The Flaws in the Dollar Indices

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAccording to the most widely recognized data series, the value of the dollar has declined by approximately 20% over the last half century. Critics of federal policy claim this is proof of systematic “dollar debasement,” engineered through quantitative easing and the Fed’s mandate to maintain a baseline level of inflation. But that data series is incomplete, and once it is corrected, the 20% decline shrinks considerably.

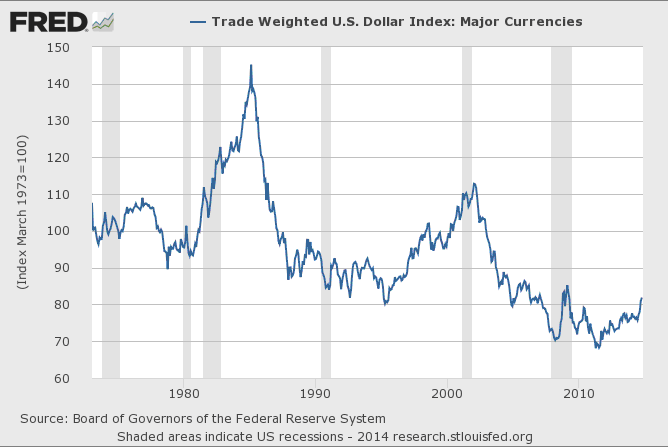

The flawed data series is the trade-weighted U.S. dollar index, which is maintained by the St. Louis Fed. It is shown below. Its construction is also the basis for the Intercontinental Exchange’s (ICE’s) dollar index, commonly known as the Dixie, which is traded in the commodities market.

The Dixie recently had a record 12-weeks of consecutive gains. But do the Dixie’s four-year highs actually mean anything for the dollars in your wallet? Moreover, what do moves like this mean for the dollar’s value in the global economy?

To answer these questions, I will look at how the Dixie and other dollar indices are constructed, highlighting their flaws and omissions. I will then show how Advisor Perspectives constructed its own dollar index and what that index says about the true value of the dollar.

Dissecting the Dixie

The Dixie is an investment tool licensed by the ICE for commercial purposes. It captures the value of the dollar against tradable currencies that fluctuate in the market, providing an index that serves the needs of traders and speculators.

But the Dixie doesn’t tell the average American everything about the value of the greenbacks in their wallet. It doesn’t measure how much a dollar can buy of imported goods and services, and it doesn’t measure the dollar value of exported goods and services.

The Dixie is not an adequate benchmark for the value of the dollar. It excludes major trading partners like China, Mexico and Saudi Arabia. It fails to account for important elements of U.S. trade like oil imports and gold and military exports. Finally, the Dixie isn’t structured to capture changes in global trade because it has no regularly scheduled adjustments or rebalancings and assigns fixed weights to countries.

So, should you really pay attention to the pundits that have been obsessing over the Dixie’s moves lately? The Dixie is relevant to investors who just want a general dollar benchmark for their daily trades in financial markets. But you should be skeptical of pundits who treat the Dixie as an economic indicator.

Existing dollar indices

Recognizing that the Dixie has many imperfections, many firms have created dollar indices. However, they are all designed to be trading instruments, and none have succeeded in providing an accurate economic measure of the value of the dollar.

The Dow Jones CME FX$INDEX was introduced in 2010 as a tool for investors looking to manage risk. It is marketed as an index that reflects more recent economic developments, as opposed to the Dixie whose composition has only changed once since it was first created in the 1970s. But the Dow Jones CME index uses fixed currency weights, and excludes major trading partners including Korea, Mexico and China. Because of its design, this index doesn’t truly capture changes in world trade.

Most indices exclude China and other countries whose currencies are pegged to the dollar. Because their exchange rate relative to the dollar is fixed, their inclusion would suppress the volatility of the index, making it less interesting for traders.

The Dixie and all other indices are adjusted for inflation and represent the real value of currencies in their domestic economies.

In 2012, the Wall Street Journal announced that it was introducing the WSJ Dollar Index (BUXX) to provide a more precise measure of the value of the U.S. dollar. This index uses a more comprehensive weighting scheme than the Dixie. However, it has some serious limitations. It is based on data from the Bank of International Settlements that is only released once every three years. Also, it excludes currencies from important economies like China, Korea and Mexico.

The FTSE Group and the Cürex Group teamed up in 2012 to launch an index in the hopes of rivaling the Dixie. Recognizing the importance of China as a trading partner, they introduced the FTSE Cürex USD/G8 Index to measure the performance of the U.S. dollar against seven developed market currencies and the Chinese renminbi. However, this index gives equal weightings to the currencies in its basket and excludes Mexico and South Korea.

Hoping to correct the shortcomings of existing dollar indices, the Bloomberg U.S. Dollar Index (BBDXY) was created in 2013. According to Bloomberg, this index “provides a better measure of the U.S. dollar as compared with other indexes that do not update their composition and are comprised of a handful of currencies with concentrated weights.” This index is rebalanced annually and is more diversified since it includes emerging-market currencies from China, Korea and Mexico. It is a good trading instrument, but it has some flaws. The BBDXY includes the Chinese renminbi but caps the weight of this major trading partner at 3%. It also does not reflect U.S. trade with Hong Kong and Saudi Arabia.

