Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

“The wages of sin are death. But by the time taxes are taken out, it’s just sort of a tired feeling.”

- Paula Poundstone

With the new Roth conversion rules about to be lifted next year and a “one-time special offer” available to allow investors to spread the tax bite of conversion over two years, more and more Roth conversion calculators are showing up every day. Be wary. If you use one of these calculators, don’t say I didn’t warn you about how misleading the results can be.

As with any program, the output is only as good as the input, and some of those inputs are the assumptions the program uses in the analysis. These assumptions about the future (which is of course uncertain) can wildly skew the answer to make the Roth look artificially attractive.

Misleading Roth analysis

I recently reviewed a paper about Roth conversions written by a large, respectable investment firm. The paper summarized key criteria of what would generally be the circumstances where a Roth conversion, or use of the Roth, would make sense.

Paraphrasing the paper, the “best candidates for conversion” are those who have taxable assets to pay for the conversion, and face ANY ONE of the following circumstances:

- Their tax rates in retirement are unlikely to be materially lower than pre-retirement rates.

- They are converting at a young age.

- They will not have a material income need from the IRA, they will only need withdrawals from the IRA much later in life, or they are using IRA assets to fund an estate goal (no need for withdrawals at all).

The paper proceeded to calculate all sorts of significant advantages for Roth conversions and showed only a few cases where a small, incremental benefit was offered by continuing to defer taxes by not converting. . Much of the supposed cause for the Roth advantage is based on required minimum distributions (RMDs) which, along with their tax effects, can be easily simulated.

I am highly skeptical of the Roth’s promise for a few reasons. First, I fear that a future government will change its mind and revoke the Roth’s tax-exempt status. Understand that Roth conversions (or contributions) increase current tax revenue at the expense of future revenue. In essence, the government is mortgaging future tax revenue to collect them now.

Roll forward thirty years and imagine the justification Congress might argue for in applying a surtax on all of these Roth multi-millionaires who don’t pay any taxes at all. It would be rather tempting for Congress to make a “needs-based amendment” to the tax-exempt status. While I wouldn’t plan on this happening, I would not assume there is no risk of it occurring either… especially for those using Roths to accumulate significant estate assets.

Secondly, the new Roth conversion rules are an option for anyone to execute at some date in the future, and with a highly uncertain future, basic option theory and common sense dictates that we should not pay additional tax now with certainty if we can avoid it, unless there is a clearly compelling advantage to doing so. In the future, this new Roth conversion option for high earners may be repealed, but I would not rush to pay a huge tax bite now if I can defer executing that option until some later date when some of the uncertainties of time have passed or a repeal of the option is imminent.

Finally, when analyzed properly, the supposed Roth advantage can actually be a detriment even where it is normally assumed to be advantageous, if an investor wants to be confident they can fund prioritized life goals and avoiding needless lifestyle sacrifice.

A case study of the problems posed by Roth conversions

Let’s do away with the erroneous assumptions that a Roth is usually advantageous for the young, when retirement tax rates are going to be as high as or higher than tax rates during earning years and when withdrawals won’t happen for many years. A scenario examining all three of these Roth-favorable conditions is simple to model.

Take a single 30-year old that earns $85,000 a year in moderately taxed Virginia. His combined federal and state marginal rate is 30.75%. He has nothing saved, but he knows he should start saving for retirement. He is considering whether to contribute to the Roth 401(k) his company offers or to a traditional 401(k) with a pre-tax contribution. He plans on retiring at age 65 on an after-tax spending budget of $60,000 a year adjusted for inflation, and he has no estate goals. The taxes on his retirement income will be at the same rate or higher if he funds the traditional 401(k) (depending on RMDs in each year of each simulation which we automatically calculate and tax). Trusting the promise of future Roth exempt status, he likewise is confident that Social Security will pay him his projected $23,464 annual benefit at retirement. To start saving for retirement, he determines that his lifestyle could afford a compromise to his current spending of $5,886 a year. This is what he could save after tax in the Roth 401(k). In the traditional 401(k), that same lifestyle compromise would make the pre-tax contribution $8,500 a year, because he would avoid paying current income taxes of $2,614 on his salary deferral. Both plans assume a balanced asset allocation due to his tolerance for risk and living to age 92, his 80th percentile life expectancy.

This example should be a poster child for the attractiveness of Roth. We have a young person deferring distributions for many years and taxes in retirement that are as high or higher than his current moderate tax rate. The Roth should show a no-brainer advantage, correct?

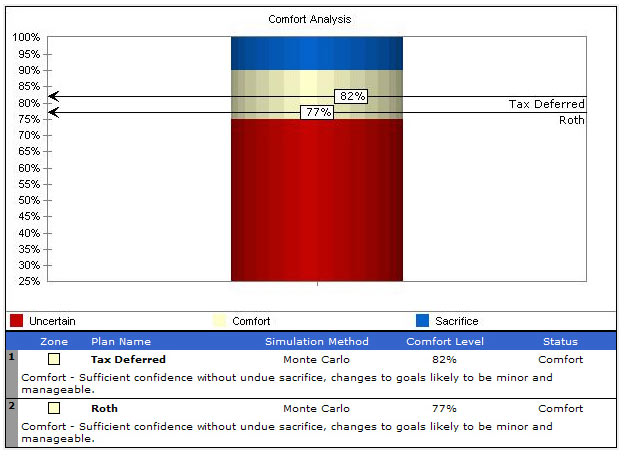

Well, Exhibit 1 demonstrates that the confidence level of exceeding his goals is HIGHER with the traditional 401(k) deferral than with the Roth. How could this be, when many other financial planning systems would show the Roth as the no-brainer choice for such a situation?

