In today’s low-interest-rate environment, advisors must add value to fixed-income allocations. Unfortunately, some of the higher yielding segments of the fixed-income markets – such as peer-to-peer (P2P) investing – don’t fit into the typical financial advisor investment platforms.

But that may soon change, as NSR Invest, a P2P analytics and management solution, prepares to launch the first integration of P2P investment platform Lending Club to Orion Advisor Services, a traditional portfolio analytics solution. The ultimate goal is to make it feasible for financial advisors to manage client investments in P2P loans, including allocating capital into individual loans (in a diversified manner), managing cash flows in and out of P2P investment accounts and consolidating performance reporting of P2P investing with the client’s other portfolio investments. Advisors can even bill for their services.

Of course, the caveat is that P2P investing still has significant risks that accompany its higher yields, from a material risk of default (which can only be partially diversified away) to significant illiquidity. Nonetheless, the demand from yield-starved clients and NSR Invest’s technology may finally make it feasible for, at least, independent RIAs to allocate client dollars to P2P investment opportunities!

The problem with P2PP2P investing (for advisors)

Most financial advisors are restricted to mutual funds and ETFs that can be traded on a custodial platform, purchasing market-traded securities like stocks or bonds directly, or for those with a broker-dealer relationship “selling” other alternative forms of registered securities (e.g., non-traded REITs). Investments that aren’t available to advisors under traditional broker-dealer or custodial relationships typically aren’t made available to their clients either.

Accordingly, when it comes to investment opportunities like P2P lending (or rather, P2P investing as a prospective lender), advisors have had little to no exposure to the marketplace, despite its arguably rather appealing fixed-income returns (albeit with significantly more risk and potential volatility).

Technically, an advisor has long been able to encourage clients to open an account directly with P2P investing platforms like Prosper or Lending Club, but helping clients invest there is tedious at best. The importance of extensive diversification (given that even the highest quality individual loans still have a material risk of default) is crucial, but manually allocating investments across a wide range of P2P loans is time consuming. Automated tools from the platforms (e.g., Lending Club’s Automate Investing, and Prosper’s Automated Quick Investment [AQI] solution) that help diversify P2P loans help, but the relatively simple automation algorithms may not be best for deploying client assets. Of course, an advisor just having clients’ login names and password credentials to do this on their behalf could trigger the SEC custody rule for advisors as well.

Even if these dynamics are navigated, it has still been difficult for advisors to help manage the overall process for clients. Client account balances at P2P lending platforms generally don’t aggregate into traditional advisor portfolio accounting and reporting tools, making it difficult for advisors to actually “manage” and report on the assets as part of the total portfolio. And if it’s impossible to effectively report on the assets, it’s also daunting to capture the information necessary to bill on them, even if the advisor is helping to manage them.

In other words, even if advisors wanted to allocate client assets towards P2P investing strategies to pursue higher yields than other fixed-income alternatives, the available technology solutions have made it impossible to do so.

But that is about to change.

NSR Invest rolls out platform for advisors

To plug the technology gap, NSR Invest is building the first integrations to connect P2P lending platforms like Prosper and Lending Club directly into advisor technology tools.

For those who aren’t familiar, NSR Invest was created earlier this year from the merger of two separate platforms – a site called Nickel SteamRoller (now NSR Platform) that was one of the first online resources to analyze the loan history of Lending Club and later Prosper, and a second site called Lend Academy Investments that packaged together some of the early versions of separately managed accounts and pooled funds for investing in P2P loans. NSR Invest’s goal is to offer a wider range of full-service managed accounts for P2P investors, expand the pooled investment funds for accredited investors allocating dollars into P2P loans, and build out an order-management and reporting platform for institutional investors.

