategy like ours, the historical analysis would say that a performance drag of about 5% or more a year would be tolerable. Well, we want to be well below that and, over the last three years, we’ve actually been running between 0% to 3% a year in performance drag against the average of the S&P 500 and the Dow Jones Industrial Average, the two primary non-risk-managed benchmarks that people use. In my view, that is exceptional performance given all the risk management that we provide. It is well within the 5% of tolerable cost.

What have been the challenges of running a risk-managed equity strategy during an extended bull market?

Timing is everything, isn’t it? We launched in the summer of 2011, and ever since we’ve been in bull-market mode. We are now in year eight of this bull market which is very long in the tooth by historical standards. That is a challenge for a risk-managed strategy. In retrospect, clients would have had a better return if they were just in the market Index funds.

But, given our client’s state of mind when we launched, many of them would not have been in equities to the extent they were able because we provided this strategy to them.

Having said that, it’s true that for any risk management strategy the nightmare scenario is to have a long extended period of time after you launch when the market doesn’t need any risk management. That’s exactly the market we have faced. It’s been a challenge to growth because investors have short memories. It may take another market crash or extended bear market for investors to be pounding the table and demanding a risk-management strategy again.

But we’re not sitting here rooting for a bear market. We prefer the market to keep going up. But I know it won’t always go up.

I have a significant portion of my family’s nest egg in this strategy because I want to be in equities but I fear the next inevitable downturn.

Some of your recent writings have asked the question: Is 80/20 the new 60/40? What do you mean by that?

What it is the single most important thing a typical investor needs in his/her portfolio? I would argue that it’s equities. That is the growth engine. That’s the thing that’s going to keep you ahead of inflation over the long term — and inflation is your biggest financial risk. The one essential component of any portfolio is equities.

Why shouldn’t that be the only component, then? Well, equities have downside risk. They tend to go down when you least expect them to — and sometimes dramatically. There is no free lunch. You can’t have equities without downside risk.

What’s the traditional way of managing that downside risk of equities? It’s diversification into bonds, real estate, commodities or other alternatives. The traditional diversified portfolio has been called the 60/40 portfolio – 60% in equities, 40% in other things, predominantly fixed income but also other alternatives.

Today, we are faced with some pretty grim prospects for that 40%. With respect to bonds, interest rates are at historic lows. We believe, they have nowhere to go but up, which means the market value of bonds have nowhere to go but down. We are looking at a long protracted bear market in bonds, and most of what we have seen over the last 30 years has been a robust bull market in bonds. It’s just not smart to expect the 40% to behave and perform as it has over the last 30 years. Those 30 years span the professional careers of most wealth advisors. They are facing a new world, and that 40% is not going to perform like it has over the last 30 years.

At the same time, the returns for alternatives have generally become mediocre. What’s even worse is that they are starting to behave more like equities, so they are not providing the kind of portfolio diversification that made them attractive in the first place.

Things are not looking good for the 40%, however you allocate among bonds and alternatives.

So, let’s get back to basics. Why do we have the 40% in the first place? It’s to buffer the downside risk of the one essential component of the portfolio, equities. If there were a way to buffer that risk more directly and more reliably, then it would lessen the need to rely on the 40% to do that. Therefore, if you replaced a healthy chunk of your equity investments with their risk-managed counterparts, then the equivalent of a 60/40 portfolio would be 80/20, where 80% was invested perhaps not entirely but in good part in risk-managed equities, which will allow you to reduce the 40% to 20%. In my opinion, you then end up with a safer portfolio that is more likely to keep you ahead of inflation over the long run. That is where the “80/20 is the new 60/40” idea comes from.

How have advisors been using your funds?

Advisors have used it in one of three ways. One is as a core equity holding, replacing some of their long-only equities with risk-managed equities. In most cases, depending on how aggressive or conservative the client is, that allocation has been anywhere from 15% to 40% of the portfolio.

Other advisors have used it as a liquid alt because they see an attractive alt as something that has, say, two-thirds of an equity return but half the volatility. They look at our risk-managed equity strategy as something that gives them more like 90% of an equity return and the volatility that’s “missing” is the bad volatility; it’s the downside. They see it as a category killer among liquid alts and have replaced some of their other alts with this strategy. In that case, the allocation has been more like 5% to 15%.

The third category, which is not as popular as the first two, is to use it for their children’s accounts as a replacement for an allocation fund. Where they would typically put their kids’ money in a 60/40 allocation fund, instead they would put it entirely in a strategy like ours. Kids have a very long investment horizon. They want them to be in equities, but they think this strategy has more long-term appeal than a 60/40 strategy for a lot of the reasons I mentioned a few minutes ago

Many advisors are fearful of a bear market in equities, based on analysis such as the historically high Shiller PE ratio. Similarly, many are fearful of rising interest rates. How do you respond to those concerns in the context of your strategies?

With respect to the fear of rising interest rates, it’s got to be more than a fear, it’s almost a certainty. It’s just a matter of how fast and how soon. I think I addressed that pretty fully earlier. So, let me address the high equity valuations.

That’s a rational fear that equities appear rich by historical standards – not exorbitantly overpriced, not a case of irrational exuberance, but rich. In the wake of the 2008-2009 meltdown, this bull market is now in its eighth year. People are nervously waiting for the next bear market. We know it’s going to occur; it is just a matter of when and how bad it is going to be. That is a rational fear.

But you can’t desert equities waiting for that to happen. That is a losing strategy.

You just don’t know when it’s going to happen. If, for example, you had anticipated that the bear market would’ve been on its normal schedule and happening once every four years or so, you would have been out of the market the last three or four years and missed out on appreciation of 50% or more. The rational way to respond to high valuations and an impending bear market of uncertain timing is to be in equities, but to be very diligent about managing the downside risk. That is exactly what led us to develop the strategy we did.

This material is for informational purposes only. Nothing in this material is intended to constitute legal, tax, or investment advice. Investing involves risk including potential loss of principal. There can be no assurance that any views, outlooks, projections or forward-looking statements will come to pass. All statements and opinions are subject to change as economic and market conditions dictate.

Giralda Advisors, located in New York City, is an asset management firm that focuses on providing risk-managed exposure to the equity markets with a goal of limiting asset depreciation during both protracted and catastrophic market downturns while allowing substantial asset appreciation in up-trending markets. The Giralda Advisors team welcomes your inquiries. Please call (212) 235-6801 or visit us at http://www.giraldaadvisors.com/.

Read more articles by Robert Huebscher