To answer this, I analyzed this case study with our Wealthcare platform. This allowed me to assess the impact of dynamic taxation, by calculating a unique tax rate to apply in each year of each simulation based on the spending goals, forced RMDs and one thousand 62-year simulations. While the paper focused on the median result (the 50th percentile), in Wealthcare we measure confidence in what we call “the comfort zone,” which is the 75th to 90th percentile confidence zone. If results fall below the 75th percentile, we consider that to be too uncertain or “underfunded” and above 90% confidence we consider as needless lifestyle sacrifice or “overfunded,” much like a defined-benefit pension plan funding calculation.

The more realistic dynamic taxation of RMDs in our system, where we measure confidence and our recognition of the price to the lifestyle of the client shows that at high confidence levels the Roth actually is detrimental in this client’s case.

Exhibit 1- 30 Year old Roth versus Traditional Tax Deferred 401(k)

Defenders of needlessly prepaying taxes will say it is erroneous to conclude that this client would leave nothing behind in their estate and that part of the benefit of the Roth is how the assets transfer to heirs by avoiding income taxation on accumulated tax-deferred IRA assets. Of course, if he wanted to leave an estate we would have identified and prioritized this goal, and if he didn’t want to leave an estate our Wealthcare advising process would adjust our advice over time to confidently have his money and blood pressure run out near the same time.

But, assuming he has an estate goal, to model this we will bump up his savings to an $8,500 Roth contribution, a lifestyle-equivalent $12,274 tax deferred contribution, and we will add a goal of a $1 million estate in today’s dollars ($6.4 million in actual dollars). This gives the Roth 78% confidence of exceeding his income and estate goals after income taxes (but before estate taxes).

Under this scenario, we can be 86% confident that the traditional 401(k) would exceed his $1,000,000 estate goal, but this is before income taxes on the amount remaining in tax-deferred assets. For the traditional 401(k), the 78th percentile outcome leaves his estate with $615,489 in taxable assets1 with a stepped-up basis and $850,878 in tax-deferred assets that would be subject to ordinary income tax. If we assume the beneficiaries immediately pay the income tax on this, their tax rate would have to be about 55% on the tax-deferred assets to be at a disadvantage to the Roth. Tax rates could go this high, and if they did the Roth conversion would look attractive. Of course, most people would apply some common sense and would opt to stretch out the tax bite using either the five year deferral option or the lifetime distribution option.

Within the distribution of outcomes, there are advantages to Roth for this combined income and estate goal circumstance. For example, at the 50th percentile outcome, the Roth would leave an estate that is 2.8 times his estate goal (assuming, of course, that the client wouldn’t use the extra two million dollars for his lifestyle). The tax-deferred account would leave an estate that is 3.3 times his estate goal, but a significant amount of that would be in tax deferred balances with income taxes still due. At the 50th percentile, the breakeven tax rate on the tax-deferred assets left for the heirs would be only 23% to equal the wealth of the tax-exempt Roth. Of course we have no idea what the tax rate will be for heirs or how long they would defer or stretch out the distributions. We also don’t know whether the client would end up spending more than we are assuming if he had a couple extra million dollars lying around, completely changing the analysis and our future advice.

What we do know is that as confidence increases (lower investment return scenarios) deferring taxation in the traditional 401(k) or IRA makes it reasonably unlikely the future tax bite heirs will pay will be high enough to justify the Roth conversion (i.e. 55% tax rate at the 78th percentile). We also know that if returns are higher and investors are thus significantly exceeding their goals, it becomes increasingly likely that the Roth tax treatment would have a wealth advantage over tax-deferred treatment, albeit at levels of wealth that are already at multiples of the client’s goals (for example, at the 50th percentile heirs’ income taxes at more than 23% would show an advantage to the Roth but the estate would already be 2.8 times more than desired).

This should dispel some of the common claims made about the advantages of Roth. It just isn’t as easy as assuming a flat tax rate on all scenarios, as taxes will vary from year to year based on uncertain market returns. The higher returns are, the more likely there will be a wealth advantage to the Roth but also less confidence one can have in achieving those higher returns.

What if you have accumulated significant tax-deferred assets?

The industry paper I reviewed showed another example that is perhaps more germane to the decision many high earners now face: whether they should convert now after already having accumulated significant tax-deferred assets.

The paper showed several examples to make the case that if one has enough taxable assets to pay for the conversion, there would be a high probability of an advantage to the Roth. In fact, the paper claimed that if tax rates don’t decline in retirement for someone with $1 million in tax-deferred assets and $450,000 in taxable assets that they use to pay for the conversion then that person would have a 97% probability of benefiting from the switch.

