Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Because I majored in comparative literature, my education, while superb in the "getting me to think" department, left me woefully unprepared for becoming a money manager.

Not that I knew back then what I wanted to be when I grew up – I was only sure of two things I didn't want to be:

-

An academic. I didn't want to risk becoming a third-rate scholar of second-rate dead writers no one cared about. Having studied 18th century literature intensely since high school, I couldn't bear to devote even one more minute to the subject.

-

A lawyer. Like many clueless humanities majors, I took the LSATs and did quite well. Thankfully, a course in Constitutional Interpretation in the fall of my senior year – one which required the writing of a brief defending the forces of evil – convinced me that a career in litigation was out of the question.

Having ruled out two of the most obvious options for a liberal arts major, and in a desperate move during my last semester, I signed up for the one practical course available to me: Accounting.

In case you were expecting the triumphant discovery of my life's calling as a result of this class, I'm sorry to disappoint you; it didn't play out that way at all. My world-class cramming capabilities could not compensate for my spotty homework output. Concepts like T accounts and negative goodwill amortization need practice to sink in.

Although my first foray into applied knowledge was (way, way) less than stellar, it awakened in me a dormant interest in finance – there is a certain thrill in putting to immediate and practical use what one learns in class. And so for the next few years after graduation, I raced to acquire my technical education at night, taking all those classes in economics, accounting and finance that I had missed out on as an undergrad.

You might think that going to school at night after working all day would be a drag. For me though, it was a constant and vital reminder that theory and the real world often live on planets in different solar systems.

Case in point: A class devoted to modern portfolio theory, taught by a portfolio manager who worked at Goldman Sachs. He was nice and earnest, and he genuinely wanted to do right by his clients. And yet the most important lesson he taught me was that nice, smart people often believe in things that don't make sense.

One night he gleefully nattered on about portfolio insurance and how he'd "immunized his portfolio." You'd have thought he'd invented gravity, he was so ecstatic. This was in early 1987 and as I listened, I felt in my bones that somehow, to quote my Russian mother-in-law, "it would all end in tears." It just didn't make sense that portfolio insurance could be so frictionless in real life.

Sure enough, and as Voltaire's 18th century satirical masterpiece Candide foreshadowed for me during all those years of comparative lit, that neat and happy theory crashed head on into the messiness of real life in October of that same year.

Fast forward to today, nearly 25 years later, and I'm having another one of those existential investing angst moments, this time having to do with the explosive growth of Exchange Traded Funds (ETFs) and the havoc they're wreaking in small-cap land.

Every day, in the last half hour or so of trading, our small-cap benchmark, the Russell 2000, seems possessed by gremlins. No matter what's in your portfolio, it seems, you will lag ... whether the market goes up or down.

Now mind you, small-cap ETFs were designed to mimic the Russell 2000 but with advantages that mutual fund Index funds don't have, most notably being able to buy and sell at real-time market prices rather than end-of-day net asset values.

Trouble is, the creature that was created to shadow its master has become bigger than the Index itself. When the mimicker BECOMES the thing it mimics, which is the tail and which is the dog?

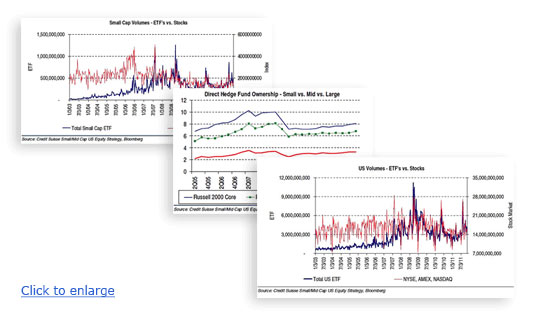

Consider the following ETF facts, kindly provided by Lori Calvasina, small-cap maven at Credit Suisse (see accompanying charts below):

-

ETFs represent anywhere from 30% to 40% of small-cap trading volume. This includes not just trading of the instruments themselves, but all the peripheral trading associated with the securities underpinning the ETFs as funds flow in and out of them.

-

By the time all ETFs, including sector funds, are counted, some small-cap companies have almost 20% of their shares held by ETFs. Additionally, trading volumes in single stocks have decreased as trading volumes in ETFs have increased. Clearly investors are caring less about differentiating among prospects for individual companies and more about sector or asset class exposure.

-

The bigger small caps (with market capitalizations over $1 billion) have more ETF ownership than the smaller cap companies, in part because they can be owned by large- and mid-cap ETFs as well. Yet the smaller small-caps are equally sensitive to moves in ETFs because they are so much less liquid. There is simply no place to hide from the impact of ETFs in small-cap land.

-

Moves in the Index are caused by fund flows into and out of ETFs. Demand for the "shadow Index" (ETFs) is causing movement in the Index itself.

What's it all mean? I don't yet have the answers. When it comes to questions, however, I see three big ones:

-

Will this trend create more valuation anomalies? In other words, if investors don't care that Secretariat can run 10 times faster than the average donkey, the valuation gap between the two will close as investors either pay too much for the donkey or too little for the thoroughbred.

-

Will all the volatility that comes from renting rather than investing in stocks turn off an entire generation of retail investors, thereby removing an important source of demand? After all, equities are subject to the same laws of supply and demand as tube socks.

-

Will company management and institutional investors, e.g., pension funds, foundations, be able to focus on their long-term objectives, or will they too suffer from mood swings and Attention Deficit Disorder? If so, God help us all.

At this point in our collective journey down the ETF path, it's much easier to uncover questions than answers; only time will tell when it comes to assessing the ultimate impact of this new elephant at the party. Let's just hope my mother-in-law's words aren't as appropriate this time as they were in 1987.

P.S. What do you think will be the impact of ETFs? How has it already affected your work or point of view? Let us know.

Striking ETF Graphs

Thanks to Lori Calvasina, Credit Suisse, for sharing the following three graphs regarding the growth of ETFs in recent years (click to enlarge graphs).

Mariko O. Gordon is founder, CEO and CIO of Daruma Asset Management, a NY-based small cap investment management firm. Subscribe to her free monthly e-newsletter On Daruma’s Watch here.

Read more articles by Mariko Gordon