All these indices have one thing in common; they were created to be commercial trading instruments. They serve the needs of one constituency – traders and speculators. They provide incomplete measures of the value of the U.S. dollar because they don’t accurately reflect changes in global trade.

The Advisor Perspectives U.S. dollar trade-weighted index

We created an index with the objective of providing an accurate benchmark for the value of the dollar. Our index is designed for informational purposes. Unlike other indices, we did not design and develop it with the objective of creating a commercial trading instrument. We successfully addressed the shortcomings of the Dixie and other indices of its kind.

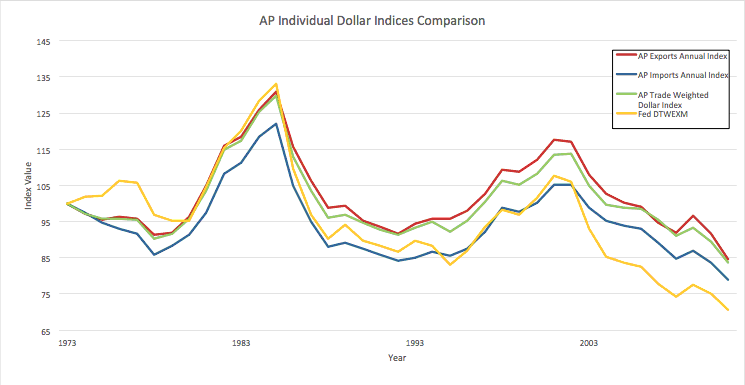

The Advisor Perspectives U.S. dollar trade-weighted index integrates time-varying weights to consistently capture approximately 75% of total U.S. trade. The index is rebalanced annually, and it includes currencies from the following countries: Brazil, Canada, China, the Euro area, Japan, South Korea, Mexico, Saudi Arabia, Singapore, Taiwan and Venezuela.

The weights assigned to the economies in our index are derived from annual import and export flows. They reflect each country’s importance as a trading partner during that given year. One of the most prominent criticisms of the Dixie is that it heavily weighs the euro; it represents 57.6% of that index. We corrected for this; in our index, the euro never represents more than 35% of the index, which more accurately reflects U.S. trade with the European Union.

Advisor Perspectives’ index is derived from a comprehensive dataset that includes oil imports, and gold and military exports. Many commercial indices exclude these goods because they are undifferentiated. Undifferentiated goods are excluded because economists don’t want to measure the role of exchange rates in the trade of what are essentially commodities (especially those like oil, which are priced in dollars). However, they represent a significant portion of U.S. trade and are important in accurately calculating the value of the dollar.

Our index is shown above with the St. Louis Fed's trade weighted index, which is the basis used to create most commercial indices, particularly the Dixie.

We also created separate import- and export-weighted dollar indices to illustrate the strength of the dollar in two distinct sectors of the economy. The Dixie, by contrast, is a combination of imports and exports. Imports measure the value of the dollar primarily as it impacts the purchasing power of U.S. consumers. Exports measure the value of the dollar primarily as it impacts corporations, mostly manufacturers of tradable goods. Therefore, we created two sub-indices, one weighted by imports and the other by exports. The composition of these sub-indices is rebalanced every 3-5 years and the weights are updated annually.

The Advisor Perspectives indices were calculated using a methodology very similar to that of the Dixie. Our indices are calculated using geometrically weighted averages of bilateral exchange rates. The weights capture each country’s importance in terms of trade competition, and the real value of exchange rates is calculated using respective CPIs. Our indices aggregate and summarize the effects of dollar appreciation and depreciation on the competitiveness of U.S. products in relation to major U.S. trading partners.

Conclusion

The Dixie and other indices were constructed for commercial reasons to serve the needs of traders and speculators. Our index was constructed purely for academic reasons, to illustrate the value of the dollar more accurately in the context of global trade.

A key finding is that the value of the dollar has declined less over the last half century than what the Dixie and other indices show. This is consistent with economic theory. Since the dollar has been the world’s reserve currency over this period, there has been a structural demand for it among our trading partners. Those countries must own dollars to trade with the U.S. As a result, there is systemic upward pressure on the value of the dollar.

Another interesting result is that the Advisor Perspectives export-weighted index shows a more aggressive strengthening of the U.S. dollar than the import-weighted index. This is partially because some of our key import trading partners (like China and Saudi Arabia) are pegged to the dollar. When the U.S. imports from one of these countries, the demand for products in that foreign country does not lead to an increase in the value of that country’s currency. In contrast, when a foreigner exchanges their domestic currency for U.S. dollars to buy U.S. exports, they increase the demand for the dollar and decrease the demand for their domestic currency.

The indices created by Advisor Perspectives are comprehensive measures of the U.S. dollar and serve as useful tools in analyzing overall levels of economic activity.

Marianne Brunet is an associate editor with Advisor Perspectives.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All