Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Recent volatility in the stock market will not evolve into a serious decline, because credit spreads in the bond market remain low and stable.

The yield premium that investors demand for holding sub-investment-grade “junk” bonds relative to U.S. Treasury bonds is an objective measure of the overall risk climate in the markets. Historically, when the spread between these two credit-market benchmarks has been low and stable, asset markets have been stable too. However, when the yield spread between junk and Treasury bonds spikes higher, trouble follows.

Despite the drop in U.S. stocks in January and a much deeper dive in emerging markets for more than a year now, domestic credit spreads have remained low and stable. Unless this changes, investors would be wise to buy stocks rather than flee to less-risky assets.

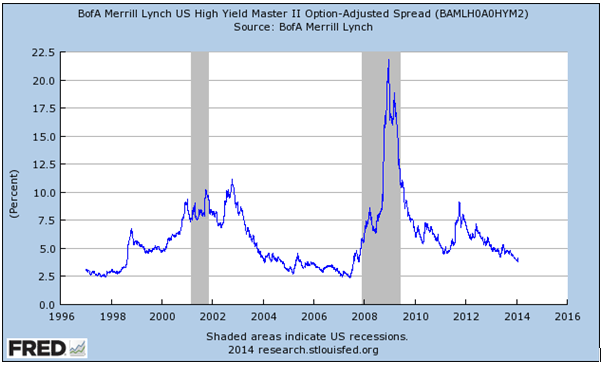

The chart below tracks the daily yield spread between a widely followed junk bond index and the 10-year U.S. Treasury. The median spread over this 17-year time period was 5.34%, while three-quarters of all observations reflect a spread below 7.25%. Credit spreads rose immediately before and during the two recessions included in the chart, as indicated by the shaded areas.

Other periods of rising credit spreads coincided with memorable moments in market history. The spike in 1998 reflected investor nervousness associated with the “Asian Contagion” that triggered the notorious collapse of the hedge fund Long Term Capital Management in the fall of that year. Gyrations in the credit spread between 2010 and 2012 coincided with the unfolding of the euro-zone debt crisis, growing political dysfunction in Washington and the first-ever downgrade of America’s triple-A credit rating in the summer of 2011.

The final data point on the chart above is from Jan. 30, 2014, when the credit spread was 4.12%, unchanged from December and lower than two-thirds of all observations since 1996. Until weakness in the stock market is confirmed by signs of stress in the credit markets, odds are good that the recent downturn in the stock market will pass without harm.

A fundamental explanation underlies the relationship between credit spreads and the behavior of other risk markets. Credit spreads measure the collective opinion of untold well-informed, financially incentivized participants in an ongoing conversation about risk.

According to the U.S. Bureau of Labor Statistics, the domestic economy includes 296,900 people employed in the profession of “loan officer” and another 61,240 in the category of “credit analyst.” The livelihood for this 350,000-strong army of professionals depends on their ability to lend real money to borrowers who pay it back. To be successful, creditors must stay in touch with the people who owe them money. As a consequence, the dialogue among participants in the credit markets is deliberate, thorough and continuous. Conversations are happening every day, in every city.

When creditors don’t like what they’re hearing, it shows up as a rising spread between the yields of junk bonds versus Treasurys. When the tone of these conversations suggests business as usual, credit spreads behave normally as well. Right now, creditors aren’t worried.

The BLS estimates there are 16,900 people in America employed as “economists.” Some of these economists think the recent decline in the stock market is a signal of more to come. Take your pick who to listen to first.

Keith Goddard is the CEO and Chief Investment Officer of Capital Advisors, Inc.