Silly assumptions in the calculations caused this ridiculous conclusion.

Replicating the analysis in our system, I take the same 65-year-old couple that is faced with making this decision, the same 20-year time horizon (they used normal life expectancy), the same present account values and even the same 60/40 asset allocation assumption. Instead of assuming the same flat tax rate regardless of the market simulations, I used our dynamic tax assumptions that not only calculate the differing year by year tax rates and forced RMDs as previously mentioned but also assumes postponing withdrawals from tax deferred assets until RMDs kick in or there is a need to make tax deferred withdrawals to meet spending goals.. This is more akin to how we would actually manage our own clients’ affairs. To keep their tax rates on the IRA distributions high, I included a taxable retirement pension income of $60,000 starting at age 65 and assumed an after-tax inflation-adjusted spending need of $130,000. (In our process, we are concerned with the lifestyle of what our clients can actually spend, so our engine forces larger distributions and taxes them sufficiently to meet the net spending desired.) Our assumption of the $130,000 spending need is what is materially different from the erroneous analysis of the paper.

1 Taxable assets were accumulated by forced RMDs above his income need that were taxed at ordinary income tax rates and then invested in a taxable account with 20% turnover and 20% short term capital gains rates, about twice what we would safely assume with our portfolio management approach.

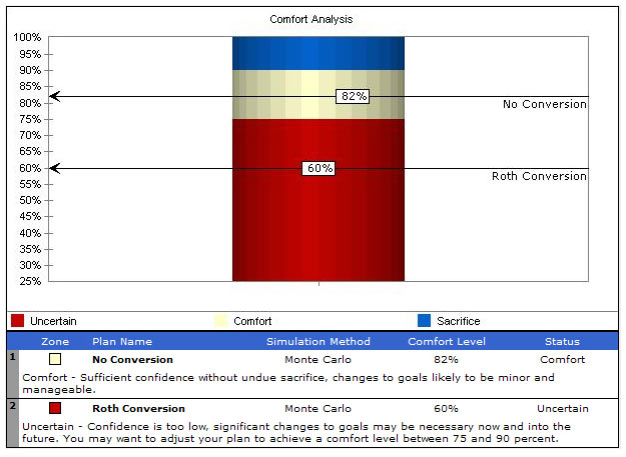

The way the paper approached income distribution was to simply take 1/20th of the Roth value the first year, 1/19th the next, and so on until it was depleted. Its authors then distributed the same dollar amounts from the IRA and taxed any remaining assets all at once at ordinary income rates at the end. Never mind that no one would do this and couldn’t really plan on a retirement lifestyle with this spending approach. But doing the analysis this way and using fixed-tax assumptions despite uncertain market returns lead to the erroneous conclusion there is a 97% chance we should rush to stroke a $450,000 check to the IRS. Hopefully, the public is smarter than this and most of them have an advisor that has the skill to appropriately model their unique situation. Exhibit 2 demonstrates that there is a cost to needlessly writing that check to the IRS.

Exhibit 2, confidence levels of supporting a $130,000 spending need for 20 Years by converting a $1 million IRA to a Roth, versus keeping IRA and $450,000 of taxable assets with $60,000 pension:

Do not take this analysis as an assumption that the Roth option is uniformly unattractive. There are a number of circumstances under which one would benefit from the Roth conversion. The key thing to remember is that paying taxes now with certainty has an uncertain future benefit or cost. The odds of a conversion being beneficial are reasonably high. But at comfortable confidence levels the certainty of giving up the assets, especially given the flexibility of choice that having those assets could otherwise have offered, can come at a price. Even if one is only making modest distributions and using the assets to grow an estate, at comfort-zone confidence levels it is often wise to avoid conversion. If markets perform better than these levels, there will be a price to not converting, but the Roth benefits are generally reserved for heirs and usually occur in markets that produce multiples of desired estate goals.

There is a clear benefit to the Roth conversion if an investor is highly confident that he will not need to use the IRA assets for any lifestyle goals at any time in the future and that he will remain in a high tax bracket throughout retirement. In such cases, conversion clearly makes sense. If one is so over-funded for his goals, however, this suggests a shortage of goals. In our process we would help the client identify what he wants to achieve with such excess wealth.

Don’t use conversion calculators that relinquish control of the analysis to an over-simplified user interface. If the inputs do not require careful thought and introspection, simplifying assumptions buried behind in the interface might lead to highly misleading and costly answers. Such systems give a false sense of security at the expense of our clients’ lifestyles. If you can’t figure out what is really going on under the hood or the tipping point of where the price and benefits cross in such decisions, contact us and we can lend our expertise to help you make an informed and objective decision.

A popular industry speaker and writer, DAVID B. LOEPER is the CEO and founder of Financeware, Inc. in Richmond, VA. He is author of the top-selling book Stop the 401(k) Rip-off!, three other books released in 2009 by John Wiley & Sons (Stop the Retirement Rip-off, Stop the Investing Rip-off and The Four Pillars of Retirement Plans) and numerous white papers. You may subscribe to our educational emails.

Read more articles by David B. Loeper, CIMA, CIMC