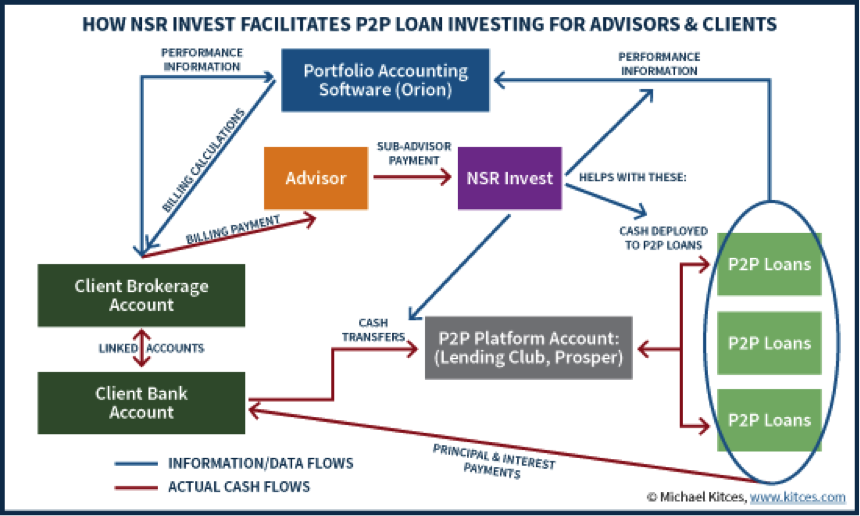

The latter development has relevance for advisors. As a part of its institutional platform development, NSR Invest is building its first integration directly into advisor portfolio accounting software tools, starting with Orion Advisor Services.

Once the integration is completed (anticipated rollout is in December), Orion will be able to pull in transaction-level P2P loan investment data directly from a client’s Lending Club account (a connection to Prosper accounts is planned for a future release). This makes it feasible to include P2P investments in the client’s consolidated balance sheet and calculate aggregate performance (including P2P loans). Advisors can bill for their advisory support related to the client’s fixed-income allocation to P2P investments.

Using the NSR Invest platform to manage P2P strategies

The integration between NSR Invest and Orion will allow for the reporting on a client’s P2P investment holdings, and manage those investments through the NSR Platform.

Creating custom P2P algorithmic investment strategies

As noted, Nickel Steamroller originated as a platform that could pull in historical loan performance data for Lending Club (and later Prosper), to run historical analyses of performance with any number of filters (e.g., to review the results of all loans of investment grade B or better that were income verified, with a five-year term, created in 2010 or 2011, and were used for the purpose for debt consolidation). This made it feasible to back-test P2P investing strategies based on historical data.

Advisors can use the NSR Invest platform to create their own P2P loan allocation strategies. For instance, say an advisor prefers to only fund loans of A-quality or better, with a three-year term, being used for debt consolidation by those who are income-verified and who have at least five years of employment history, while allocating no more than $200 into any particular loan. NSR Invest can facilitate this process and invest directly with Lending Club (and soon, Prosper).

For instance, if the advisor wishes to allocate $40,000 of the client’s assets into 200 different loans that meet certain criteria, NSR Invest can transfer the funds with Lending Club directly from the client’s authorized bank account – and then allocate into the desired loans as new borrowers who fit the criteria come to the platform to request funding. This is the whole function of P2P lending platforms in the first place: matching borrowers to investors.

Alternatively, advisors can use NSR Invest’s own P2P investment strategies – aptly dubbed “conservative, balanced, and assertive” – which currently target net returns (after default/write-downs) of 5%, 7%, and 10%, respectively. By following this path, client assets are allocated into P2P loans based on NSR’s expertise, rather than the advisor determining the loan-implementation strategy.

Costs for using NSR Invest to manage P2P loans

The NSR Invest platform costs 45bps per year, which is billed quarterly in arrears based on the client’s average daily balance in the P2P investment account.

The arrangement is formally structured with NSR Invest as a sub-advisor to the investment adviser’s own client relationship, which technically means the advisor is responsible for collecting the investment management fee and remitting it to NSR Invest. In practice, this means the advisor can either bill the client’s other investment accounts and remit the amount to NSR Invest, or it can be swept directly from P2P investment payouts of principal and interest as they occur. NSR Invest has been working on additional enhancements to allow its fees for supporting the P2P investing process to be swept directly from the P2P account at Lending Club.

For advisors who use NSR Invest’s proprietary P2P investment strategies, rather than create their own algorithms, the fee increases from 45bps to 60bps. The advisor still determines how much of the client’s cash/assets to deploy to the P2P platform and facilitates the transfer, and then effectively hires NSR Invest as the subadvisor (and the client will literally sign a sub-advisor agreement with NSR) to allocate into P2P loans.

The advisor may still charge his or her own fee for making the decision about whether and how much to allocate to the P2P investment strategy, and pass through the NSR costs, in a similar manner to any other outsourced/third-party investment manager or subadvisor (where the advisor charges a wrap fee, and then the client pays the underlying mutual fund manager’s expense ratio or a separately managed account fee). Of course, with the significantly higher yield in P2P loans compared to most other fixed-income investments, there may be less fee pressure on the arrangement.

Automating cash movement between brokerage and P2P platforms

NSR’s latest development was to more fully automate the cash movements between a client’s other investment accounts and the available Lending Club and Prosper P2P platforms. This would allow advisors to more dynamically rebalance and adjust allocations in P2P and brokerage accounts.

In fact, while the original NSR Invest process only automated pulling client cash from a bank account with ACH capabilities to facilitate the transfer (which is not how most brokerage accounts are structured), their latest iteration now permits transfers to occur directly from brokerage accounts to a related P2P account. While the connections still have to be authorized by clients to permit transfers initially (a manual step), this should further facilitate the process of managing client households across “traditional” brokerage and P2P accounts (at least to/from Lending Club, which can facilitate this thanks to their more robust APIs than competing provider Prosper).

On the other hand, it appears that while P2P investing accounts can handle retirement assets –the high yield of P2P loans make them an especially appealing fixed-income investment to hold within a tax-deferred retirement account – at this point the process of transferring money from one retirement account (e.g., at an IRA custodian) to another retirement account (at the P2P platform) requires paperwork with client signatures. Ultimately, NSR Invest hopes to automate more of these cash transfers. Nonetheless, NSR Invest can handle the performance reporting and deploy cash into P2P loans, once the funds have been transferred into the proper IRA.

Will NSR Invest open a new P2P alternative fixed-income asset sub-class?

Today’s low-return environment has put increased pressure on advisors to justify their investment management fees, especially for low-yielding fixed-income investments. This has spawned everything from controversial hybridized fee structures (with “discounted” investment management fees for the cash and fixed income portion of the portfolio compared to the equity portion), to the rapid growth of many “alternative” asset classes serving as fixed-income substitutes.

P2P loans represent an opportunity to add value and diversify into a new subset of the fixed-income category itself, one with far more appealing yields and the potential for higher total returns. Of course, the caveat to investing in P2P loans is that even the highest quality loans still have a material default risk, and the default rate will only rise further if/when the next recession occurs (P2P loans from the 2008-2009 period barely ended out with positive total returns). In addition, the loans are illiquid and difficult to sell if clients need to raise cash. Fortunately their relatively short three- to five-year maturities and the fact that only a limited portion of fixed-income assets would be allocated to the asset class mitigates the impact. And the rise of a secondary market for P2P loans, currently through a FolioFN note platform, also provides at least some liquidity (though realistically, in a significant market sell-off, the available bids for P2P loans in the Folio marketplace may not be at a price a seller wants to accept, as the market is still very thinly traded).

The starting point for NSR Invest is to integrate just with the Orion Advisor Services platform – due out sometime in December – so advisors not using Orion will have to wait until NSR expands its integrations to other portfolio-accounting solutions. Or alternatively, advisors could use the NSR Invest platform directly to manage P2P investing for clients (or have NSR Invest manage it using their proprietary strategies), but as an externally managed account that isn’t reported alongside the client’s other investments in an automated manner.

On the plus side, since the solution is being driven through the portfolio accounting software, NSR Invest will be “custodian agnostic.” It won’t matter whether the RIA custodies the rest of a client’s assets at Schwab, Fidelity, TD Ameritrade or elsewhere. (Though ultimately the funds will leave the custodian to go to the P2P platform, and the process of trying to automate cash transfers to fund P2P platform accounts may vary depending on the custodian.) Advisors will “just” need to enroll in the NSR Invest platform, activate the Orion integration, have clients sign a sub-advisor agreement with NSR Invest and update their Form ADV to reflect the sub-advisor relationship.

The Orion integration means that, for the time being, NSR Invest’s offering will only be available to independent RIAs. Advisors who work at a broker-dealer would need NSR to go through the broker-dealer’s application/approval process to become an outside manager, which NSR Invest isn’t pursuing at this time (and even then, Orion is generally not used by captive advisors at a broker-dealer). Whether NSR Invest ultimately expands to work with independent broker-dealers remains to be seen.

Nonetheless, given the ongoing growth of independent RIAs, the new availability of the NSR Invest platform opens up a new fixed-income asset class to a subset of advisors, in a manner that has some additional cost but is much less expensive than most of the third-party managers that offer P2P investment solutions for clients.

It remains to be seen whether the NSR Invest solution will execute P2P investing as efficiently as advisors hope. While NSR Invest won the “Most Promising Prototype” award at the Fuse Hackathon earlier this year, the integrations are just now being completed. For advisors who are looking to add more variety to client fixed-income allocations, and the potential for some higher returns (albeit with greater risks), NSR Invest is worth a look.

Michael Kitces is a Partner and the Director of Research for Pinnacle Advisory Group, co-founder of the XY Planning Network, and publisher of the financial planning industry blog Nerd’s Eye View. You can follow him on Twitter at @MichaelKitces.

Read more articles by Michael Kitces